IndiaFilings

Expert

Published on: Apr 22, 2026

IGST on Imports - Calculation Methodology

The formalities for import and export would change once GST is implemented in India on 1st July 2017. Under GST, certain types of duties and taxes like Basic Customs duty, Education Cess, Anti-dumping duty, Safeguard duty and the like would continue. On the other hand, Countervailing Duty (CVD) and Special Additional Duty of Customs (SAD), would be replaced by Integrated Goods and Services Tax(IGST). In this article, we look at the levy of IGST on imports along with the procedure for calculation of IGST on imports into India.

Duties Levied on Imports under GST

From 1st July 2017, the duties and tax levied on imports into India would change significantly. Before implementation of GST, the following types of duties and taxes are levied on imports into India based on the HSN code of the item.

- Basic Customs Duty

- Countervailing Duty (CVD)

- Special Additional Duty of Customs (SAD)

- Education Cess

- Anti-dumping duty

- Safeguard duty

Once GST is implemented, the following duties and taxes would be applicable for a majority of the products :

- Basic Customs Duty

- Integrated Goods and Services Tax (IGST) - Know more about IGST, CGST and SGST

- GST Compensation Cess

- Education Cess

- Anti-dumping duty

- Safeguard duty

Cutoff Date for GST Implementation Purposes

According to a notification issued by the Central Board of Excise and Customs, IGST and GST Compensation Cess would be levied on all cargo that arrives into India on or after 1st July 2017. Further, IGST and GST Compensation Cess would be applicable on all goods that arrived into India after 30th June 2017 for which Bill of Entry is filed on or after 1st July 2017. In case of goods arriving into India after 1st July 2017 for which advance bill of entry was filed, the bill of entry can be recalled, and the Customs Officer could reassess for levy of IGST and GST Compensation Cess.

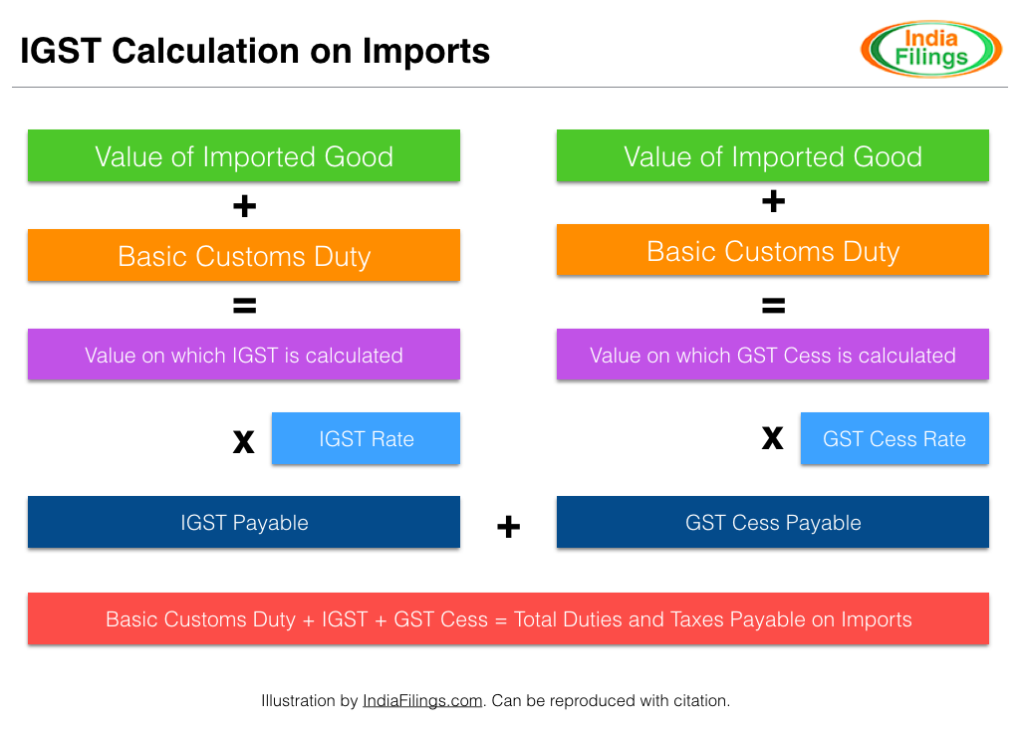

Calculating GST on Imports

GST is applicable on all imports into India in the form of levy of IGST. It is levied on the value of imported goods + any customs duty chargeable on the goods. Hence, IGST must be calculated after adding the applicable customs duty to the value of imported goods. 1.

If for any imported articles, in addition to basic customs duty, other duty of customs is chargeable, then it must be included along with the basic customs duty to arrive at the value on which GST cess or IGST is calculated. To arrive at the rate for levying IGST or GST Compensation Cess, the methodology shall include education cess, higher education cess, as well as anti-dumping and safeguard duties. Further, it shall also include, anti-dumping and safeguard duties must be added along with basic customs duty.

If for any imported articles, in addition to basic customs duty, other duty of customs is chargeable, then it must be included along with the basic customs duty to arrive at the value on which GST cess or IGST is calculated. To arrive at the rate for levying IGST or GST Compensation Cess, the methodology shall include education cess, higher education cess, as well as anti-dumping and safeguard duties. Further, it shall also include, anti-dumping and safeguard duties must be added along with basic customs duty.

Input Tax Credit for Imports under GST

Under GST, the

input tax credit would be provided for IGST paid, and GST Compensation Cess paid. However, the input tax credit is not applicable for basics customs duty paid during imports. To avail input tax credit, the importer would have to obtain GST registration and quote the GSTIN on Bill of Entry. During the transitional period, provisional GSTIN can also be quoted instead of GSTIN.Know more about GST at the IndiaFilings GST Portal