Chris John

Expert

Published on: Jun 24, 2026

Gstr 9a - GST Annual Report

GST registered taxpayers who have opted for the Composition Scheme under Goods and Services Tax (GST) are required to file GSTR-9A. Gstr 9a is a type of GST Annual Return that is expected to be filed once in a particular financial year. GSTR-9A includes all the information, submitted by the composition taxpayers, furnished in the quarterly return during a specific fiscal year. In this article, we look at the various aspects of GST annual return or Gstr 9a in detail.Eligibility

Every taxpayer registered under the composition levy scheme under

GST must file GSTR-9A. However, the following indivduals are not required to file Gstr 9a:- Input Service Distributor

- Non-Resident Taxable Individuals

- Individuals who pay Tax Deducted at Source (TDS) under Section 51 of the Income Tax Act.

- Casual Taxable Individuals

- E-Commerce operators who pay Tax Collected at Source (TCS) under Section 52 of the Income Tax Act.

Due Date Extended to 30th November 2019

The Government has decided to further extend the due date for filing various GSTR-9 forms for FY 2017-18 until 30th November 2019. This is applicable for GSTR-9, 9A & 9C forms.

Due Date for Filing Gstr 9a

The usual due date for filing GSTR-9A is on or before the 31st of December that follows the close of a certain financial year. For instance, assume a composition taxpayer is to file GSTR-RA for the FY 2017-2018. The taxpayer is required to file Gstr 9a on or before the 31st of December of the year 2018.

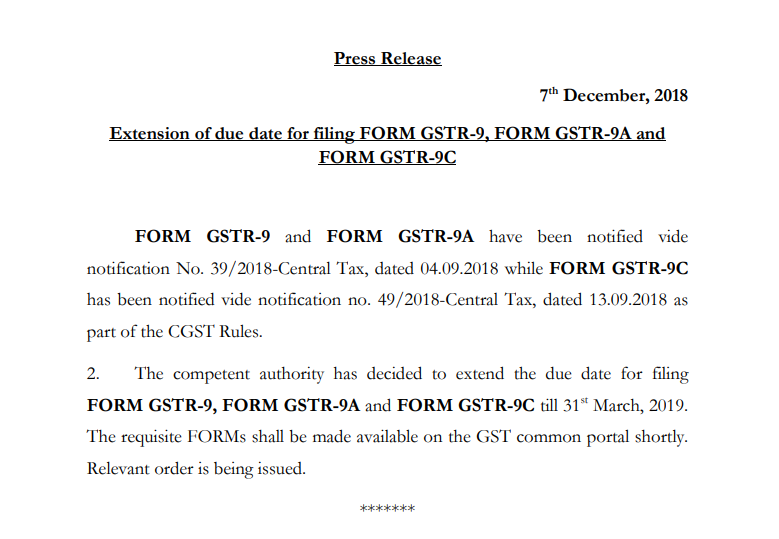

However, as per the latest press release, on the 7th of December, 2018, the Central Board of Indirect Taxes and Customs has extended the due date for filing Gstr 9a to 31st of March, 2019. A copy of the press release is reproduced below for reference: Due Date Extension Press Release for Gstr 9a

Due Date Extension Press Release for Gstr 9a

Details for Filing Gstr 9a

While filing Gstr 9a, the taxpayer would be required to furnish the following information:

Part-I of Gstr 9a

Basic details such as the GSTIN, Trade Name and Legal Name of the taxpayer would be auto-populated on the GST Portal.

Part-II of Gstr 9a

Information on the outward and inward supplies that are declared in GSTR-4 that was filed during the financial year. This would comprise of the summary from all the quarterly returns filed during the fiscal year.

Part-III of Gstr 9a

Information of the tax paid as declared in the returns filed during the certain financial year. Taxes paid under different heads such as the IGST, SGST, CGST, Cess, Interest, Penalty and Late Fee has to be mentioned here.

Part-IV of Gstr 9a

Some specifics on particular transactions for the previous fiscal year that were declared in the returns of April to September of the current FY or up to the date of filing of annual return, whichever may be earlier. This section would comprise of the summary of the corrections or amendments concerning to the entries of previous FY. It may be omissions or additions.

Part-V of Gstr 9a

Various information such as the following:

- Specifics of Demands and Refunds. Here, the details of any other demands from the tax department regarding tax, tax paid on a demand raised, any balance to be paid should be mentioned. Similarly, all the details of the Refunds claimed, refunds received out of a claim or any pending refund shall be mentioned.

- The details of credit reversed or availed. If a taxpayer switches from a regular to a composition scheme or vice versa, ITC should be reversed or added accordingly. Such details concerning to ITC should be entered here.

- Any Delay fee payable and paid. Any late fee on the account of delayed payments of tax or late filing of returns should be mentioned in this section.

Penalty

The penalty for delayed filing of Gstr 9a will incur charges based on the delay as follows:

- Under Central Goods and Services Tax: INR 100 per day of default.

- Under State Goods and Services Tax: INR 100 per day of default.