RENU SURESH

Expert

Published on: Jun 15, 2026

Find Complete Details of Gst Registration Procedure

GST registration applies to all individuals and entities supplying goods or services in India. GST registration becomes mandatory when the aggregate value of supplying goods exceeds Rs.40 lakh. The Ministry of Finance (MoF) has simplified the GST registration process to ease the tax filing process. If the entity operates in a special category state, GST registration becomes applicable if the value exceeds Rs.20 lakh p.a. In this article, let us look at the eligibility to engage in the GST registration process under GST. The article also covers the documents required as well as the Gst Registration Procedure online.

Simplify the GST registration process with IndiaFilings expert assistance!!Latest Update: GST Registration within 3 Days: India’s New Auto-Approval System to Begin Nov. 1, 2025

What is the Eligibility Criteria for GST Registration?

The following mentions the categories and eligibility for GST registration and can go through the procedure for registration under GST:

Aggregate Turnover

Any service provider who provides a service value of more than Rs. 20 Lakhs aggregate in a year is required to obtain GST registration. In the special category states, this limit is Rs. 10 lakhs. Any entity engaged in the exclusive supply of goods whose aggregate turnover crosses Rs.40 lakhs is required to obtain GST registration.

Inter-state Business

An entity shall register for GST if they supply goods inter state, i.e., from one state to another irrespective of their aggregate turnover. Inter state service providers need to obtain GST registration only if their annual turnover exceeds Rs. 20 lakhs. (In special category states, this limit is Rs. 10 lakhs).

E-commerce Platform

Any individual supplying goods or services through an e-commerce platform shall apply for GST registration. The individual shall register irrespective of the turnover. Hence, sellers on Flipkart, Amazon and other e-commerce platforms must obtain registration to commence activity.

Casual Taxable Persons

Any individual undertaking supply of goods, services seasonally or intermittently through a temporary stall or shop must apply for GST. The individual shall apply irrespective of the annual aggregate turnover.

Voluntary Registration

Any entity can obtain GST registration voluntarily. Earlier, any entity who obtained GST voluntarily could not surrender the registration for up to a year. However, after revisions, voluntary GST registration can be surrendered by the applicant at any time.

Types of GST Registration

The following details the types of GST registration which are essential to understand to follow through procedure for registration under GST, properly:

Normal Taxpayer

This category of GST registration applies to taxpayers operating a business in India. Taxpayers registering for normal taxpayer does not require a deposit and also provided with unlimited validity date.

Composition Taxpayer

To register as a Composition Taxpayer, the individual should enroll under GST Composition Scheme. Taxpayers enrolled under the Composition Scheme can pay a flat GST rate. However, the taxpayer would not be allowed to claim the input tax credit.

Casual Taxable Person

Any taxpayer establishing a stall or seasonal shop shall register under Casual Taxable Person. To register as a casual taxable person, the taxpayer shall pay a deposit equal to the amount of GST liability. The liability should match the active registration periods. The registration remains active for a period of 3 months.

Non-Resident Taxable Person

The category non-resident taxable person applies to individuals located outside of India. The taxpayers can supply taxable goods or services to residents in India only after obtaining registration. To register as a non-resident taxable person, the taxpayer shall pay a deposit equal to the amount of GST liability. The liability should match the active registration periods. The registration remains active for a period of 3 months. The following details the types of GST registration process:

- GST Registration for Non-Resident Online Service Provider

- UN Body /Embassy/Other Notified Person

- Special Economic Zone Developer

- Special Economic Zone Unit (SEZ)

- GST TDS Deductor-Government Entities

- GST TCS Collector -E-commerce Companies

What is the List of Documents Required for the Gst Registration Procedure?

Before understanding how to do GST registration, let's look at the following checklist of documents required for obtaining GST registration:

| Proof of Constitution of Business (Any One) | Certificate of Incorporation |

| A passport-sized photo of the applicant | Passport-size photo of Promoter/Partner |

| Photo of the Authorised Signatory | Photo |

| Proof of Appointment of Authorised Signatory (Any One) | Letter of Authorisation |

| Copy of Resolution passed by BoD/ Managing Committee and Acceptance letter | |

| Proof of Principal Place of business (Any One) | Electricity Bill |

| Legal ownership document | |

| Municipal Khata Copy | |

| Property Tax Receipt | |

| Proof of Details of Bank Accounts (Any One) | The first page of Pass Book |

| Bank Statement | |

| Cancelled Cheque |

Click here to get the complete GST Registration Documents

Step-by-step Guide On the GST Registration Process Online

The MoF has simplified the online procedure for registration under GST. The applicant can process of GST registration through the GST Portal. After submission of the application, the portal generates GST ARN immediately. Using the GST ARN, the applicant can check the application status and post queries if necessary. Within 7 days of ARN generation, the taxpayer shall receive a GST registration certificate and GSTIN. The following GST registration process guides you through on how to do GST registration clearly.

Step 1: Go to the GST Portal

Access the GST Portal ->/ > Services -> Registration > New Registration option.

Step 2: Generate a TRN by Completing OTP Validation

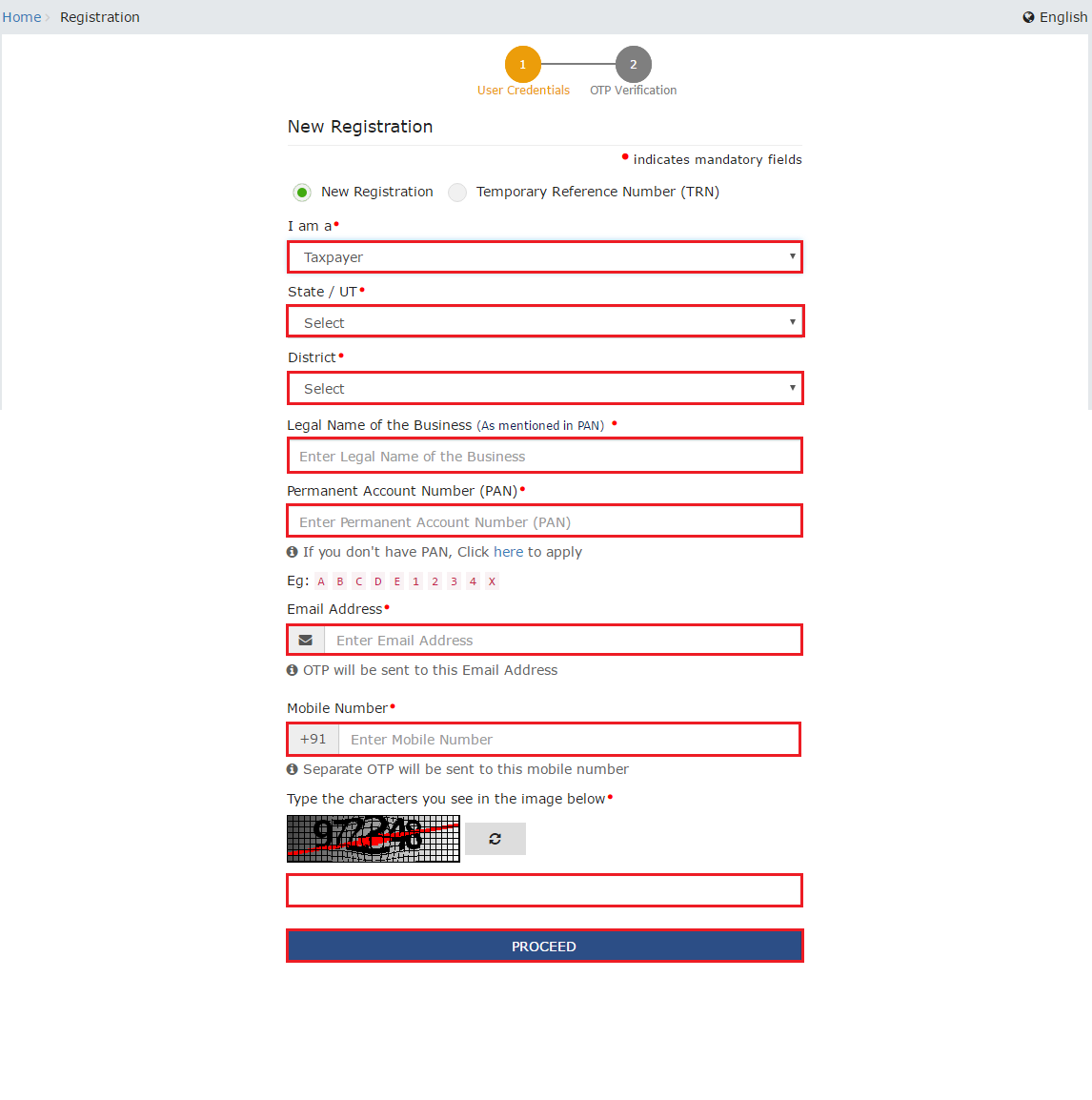

The new GST registration page is displayed. Select the New Registration option. If the GST registration application remains incomplete, the applicant shall continue filling the application using the TRN number.

- Select the Taxpayer type from the options provided.

- Choose the state as per the requirement.

- Enter the legal name of the business/entity, as mentioned in the PAN database. As the portal verifies the PAN automatically, the applicant should provide details as mentioned in the card.

- In the Permanent Account Number (PAN) field, enter the PAN of the business or the PAN of the Proprietor. GST registration is linked to PAN. Hence, in the case of a company or LLP, enter the PAN of the company or LLP.

- Provide the email address of the Primary Authorised Signatory. (Will be verified in next step)

- Click the PROCEED button.

Step 3: OTP Verification & TRN Generation

On submission of the above information, the OTP Verification page is displayed. OTP will be valid only for 10 minutes. Hence, enter the two separate OTP sent to validate the email and mobile number.

- In the Mobile OTP field, enter the OTP.

- In the Email OTP field, enter the OTP.

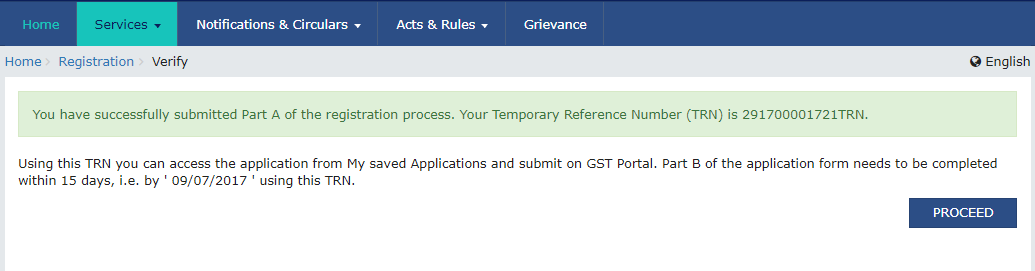

Step 4: TRN Generated

On completing OTP verification, a TRN will be generated. TRN will now be used to complete and submit the GST registration application.

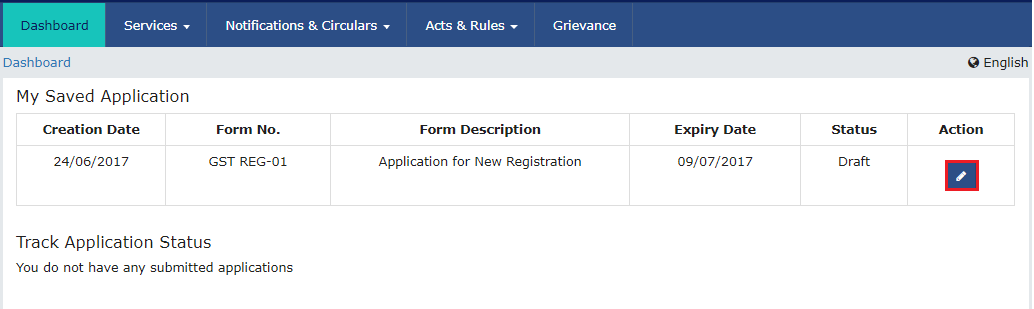

Step 5: Log in with TRN

Upon receiving the TRN, the applicant shall begin the process of GST registration. In the Temporary Reference Number (TRN) field on the GST Portal, enter the TRN generated and enter the captcha text as shown on the screen. Complete the OTP verification on mobile and email.

Click on the icon marked in red to start the process of GST registration.

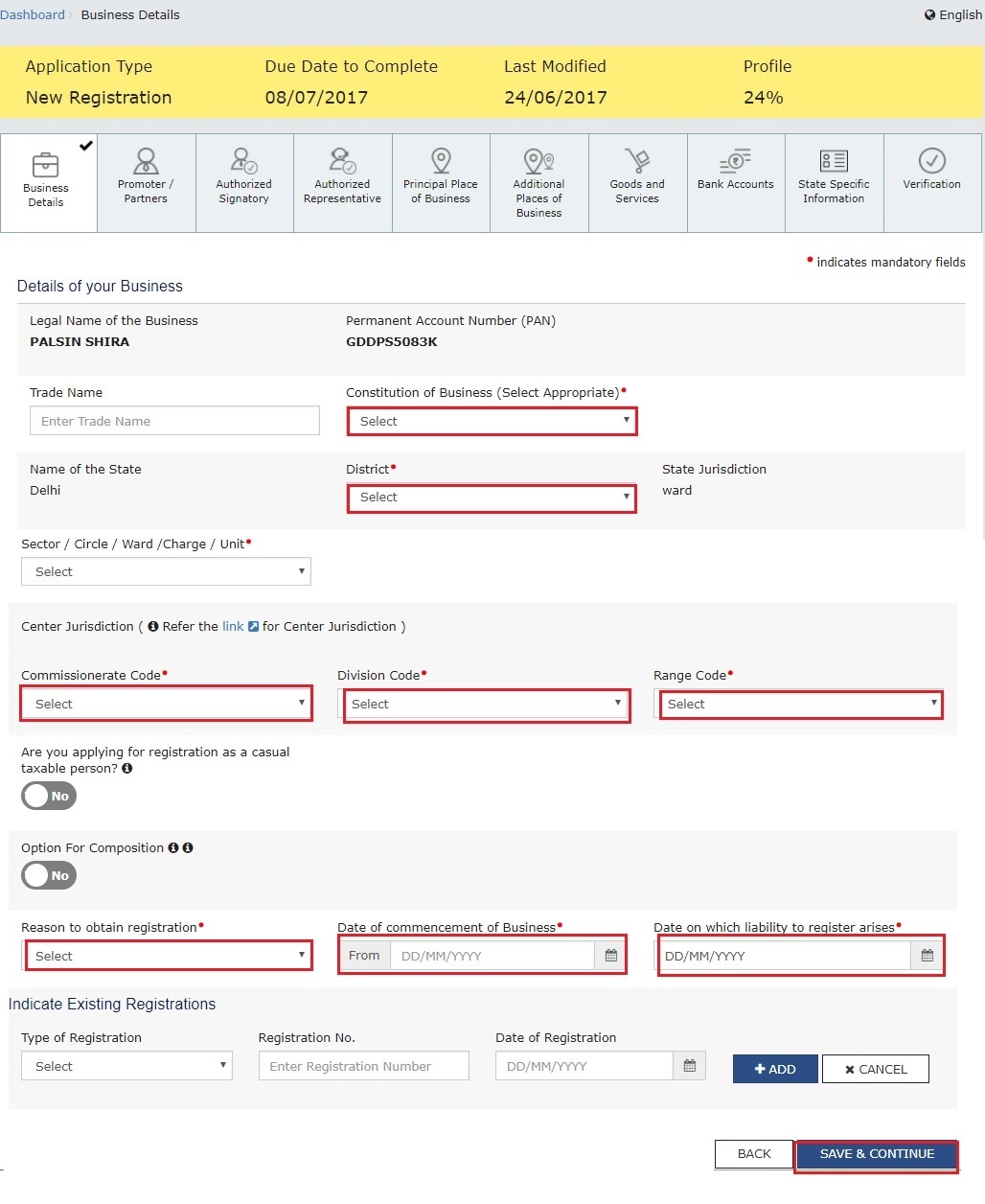

Step 6: Submit Business Information

Various information must be submitted to navigate how to do GST registration properly. In the first tab, business details must be submitted.

- In the Trade Name field, enter the trade name of the business.

- Input the Constitution of the Business from the drop-down list.

- Enter the District and Sector/ Circle / Ward / Charge/ Unit from the drop-down list.

- In the Commissionerate Code, Division Code and Range Code drop-down lists, select the appropriate choice.

- Opt for the Composition Scheme, if necessary

- Input the date of commencement of business.

- Select the Date on whichthe liability to register arises. This is the day the business crossed the aggregate turnover threshold for GST registration. Taxpayers are required to file the application for new GST registration within 30 days from the date on which the liability to register arises.

Rule 14A: Opt-in for Simplified GST Registration (if eligible)

If you estimate that your monthly output tax liability on B2B supplies (i.e., to GST-registered customers) will not exceed ₹2.5 lakh, you can opt for simplified registration under Rule 14A.

- Select “Yes” for “Option for Registration under Rule 14A” (visible at the end of the Business Details tab).

- This option is voluntary and triggers Aadhaar authentication-based fast-track processing.

Note: Once opted, Aadhaar authentication for the Primary Authorised Signatory and at least one Promoter/Partner becomes mandatory, and only one registration per State/UT per PAN is allowed under Rule 14A.

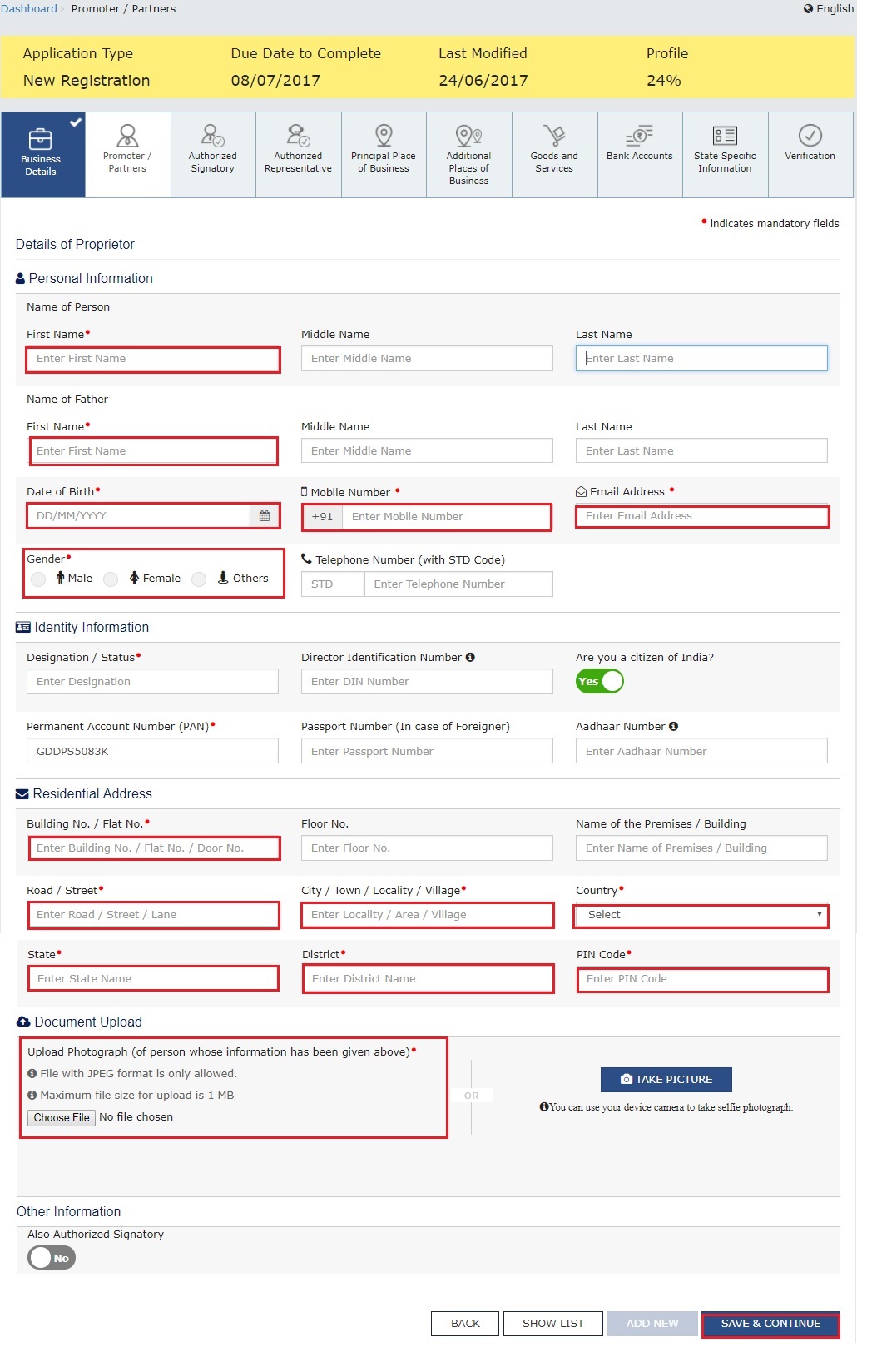

Step 7: Submit Promoter Information

In the next tab, provide promoters and directors information. In case of proprietorship, the proprietors' information must be submitted. Details of up to 10 Promoters or Partners can be submitted in a GST registration application. The following details must be submitted for the promoters:

- Personal details of the stakeholder like name, date of birth, address, mobile number, email address and gender.

- Designation of the promoter.

- DIN of the Promoter, only for the following types of applicants:

- Private Limited Company

- Public Limited Company

- Public Sector Undertaking

- Unlimited Company

- Foreign Company registered in India

In case the applicant provides Aadhaar, the applicant can use Aadhaar e-sign for filing GST returns instead of a digital signature.

Step 8: Submit Authorised Signatory Information

An authorised signatory is a person nominated by the promoters of the company. The nominated person shall hold responsibility for filing GST returns of the company. Further, the person shall also maintain the necessary compliance of the company. The authorised signatory will have full access to the GST Portal. The person shall undertake a wide range of transactions on behalf of the promoters.

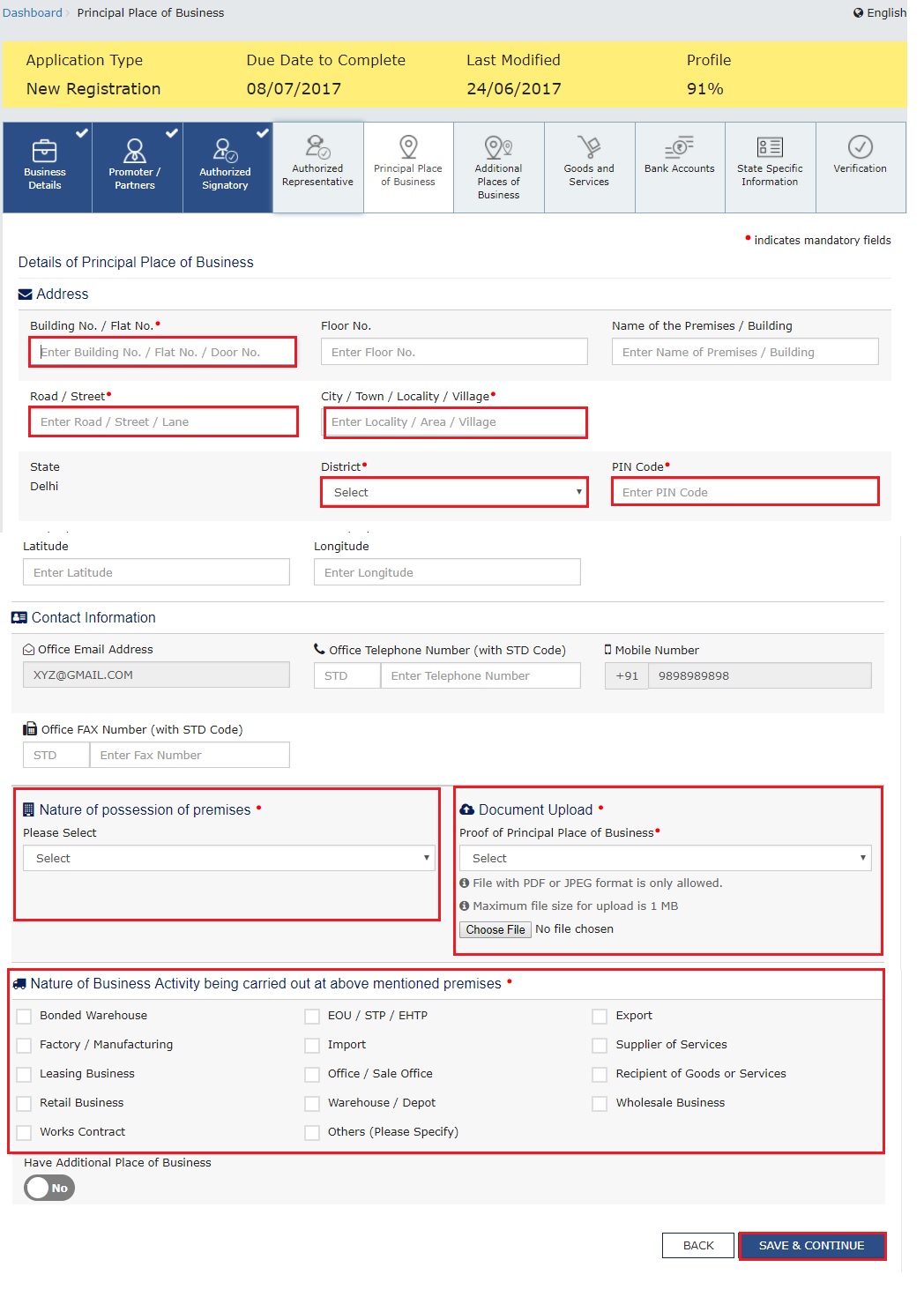

Step 9: Principal Place of Business

In this section of the Gst Registration Procedure, the applicant shall provide the details of the principal place of business. The Principal Place of Business acts as the primary location within the State where the taxpayer operates the business. It generally addresses the books of accounts and records. Hence, in the case of a company or LLP, the principal place of business shall be the registered office. For the principal place of business, enter the following:

- Address of the principal place of business.

- Official contact such as Email address, telephone number (with STD Code), mobile number field and fax number (with STD Code).

- Nature of possession of the premises.

If the principal place of business is located in SEZ or the applicant acts as SEZ developer, the necessary documents/certificates issued by the Government of India are required to be uploaded by choosing ‘Others’ value in Nature of possession of premises drop-down and uploading the document. In this section, upload documents to provide proof of ownership or occupancy of the property as follows:

- Own premises – Any document in support of the ownership of the premises, like the Latest Property Tax Receipt or Municipal Khata copy or a copy of the Electricity Bill.

- Rented or Leased premises – A copy of the valid Rent / Lease Agreement with any document in support of the ownership of the premises of the Lessor, like the Latest Property Tax Receipt or Municipal Khata copy or a copy of the Electricity Bill.

- Premises not covered above – A copy of the Consent Letter with any document in support of the ownership of the premises of the Consenter, like Municipal Khata copy or Electricity Bill copy. For shared properties, also, the same documents may also be uploaded.

Step 10: Additional Place of Business

Upon having an additional place of business, enter the details of the property in this tab. For instance, if the applicant is a seller on Flipkart or another e-commerce portal and uses the seller's warehouse, that location can be added as an additional place of business.

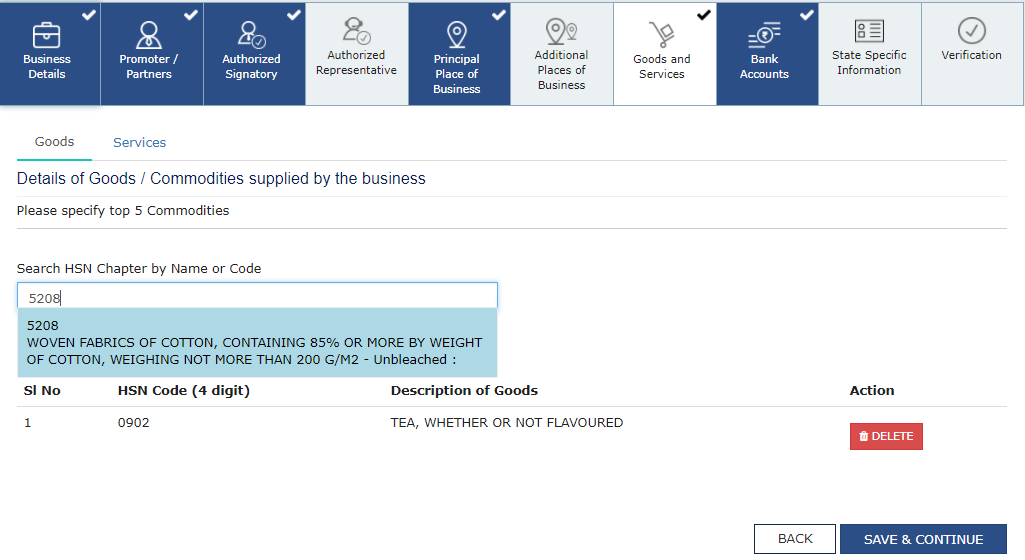

Step 11: Details of Goods and Services

In this section, the taxpayer must provide details of the top 5 goods and services supplied by the applicant. For goods supplied, provide the HSN code, and for services, provide the SAC code.

Click here to know more about the HSN code and SAC code.

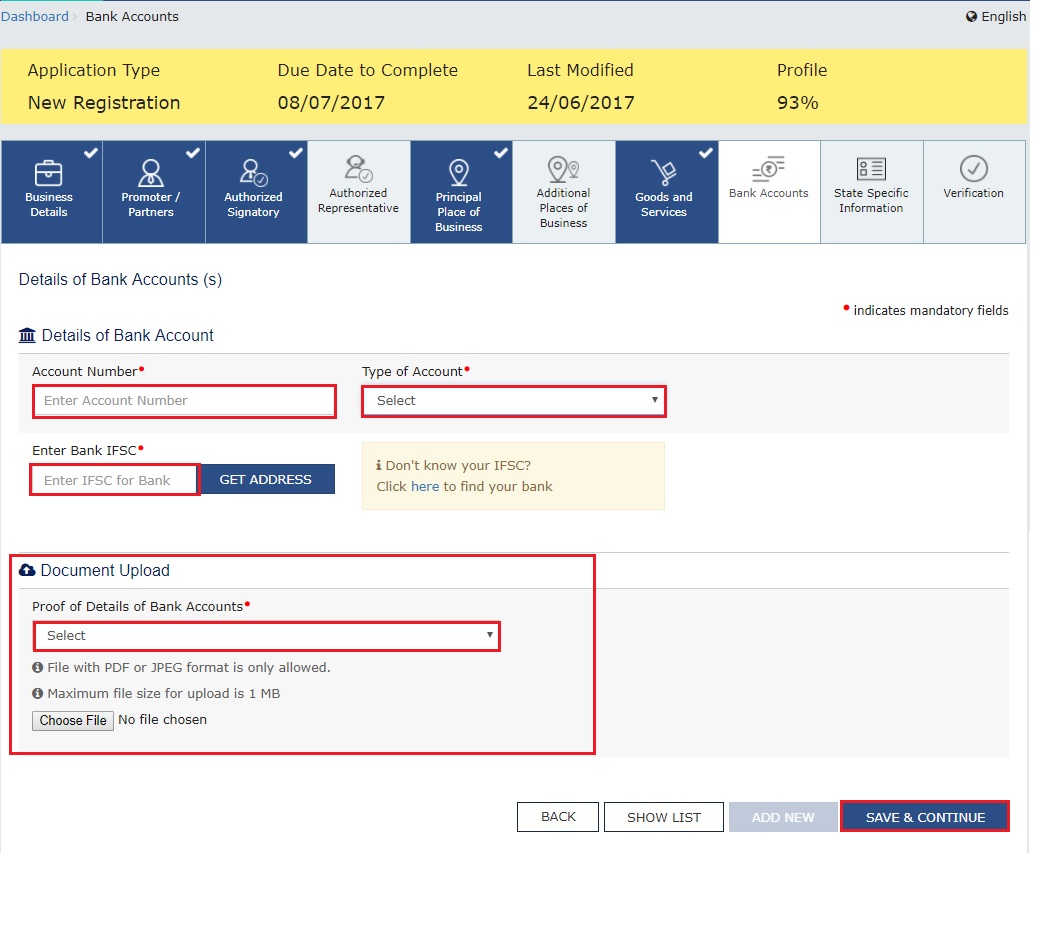

Step 12: Details of Bank Account

In this section, enter the number of bank accounts held by the applicant. If there are 5 accounts, enter 5. Then provide details of the bank account like account number, IFSC code and type of account. Finally, upload a copy of the bank statement or passbook in the place provided.

Step 13: Verification of Application

In this step, verify the details submitted in the application before submission. Once verification is complete, select the verification checkbox. In the Name of Authorised Signatory drop-down list, select the name of the authorised signatory. Enter the place where the form is filled. Finally, digitally sign the application using a Digital Signature Certificate (DSC)/ E-Signature or EVC. Digitally signing using DSC is mandatory in the case of LLPs and Companies.

Rule 9A: Automatic Registration within 3 Days

In addition to Rule 14A, Rule 9A enables automatic approval of your registration application within 3 working days, based on system-generated risk analysis.

If your application is low-risk (based on data validation, PAN/Aadhaar match, etc.), the system may auto-approve your GSTIN — even if you haven’t opted for Rule 14A.This benefits all applicants, including those applying under regular GST registration rules (Rules 8, 12, 17).

- Date of Commencement of Business: The actual date when your business started operations.

- Date on which liability to register arises: This is the date your turnover crossed the prescribed threshold (e.g., ₹20L/₹40L depending on business type and state).

- You must apply for registration within 30 days from this date.

Click here to know more about Rule 9A: Automatic Registration Within 3 Working Days

Step 14: ARN Generated

On signing the application, the success message is displayed. The acknowledgement shall be received in the registered e-mail address and mobile phone number. The Application Reference Number (ARN) receipt is sent to the e-mail address and mobile phone number. Using the GST ARN Number, the status of the application can be tracked. This 14-step process can help you with how to do GST registration.

Do businesses need separate GST registrations for each state of operation?

Yes, businesses need separate GST registrations for each state where they have a place of business and supply goods or services. This is because GST is state-specific, and each state's operations are treated as distinct entities for compliance purposes.

Simplify the GST registration process with IndiaFilings expert assistance!!