IndiaFilings

Expert

Published on: Mar 28, 2026

TDS on Property Purchase

Tax Deducted at Source (TDS) refers to the tax withheld by a payer of income, on a payment made to a recipient. TDS applies to payments made in connection with the purchase of an immovable property. Any person who purchases a property from a resident transferor is required to deduct tax at source (TDS) on any money or consideration paid. In this article, we look at the applicable TDS on property purchase.

Click here to learn more about Section 194IA – TDS on Sale of PropertyWhen is TDS on Property Purchase Required?

TDS must be deducted from all immovable property purchase. Immovable property means land or any building, other than agricultural land. In the following cases, TDS on property purchase is not required:

- When the immovable property transferred is rural agricultural land.

- When the immovable property is being compulsorily acquired under any law by the Government.

- When the total amount of consideration paid for the purchase of immovable property is less than Rs.50 lakhs.

TDS must be deducted during a property purchase at the time of transfer of money to the account of property seller or at the time of payment of any money in cash or by cheque or demand draft. This is how the TDS on purchase of property works.

TDS Rate on Property Purchase

The TDS rate for property purchase is 1%. Surcharge and secondary and higher education cess (SHEC) need not be added. If the property seller does not have PAN or if PAN is not quoted, then TDS must be deducted at the rate of 20%. At this rate only, the TDS on property purchase will be deducted.

Procedure for Remitting Deducted TDS on Property Purchase

Any amount deducted as TDS on property purchase must be remitted electronically within seven days from the end of the month in which deduction was made to any of the banks authorised as below:

- Allahabad Bank

- Andhra Bank

- Axis Bank

- Bank of Baroda

- Bank of India

- Bank of Maharashtra

- Canara Bank

- Central Bank of India

- Corporation Bank

- Dena Bank

- HDFC Bank

- ICICI Bank

- IDBI Bank

- Indian Bank

- Indian Overseas Bank

- Jammu & Kashmir Bank

- Oriental Bank of Commerce

- Punjab and Sind Bank

- Punjab National Bank

- State Bank of India

- Syndicate Bank

- UCO Bank

- Union Bank of India

- United Bank of India

- Vijaya Bank

Payment of TDS on property purchase can be done only through online payment or at any of the banks above. The payment must be accompanied by a challan in Form 26QB.

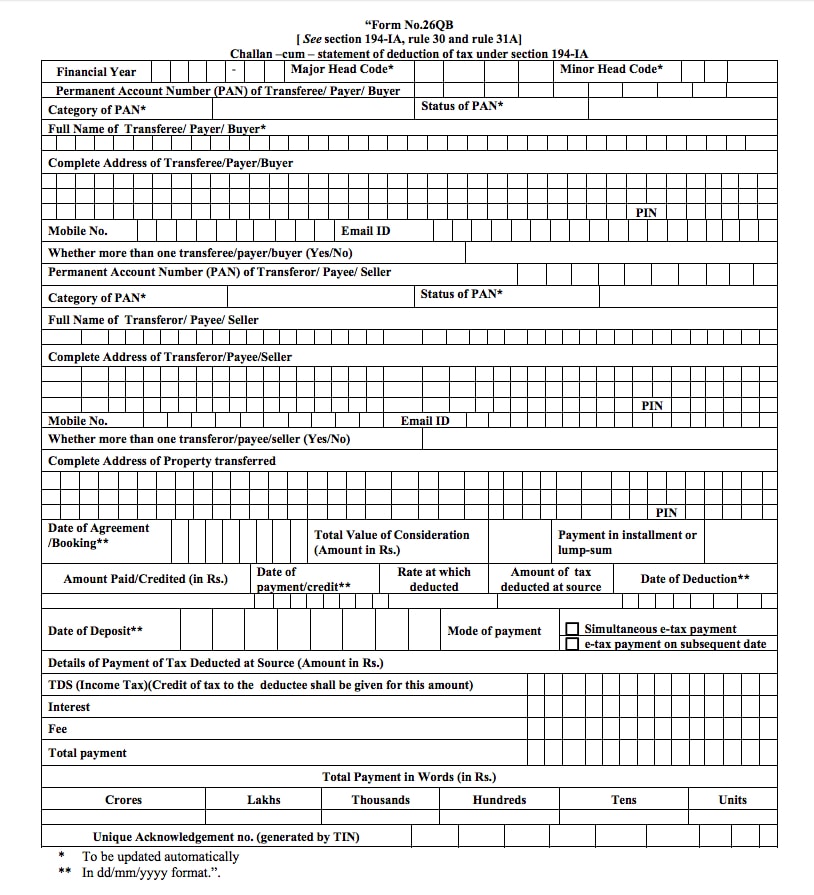

Form 26QB - TDS on Purchase of Property

Form 26QB is the name of the challan which should be submitted to the Income Tax Department at the time of remitting the TDS amount to the Government.

Form 26QB

Form 26QB can be generated and submitted online on the TIN Network website after the payment of TDS on purchase of property is made.

Form 26QB

Form 26QB can be generated and submitted online on the TIN Network website after the payment of TDS on purchase of property is made.

Form 16B - TDS on Purchase of Property

All persons responsible for TDS on property purchase are required to furnish a certificate to the seller in Form 16B within 15 days of the due date of filing Form 26QB. Form 16B format is attached below for reference:

To prepare and download Form 16B, the taxpayer who are responsible for TDS on property purchase can follow the steps mentioned below:

- Login to TRACES.

- Go to Downloads tab.

- Select Form 16B.

- Enter the details and click on go.

To know about the concept of Tax Audit Turnover in Income Tax, click

here.FAQs on TDS on Property Purchase

1. What is TDS on property purchase?

TDS on property purchase refers to the tax that must be deducted by the buyer when paying a resident seller for immovable property, such as land or a building, but not including agricultural land if the transaction value exceeds Rs. 50 lakhs.

2. When is TDS applicable on property purchase?

TDS is required to be deducted on all immovable property purchases, except when the property is rural agricultural land, compulsorily acquired by the government, or when the transaction value is below Rs. 50 lakhs.

3. What is the rate of TDS on property purchase?

The TDS rate for property purchase is 1%. If the seller does not provide a PAN, TDS should be deducted at 20%.

4. Who is responsible for deducting TDS on property purchase?

The buyer of the property is responsible for deducting TDS when purchasing immovable property from a resident seller.

5. How is TDS calculated on property purchase?

TDS is calculated at 1% of the transaction amount if the property value is above Rs. 50 lakhs. If no PAN is provided by the seller, the TDS rate is 20%.

6. Is TDS applicable on all types of properties?

TDS is applicable to all types of immovable properties, except agricultural land in rural areas and properties compulsorily acquired by the government.

7. How and where can I pay the TDS on property purchase?

TDS on property purchase must be paid electronically through the TIN website using Form 26QB. The amount deducted must be remitted within seven days from the end of the month of deduction at any authorized banks.

8. Who will pay 1% TDS on sale of property?

The buyer is required to deduct and pay 1% TDS on the sale of property where the transaction value exceeds Rs. 50 lakhs.

9. What is the new rule for TDS on property?

The new rule mandates that for any property transaction exceeding Rs. 50 lakhs, the buyer must deduct 1% TDS from the payment made to the seller.

10. What is the time limit to pay TDS on property purchase?

The deducted TDS must be paid within seven days from the end of the month in which the TDS is deducted.

11. What happens if the buyer doesn't deduct TDS on property?

If the buyer fails to deduct or deposit TDS on property, they may face penalties and interest charges for non-compliance with TDS regulations.