IndiaFilings

Expert

Published on: Apr 22, 2026

GST Input Tax Credit Guide

GST is an indirect tax levied on goods and services based on the principle of value addition. Hence, the levy of tax is based on the value-added at each stage of the supply chain until the product or service reaches the ultimate consumer. In such a tax system, to negate the cascading effect of the tax, there exists a means to set of taxes paid on procurement of raw materials, consumables, plant and machinery, equipment, services, etc., that are used for the manufacturing or supply of goods and services. This element used to offset the tax liability is called an input tax credit. In this article, we look at the concept of Input Tax Credit under GST in detail.

What is Input Tax Credit?

Under GST, each person having a

GST registration in the supply chain takes part in the process of controlling, collecting GST tax and remitting the amount collected. However, to avoid double taxation and cascading effect of the tax, input tax credit is provided as a means to set off tax paid on procurement of raw materials, consumables, goods or services that were used in the manufacturing and supply and sale of goods or services. By using the input tax credit mechanism, businesses are able to achieve neutrality in the incidence of tax and ensure that such input tax element does not enter into the cost of production or cost of supply of goods and services.Eligibility for Claiming Input Tax Credit

To claim the Input tax credit, the taxpayer should have registered with GST by providing all the necessary documents and filed GSTR-2 returns. The following documentary requirements must be satisfied by a taxpayer for claiming the credit:

- An invoice issued by the Supplier as per the GST Rules for Invoice; or

- A debit note issued by a supplier; or

- A bill of entry or any similar document; or

- An ISD invoice or ISD credit note or any document issued by an Input Service Distributor.

- The taxpayer is in possession of a tax invoice or debit note issued by a registered supplier or other tax paying documents.

- The taxpayer has received the goods and/or services.

- The tax charged in respect of the supply has been actually paid to the account of the appropriate Government, in cash or through the utilization of available input tax.

- The taxpayer has filed the necessary GST filings.

Goods & Services Not Eligible for Input Tax Credit

Under GST, the input tax credit does not apply to the below mentioned following goods or services:

- Motor vehicles, except when supplied in the course of business or used for providing taxable services like:

- Transportation of passengers

- Transportation of goods

- Providing training on driving, flying, navigating such vehicles

- Further supply of such vehicles or conveyance

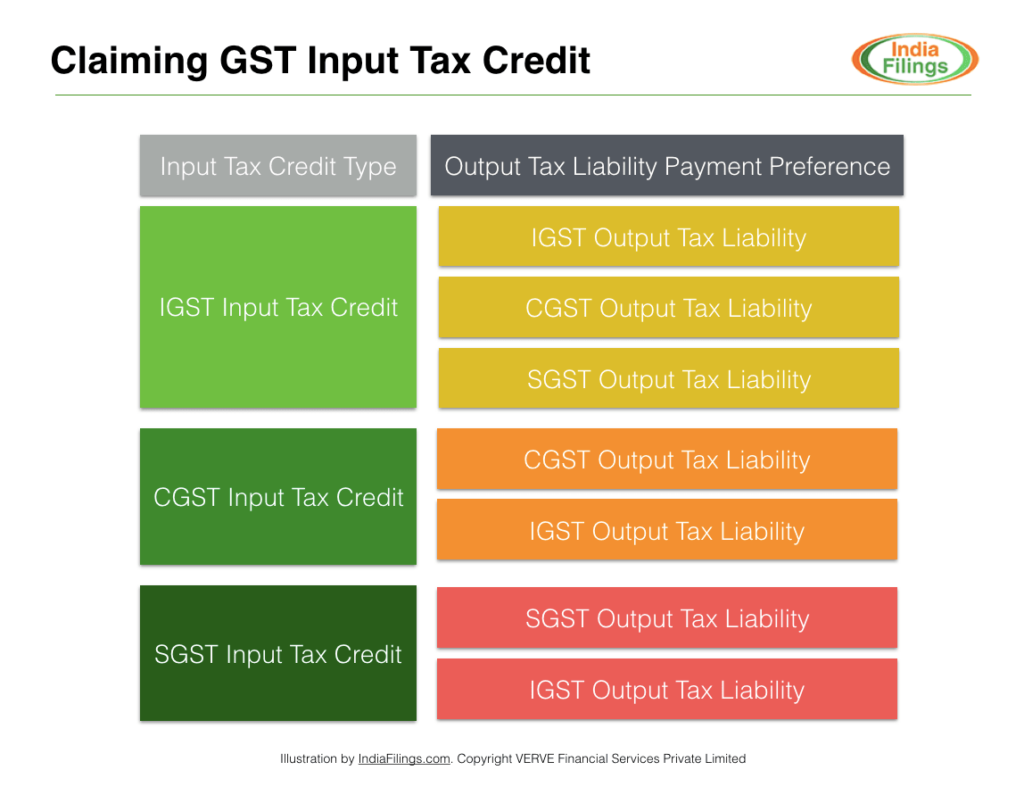

Utilization of CGST and SGST Credit

The following illustration shows the preference for utilisation of GST Input Tax Credit: After filing necessary documents, the taxpayer shall receive the CGST and SGST credit in the electronic credit ledger of the taxpayer, maintained by the GST Network. The taxpayer can use the credit amount to pay output tax payable as notified under the GST Act. However, the individual should use the amount of input tax credit, primarily for making the payment of CGST and the balance amount shall be used for making IGST payments. The input tax credit amount deposited in the electronic credit ledger can hence be used only for IGST and CGST and not making payment for SGST.

Further, it is important to note that only the payment of output tax can be made by utilising the input tax credit. Hence, the taxpayer should make payments for penalty and interest, only using the amount available in the electronic cash ledger.

After filing necessary documents, the taxpayer shall receive the CGST and SGST credit in the electronic credit ledger of the taxpayer, maintained by the GST Network. The taxpayer can use the credit amount to pay output tax payable as notified under the GST Act. However, the individual should use the amount of input tax credit, primarily for making the payment of CGST and the balance amount shall be used for making IGST payments. The input tax credit amount deposited in the electronic credit ledger can hence be used only for IGST and CGST and not making payment for SGST.

Further, it is important to note that only the payment of output tax can be made by utilising the input tax credit. Hence, the taxpayer should make payments for penalty and interest, only using the amount available in the electronic cash ledger.

A simple guide to CGST, SGST and IGST, if you need to understand the difference. A simple guide to electronic cash ledger and procedure for making GST payment.