IndiaFilings

Expert

Published on: Apr 22, 2026

Composition GST Scheme acts as an alternative method for levying a tax under GST. Small businesses registered under the GST composition scheme can pay GST at a fixed rate of turnover every quarter and file quarterly GST returns. Composition levy would be generally related to small taxpayers who are supplying goods and services or both to the end consumer with low turnover. Further, the composition GST scheme has been designed with the aim of making compliance more accessible and cost-effective for the taxpayers. In this article, let us look at the composition scheme in GST, composition scheme limit and composition scheme GST rate in detail. Any existing taxpayer whose annual turnover did not cross the Rs.1.5 crore threshold of Rs.75 lakhs in the preceding financial year. In the case of states under a special category, except Jammu & Kashmir and Uttarakhand, the limit of GST composition scheme turnover limit has increased from Rs.50 lakhs to Rs.75 lakhs. Hence, the Ministry provided the GST composition scheme turnover limit threshold for Jammu & Kashmir and Uttarakhand as Rs.1 crore and must register under the composition scheme under GST. The following conditions must be satisfied to avail of this composition levy scheme after meeting the GST composition scheme turnover limit. The submission of various forms under the Composition GST Scheme Rules is meant for specific reasons. The list of forms under Composition GST Scheme Rules with the purposes and due dates are tabulated below for the reference. The validity of the composition GST scheme will depend upon the option exercised by a taxable person to pay tax to remain valid so long as all the conditions are fulfilled as specified in the law. However, individuals who are eligible for the composition GST scheme can choose to opt-out of it by simply filing an application. The taxpayers must follow the below steps to Opt for the Composition Levy on the GST Portal, if they are meeting the GST composition scheme turnover limit:GST Composition Scheme

Eligibility Criteria & GST Composition Scheme turnover limit

Composition Scheme Limit for Special Eligibility

Conditions for Availing Composition GST Scheme

Rules on Composition Scheme under GST – Compliance

S.No.

Forms to be Filed

Description

Due Date

1

Form GST CMP 01

Intimation of willingness to opt for the scheme

Within 30 days

2

Form GST CMP 02

Information pertaining to stock and inward supplies from unregistered individuals

Prior to the commencement of the Financial year

3

Form GST CMP 03

Intimation of withdrawal from the scheme

Within 60 days of the exercise of an option

4

Form GST CMP 04

Show-cause notice on contravention of the Act or rules by the proper officer

Within seven days of the occurrence of the event

5

Form GST CMP 05

The replies to show cause notice

On contravention

6

Form GST CMP 06

An issue of order

Within 15 days

7

Form GST CMP 07

Registration under the Composition GST Scheme

Within 30 days

8

Form GST REG 01

Information of inputs in the stocks finished or semi-finished goods

Prior to the appointed date

9

Form GST ITC 01

Intimation of ITC available

Within 30 days of the option withdrawn

10

Form GST ITC 13

Intimation of willingness to opt for the composition GST scheme

Within 60 days of the commencement of the Financial year

Validity of Composition Scheme Levy

Online Application Procedure for Composition Scheme in GST

Visit GST Portal

Step 1: Firstly, the taxpayers have to visit theGST portal to Opt for the Composition Levy online.

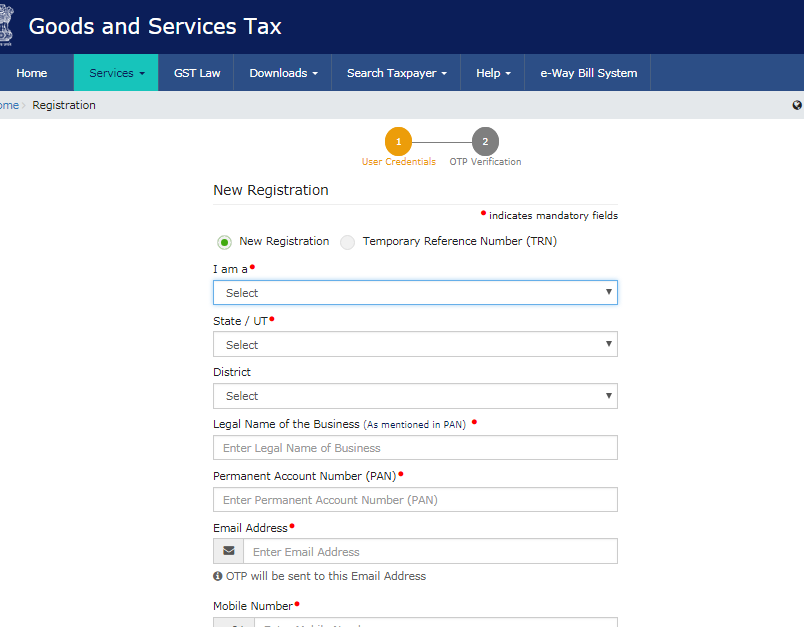

Step 2: The applicant shall click on the New Registration under the services tab that is visible on the home page. The following application procedure for composition scheme in GST is of two parts:

Step 2: The applicant shall click on the New Registration under the services tab that is visible on the home page. The following application procedure for composition scheme in GST is of two parts:

New Registration

Step 3: By clicking on the New Registration radio button, the new registration page is displayed.

Step 3 - GST Composition Levy Scheme

Step 3 - GST Composition Levy Scheme

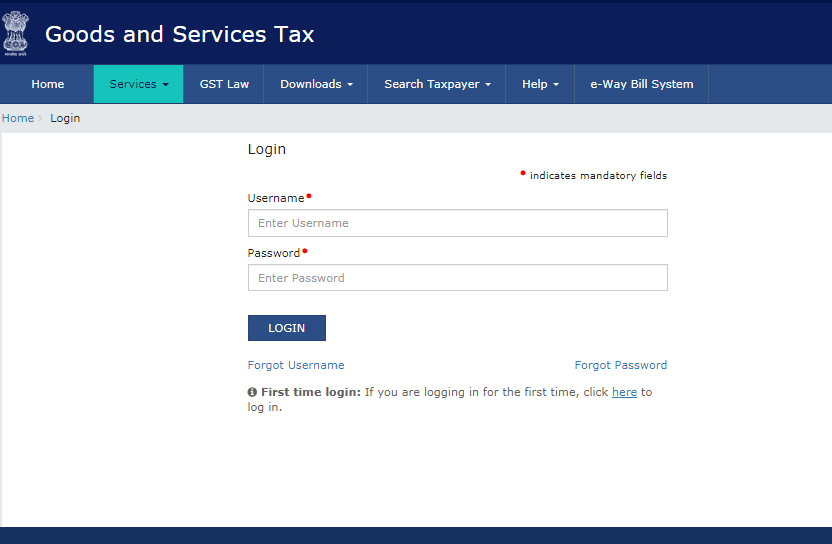

Login into Portal

Step 4: Click on the ‘Login’ button to access the username and password page.

Step 5: Enter the correct ‘Username’ and ‘Password’ credentials along with the captcha in the required field and then click ‘login.’

Step 5: Enter the correct ‘Username’ and ‘Password’ credentials along with the captcha in the required field and then click ‘login.’

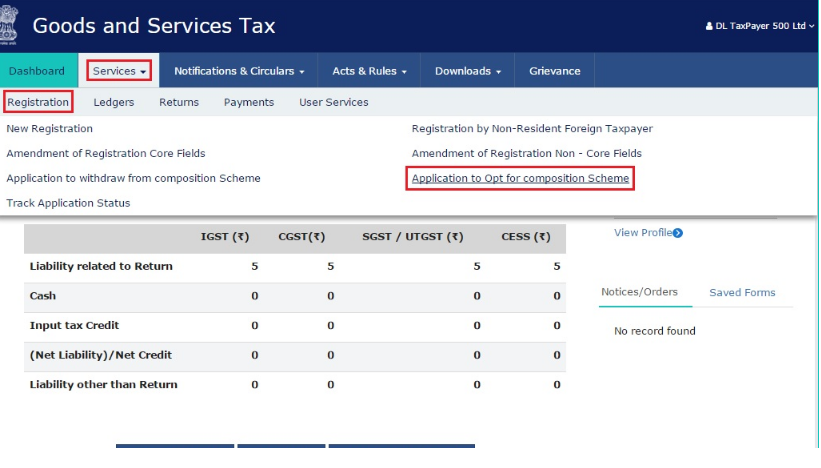

Application to Opt for Composition Levy

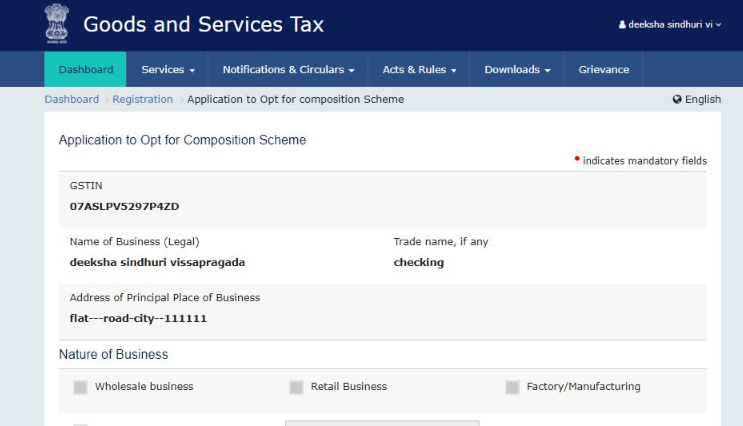

Step 6: After logging in, the applicant shall then select ‘Application to Opt for Composition Levy’ from the Registration Menu under the service tab that is visible on the home page to initiate the composition scheme in GST registration.

Step 7: The page shall redirect to the new page, where the Application to Opt for Composition Levy page will be displayed with the following details:

Step 7: The page shall redirect to the new page, where the Application to Opt for Composition Levy page will be displayed with the following details:

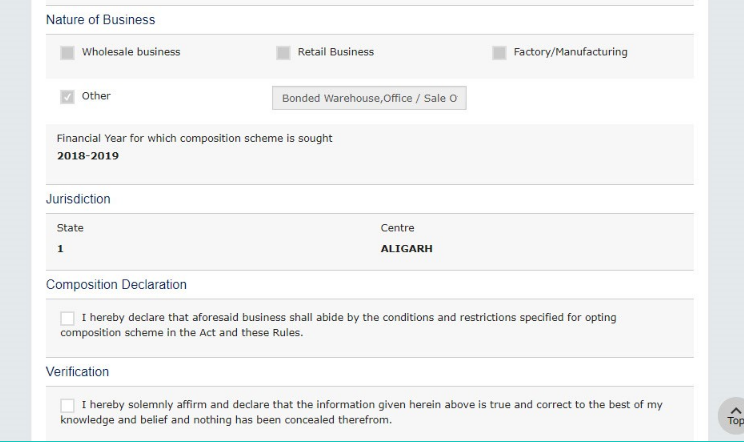

Step 8: Below these details, the Nature of business and Jurisdiction will be listed, as shown below:

Step 8: Below these details, the Nature of business and Jurisdiction will be listed, as shown below:

Step 9: Below these details, the page shall exhibit the Composition Declaration. The applicant must then check to pledge to abide by the rules and conditions for the Taxpayers who are under the Composition Levy.

Step 9: Below these details, the page shall exhibit the Composition Declaration. The applicant must then check to pledge to abide by the rules and conditions for the Taxpayers who are under the Composition Levy.

Verification Process

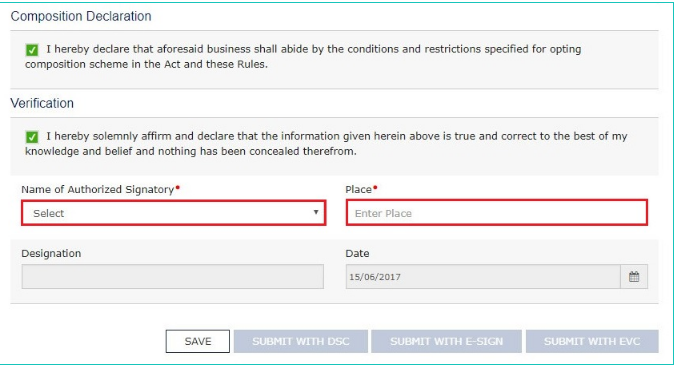

Step 10: Before submitting the application, the applicant must also check the box for the Verification process (below the Composition Declaration) that states that all the information given is true and that nothing has been concealed from the authority.

Step 11: Finally, the applicant shall select the Authorized Signatory from the drop-down menu.

Step 12: Enter the place where the application is filed in the Place field.

Step 13: Click the ‘save’ button to save the application form and retrieve it later.

Step 11: Finally, the applicant shall select the Authorized Signatory from the drop-down menu.

Step 12: Enter the place where the application is filed in the Place field.

Step 13: Click the ‘save’ button to save the application form and retrieve it later.

Submit the Application

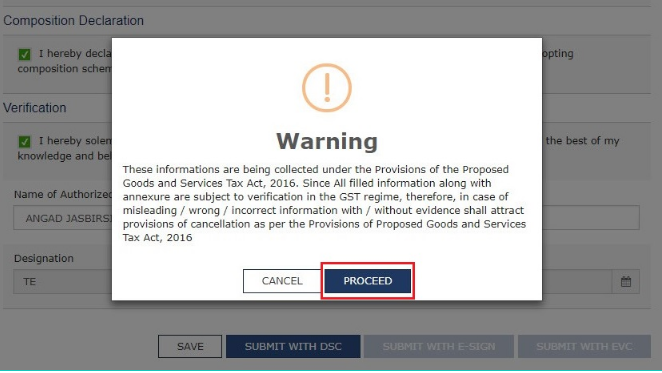

Step 14: The options to submit the form gets activated after selecting the Authorized Signatory and the Place.

Step 15: Sign the form by using either the Digital Signature Certificate (DSC) or the EVC option. On selecting any of these options below, the applicant shall then receive an OTP.

Using DSC Option

Step 16: If using a DSC, the applicant will be required to select the registered DSC from the emSigner pop-up screen and then proceed from there accordingly.

Using EVC Option

Step 17: Enter the OTP and then click on the Validate OTP button.

Step 18: The page will display a prompt to confirm the action. Click on Proceed to move forward to register on the composition scheme under GST.

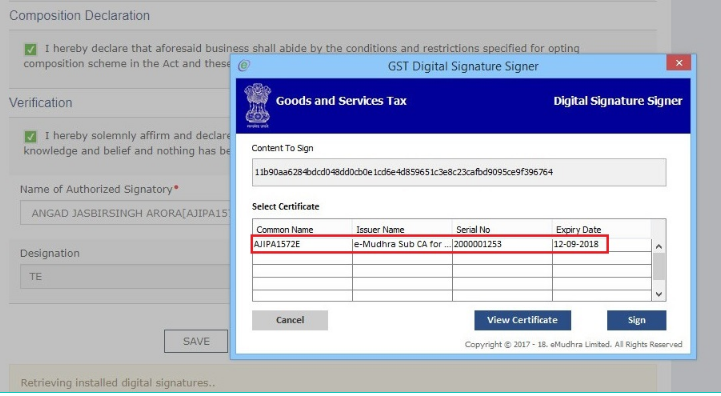

Digital Signature Signer

Step 19: The system retrieves the installed digital signatures available using the emSigner. The applicant shall receive a pop-up message to select the desired DSC. After receiving the pop-up message, select the desired signature to receive the confirmation message.

Step 19 - GST Composition Levy Scheme

Step 19 - GST Composition Levy Scheme

Acknowledgement Message

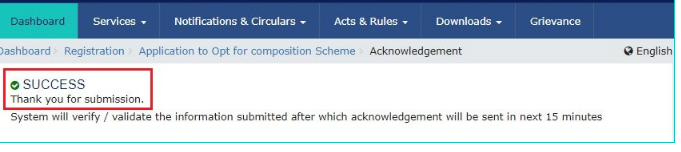

Step 20: On successfully filing the application for cancellation of registration, the system shall then generate the ARN and display a confirmation message.

Step 21: GST Portal also sends a confirmation message to the registered mobile phone number and email.

Step 22: On successfully filing the application to Opt for the Composition Levy, the system generates the ARN for the work item. The ARN shall generate and sends the link to the registered email and SMS within the next 15 minutes.

Conclusion

The Composition Scheme simplifies compliance for small businesses with reduced tax composition scheme GST rates and minimal filing requirements. The composition scheme GST rate offers a cost-effective solution, allowing eligible taxpayers to focus on growth while adhering to regulations. However, businesses must consider the composition scheme limit and evaluate its restrictions, such as the ineligibility for input tax credit and supply limitations, to determine its suitability.