IndiaFilings

Expert

Published on: Apr 22, 2026

Form 16: Benefits, Format & How to Download?

Form 16 is a crucial certificate issued by employers to salaried employees in India, serving as proof of Tax Deducted at Source (TDS) from their salary income. This essential document plays a key role in Income Tax Return (ITR) filing, providing a detailed breakdown of salary components, tax-exempt allowances, and deductions. Beyond simplifying the income tax filing process, Form 16 is also commonly required when applying for loans, claiming tax deductions, or for visa processes, among other purposes. In this article, we’ll explore the definition, components, the process to download Form 16, and how to use it effectively for accurate taxation and compliance.

What is Form 16?

Form 16 is a TDS (Tax Deducted at Source) certificate issued by an employer under Section 203 of the Income Tax Act, 1961, and is a key document for salaried employees in India. It is provided on or before June 15th of the following financial year, after the income has been earned and tax has been deducted. The certificate serves as proof of TDS deducted and deposited with the Income Tax Department, containing essential details such as salary earned, income tax deducted, and other relevant information required to file Income Tax Returns (ITR) accurately.

Also referred to as a salary TDS certificate, Form 16 outlines the salary components, taxable income, and deductions, making it indispensable for ITR filing and claiming refunds, if eligible. If your salary income exceeds the basic exemption limit of ₹2,50,000, your employer is mandated to deduct TDS and issue this certificate. In cases where an employee has changed jobs or worked with multiple employers during the financial year, they must collect Form 16 from each employer, as it reflects the individual TDS details for each employment period. However, if your annual income is below the taxable limit, and no TDS is deducted, Form 16 may not be issued.

Benefits of Form 16 TDS Certificate

Form 16 offers several practical advantages to salaried individuals, especially in the context of income tax compliance and financial transactions. Below are the key benefits rephrased and explained in detail:

1. Proof of Tax Compliance

Form 16 serves as official documentation that tax has been deducted at source by your employer and deposited with the Income Tax Department. This helps you stay compliant with your tax obligations and provides a reliable record for any future reference or verification.

2. Ease in Filing Income Tax Returns

By containing all necessary information related to your salary, TDS, and deductions, Form 16 simplifies the process of filing your Income Tax Return (ITR). It eliminates the need to gather multiple documents, making it easier to calculate your total income and tax liability accurately.

3. Helps in Claiming Tax Deductions

The certificate includes a detailed summary of investments and deductions claimed under various sections, such as Section 80C and 80D. This helps ensure that all eligible deductions are accounted for, thereby reducing your overall tax liability.

4. Essential for Loan Approvals

Financial institutions often request Form 16 as proof of steady income and tax compliance when assessing your eligibility for loans such as home loans, personal loans, or car loans. It helps lenders verify your repayment capacity based on the income you have disclosed.

5. Supports Tax Refund Claims

If excess tax has been deducted from your salary, Form 16 provides the necessary details to file a refund claim accurately. It ensures that any overpaid tax can be recovered efficiently during the income tax return (ITR) process.

Eligibility & Applicability of Form 16

According to the guidelines set by the Ministry of Finance of the Indian Government, Form 16 applies to salaried individuals whose income exceeds the basic exemption limit. It is therefore subject to Tax Deducted at Source (TDS). In such cases, employers are legally required to issue Form 16 as proof of tax deducted at source (TDS). However, if an employee’s annual income does not cross the taxable threshold, TDS is not applicable, and the employer is not obligated to provide Form 16. Despite this, many organisations voluntarily issue the certificate even to non-taxable employees as a good practice, as it offers consolidated summary of earnings and serves multiple administrative and financial purposes.

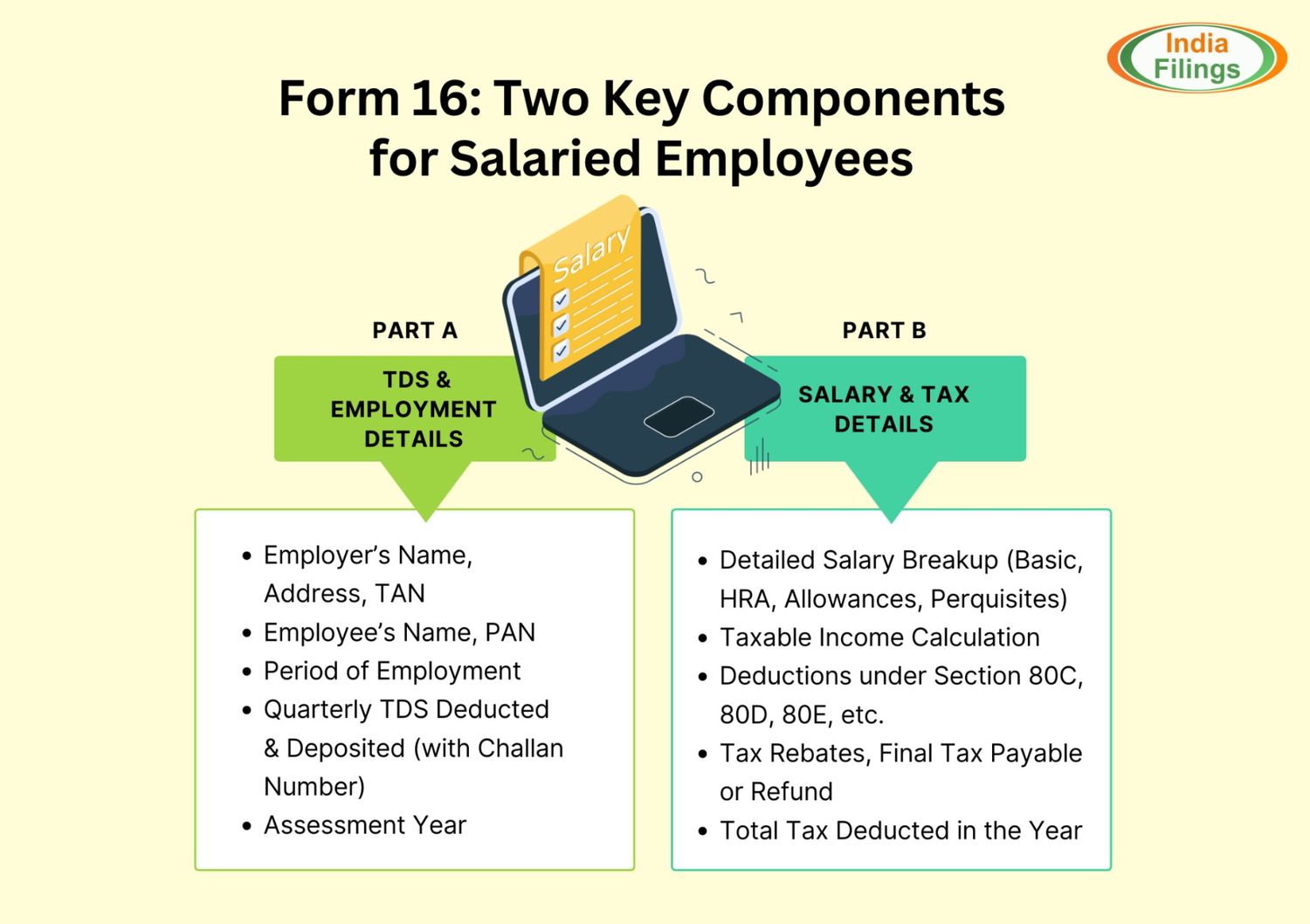

Components of Form 16 - Part A & B

Form 16 is divided into two distinct parts - Part A and Part B, each serving a specific purpose in helping salaried individuals understand their earnings, deductions, and tax liabilities. While Part A contains details related to TDS and employment, Part B offers a comprehensive breakdown of income and applicable deductions.

Together, these sections provide all the necessary information required to file your Income Tax Return (ITR) accurately.

1. Part A of Form 16

This section covers the essential details related to tax deduction and employment:

- Employer’s Details: Name, address, and TAN (Tax Deduction and Collection Account Number) of the employer.

- Employee’s Details: Name, PAN (Permanent Account Number), and employment specifics.

- Period of Employment: The time frame during which the employee worked with the employer in the given financial year.

- TDS Information: Monthly details of TDS deducted and deposited with the government, including the Challan Identification Number (CIN).

- Assessment Year: Indicates the financial year for which the tax is assessed and deducted.

2. Part B of Form 16

Part B is an annexure to Part A and provides a detailed summary of salary and tax computation:

- Breakdown of Salary Components: Includes basic salary, house rent allowance, travel allowances, perquisites, and other salary-related elements.

- Taxable Income Calculation: Computation of total taxable income after accounting for all allowable exemptions and deductions.

- Deductions Under Section 80: Details of deductions claimed under sections like 80C, 80D, 80E, etc., for investments, insurance premiums, education loans, and more.

- Rebate and Tax Payable: Information on applicable tax rebates, final tax liability, or refund due.

- Tax Paid Details: A consolidated summary of total tax deducted by the employer throughout the year.

Sample Format of Form 16

Below, we have attached the sample format of Form 16 to give you an idea about the structure and content:

How to Download Form 16?

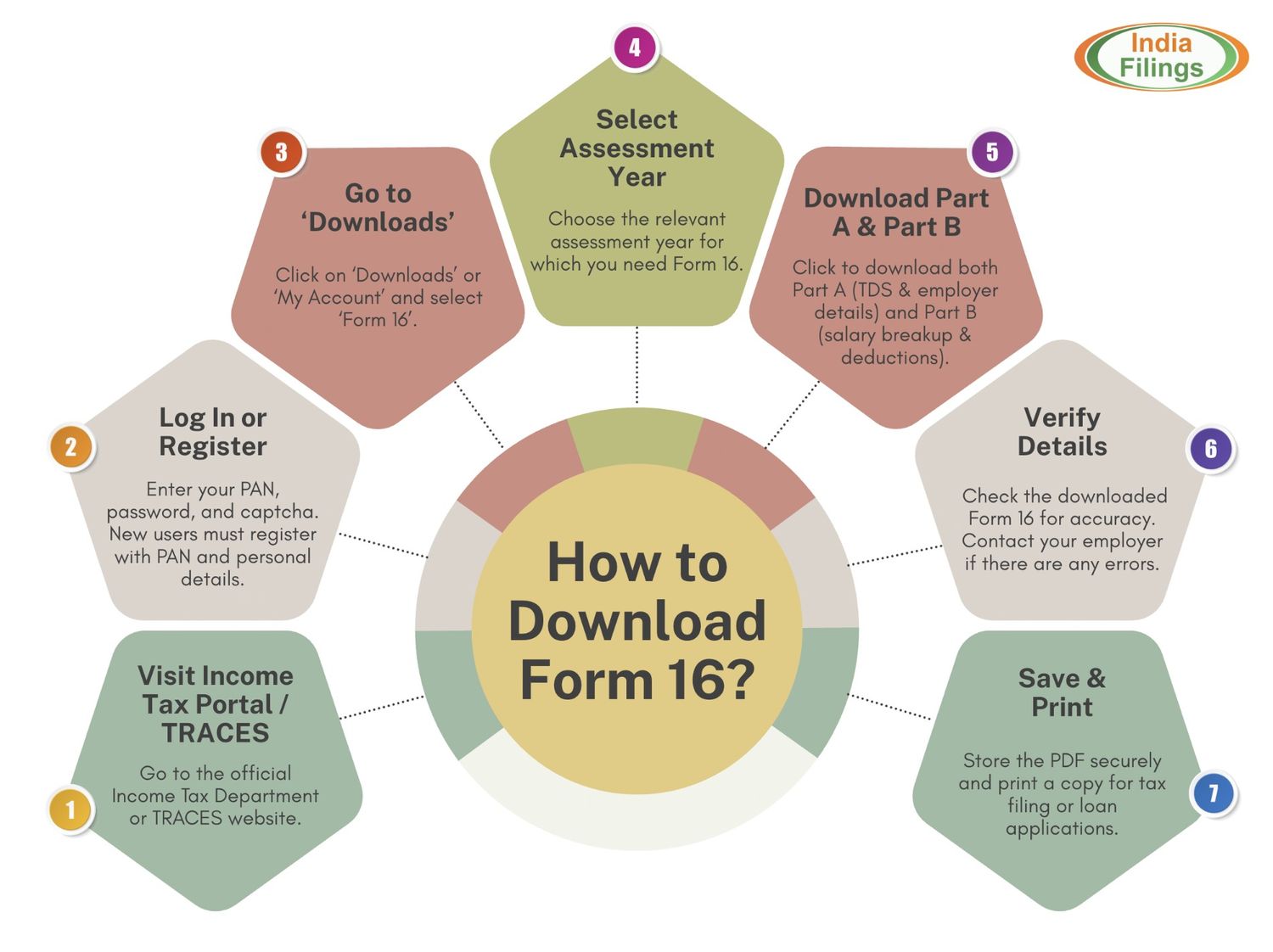

Salaried individuals registered with the Income Tax Department of India can download Form 16 from the IT Portal. This document, issued annually by your employer, can be accessed online if your employer has uploaded it to the portal. Follow the steps below to download Form 16:

- Visit the Income Tax Department Portal: Go to the official website of the Income Tax Department of India.

- Log in or Register:

- If you’re an existing user, log in using your PAN, password, and captcha code.

- New users must register by providing details such as their PAN, name, date of birth, and contact information.

- Navigate to the Downloads Section: After logging in, click on the ‘My Account’ tab. Then go to ‘Downloads/Forms’ and select ‘View Form 16’ from the dropdown list.

- Select Assessment Year: Choose the appropriate assessment year for which you want to download Form 16. For example, if the financial year is 2023–24, the assessment year will be 2024–25.

- Download Part A of Form 16: Click on the download link to get Part A, which contains your employer's TAN, your PAN, period of employment, and TDS details.

- Download Part B of Form 16: Download Part B, which includes a detailed breakup of your salary components, deductions under Section 80, taxable income, and final tax liability.

- Verify Information: Cross-check both parts of the form to ensure that the details match your salary records. In case of any discrepancies, contact your employer for corrections.

- Save and Print: Save the Form 16 PDF securely for your records. You may also print a copy for physical documentation or future reference, especially while filing your Income Tax Return (ITR) or applying for loans.

How to Use Form 16 for ITR Filing?

Form 16 can be utilised for income tax filing for various purposes since it contains essential details such as salary income, TDS deductions, and eligible deductions under various sections of the Income Tax Act. Here's a step-by-step guide on how to use Form 16 for filing your ITR:

- Collect All Necessary Documents: Before you begin, gather Form 16, salary slips, Form 26AS, and investment proofs to ensure all income and deduction details are accurate.

- Log In to the e-Filing Portal: Visit the official Income Tax e-Filing portal and log in using your PAN, password, and captcha code.

- Select the Appropriate ITR Form: Based on your income sources (salary, other income, etc.), choose the relevant ITR form (e.g., ITR-1 for most salaried individuals).

- Enter Form 16 Details: Use Form 16 to fill in salary income, TDS deducted, and employer details. Make sure the information entered matches exactly with what is provided in the form.

- Verify Deductions: Cross-check and enter eligible deductions under Sections 80C, 80D, 80E, and others, as shown in Part B of Form 16 or based on additional investment proofs.

- Calculate Tax Liability: Review your income details and compute your total tax liability. If there's any additional tax payable, you can pay it online through the portal.

- Submit and Verify ITR: Once all the information is complete, submit your ITR. Complete the process by verifying it online using methods such as Aadhaar OTP, net banking, or by sending a signed ITR-V form to the CPC in Bangalore.

Difference between Form 16, Form 16A & Form 16B

It’s important to distinguish between Form 16, Form 16A, and Form 16B, as each serves a distinct function within the Indian taxation framework. In the table below, we have given the differences between Form 16, Form 16A, and Form 16B:

Particulars | Form 16 | Form 16A | Form 16B |

Description | Certificate of TDS on salary income, issued to employees. | Certificate of TDS on non-salary income such as interest, commission, or rent. | Certificate of TDS for property transactions under Section 194-IA of the Income Tax Act. |

Who Issues It | Employer | Financial institution or any deductor other than an employer | Buyer of the property |

Income Covered | Salary income | Income from sources like interest, commission, or rent | Sale of immovable property (excluding agricultural land) |

Frequency | Issued once a year | Issued every quarter | Issued for every eligible property sale transaction |

Threshold Limit | Applicable if salary exceeds the basic exemption limit | Applicable if the specific income crosses the TDS threshold for that category | Applicable if the property’s sale value or stamp duty value is more than ₹50 lakhs |

Purpose | Serves as proof of TDS on salary, required for filing income tax returns | Serves as proof of TDS on non-salary income | Serves as proof of TDS deduction on property sales |

Rates | According to income tax slab rates | As per the rates specified under respective TDS sections | 1% of the sale consideration or stamp duty value, whichever is higher |

Mode of Issuance | Downloaded by the employer from the TRACES portal and given to the employee | Downloaded by the deductor from the TRACES portal and given to the payee | Downloaded by the property buyer from the TRACES portal and given to the seller |

Conclusion

Form 16 remains an important document for salaried employees in India, serving as a comprehensive record of income earned, taxes deducted, and deductions claimed. By clearly outlining salary components and TDS details, it not only simplifies the ITR filing process but also supports financial activities like loan applications and refund claims. Understanding the structure and usage of Form 16 empowers individuals to maintain tax compliance, avoid errors during return filing, and take full advantage of eligible deductions under the Income Tax Act.

FAQs

1. What is Form 16, and who issues it?

Form 16 is a TDS certificate issued by an employer to salaried employees, detailing the salary paid and the tax deducted during the financial year. It serves as proof of TDS for income tax purposes.

2. When is Form 16 issued by the employer?

Employers must issue Form 16 on or before June 15th of the following financial year in which the tax was deducted.

3. What is the difference between Part A and Part B of Form 16?

Part A contains employer and employee details, TDS summary, and period of employment, while Part B includes the breakup of salary, exemptions, deductions under Section 80, and tax computation.

4. Can I get Form 16 if my salary is below the taxable limit?

Form 16 is not mandatory if your income is below ₹2.5 lakhs and no TDS is deducted. However, some employers may still issue it voluntarily.

5. How can I download Form 16 online?

Form 16 can be downloaded from the Income Tax Portal if uploaded by your employer. Log in to the portal, navigate to 'Downloads', select the relevant assessment year, and download both Part A and Part B.

6. Is Form 16 mandatory for filing Income Tax Returns (ITR)?

While not legally mandatory, Form 16 significantly simplifies the ITR process by providing all necessary salary and TDS information in one place.

7. What should I do if there is an error in Form 16?

In case of discrepancies, you should contact your employer immediately for corrections before proceeding with ITR filing.

8. What is the difference between Form 16, 16A, and 16B?

Form 16 is for salary income, Form 16A covers TDS on non-salary income like interest and rent, and Form 16B is issued for TDS on property transactions under Section 194-IA.