IndiaFilings

Expert

Published on: Apr 22, 2026

GSTR 1 Return Filing

GSTR 1 return must be filed by all persons

registered under GST. GSTR 1 return is due on the 10th of each month for taxpayers who have a turnover of more than Rs.1.5 crores. GSTR 1 is due every quarter for taxpayers having less than Rs.1.5 crores turnover. From the month of October 2017, the normal schedule for filing GSTR 1 return will continue. In this article, we continue to look at the procedure for preparing and filing GSTR 1 return. Read the first article, to know more about how to prepare details of outward supplies for GSTR 1. In this article, we look at the procedure for preparing GSTR 1 return, wherein amendments were applicable.Late Fee Waiver & Extended Due Date

As per the latest notification from the Ministry of Finance (Notification No.74/2019-Central Tax), the late fee is waived for the registered persons who have not provided the details on outward supplies in Form GSTR-1 for the period of July 2017 to November 2019. But, they should have furnished the details for the period between 19th December and 10th January 2020. The exact text from the notification is provided below: “Provided also that the amount of late fee payable under section 47 of the said Act shall stand waived for the registered persons who failed to furnish the details of outward supplies in FORM GSTR-1 for the months/quarters from July, 2017 to November, 2019 by the due date but furnishes the said details in FORM GSTR-1 between the period from 19th December, 2019 to 10th January, 2020.” The notification can be accessed from:

Also, the due date for filing Form GSTR-1 for the month of November 2019 is extended to businesses having turnover of more than 1.5 crores in the States of Assam, Manipur or Tripura is extended to 31st December 2019 through a separate notification from the Ministry of Finance (Notification No.76/2019-Central Tax). The exact text is provided below: “Provided that for registered persons whose principal place of business is in the State of Assam, Manipur or Tripura, the time limit for furnishing the details of outward supplies in FORM GSTR-1 of Central Goods and Services Tax Rules, 2017, by such class of registered persons having aggregate turnover of more than 1.5 crore rupees in the preceding financial year or current financial year, for the month of November, 2019 till 31st December, 2019.” The notification can be assessed below:

No Late Fee for GSTR-1 & GSTR-3B Return

The biggest relief extended to small business by the 31st GST Council is the waiver of late fee for filing GSTR-1 and GSTR-3B return. The GST Council has announced: “Late fee shall be completely waived for all taxpayers in case FORM GSTR-1, FORM GSTR-3B & FORM GSTR-4 for the months/quarters July 2017 to September 2018, are furnished after 22.12.2018 but on or before 31.03.2019.” Thus, filing of Form GSTR-1, GSTR-3B and GSTR-4 will not attract any late fee penalty until 31st March 2019.

GST Annual Return Due Date Extended

All entities having GST registration are required to file GST annual return in form GSTR-9. The due date for filing GST annual return is usually 31st December of each year for the financial year ended on 31st March of the same calendar year. As GST is newly introduced in India, the Government has decided to extend the due date for GST annual return filing to 30th June 2019. The due date for filing GST annual return was originally extended upto 31st March 2019, which has been further extended to 30th June 2019 by the GST Council.

Due Dates Modified

The Government has recently deferred the due date for filing GSTR 1 from the 11

th of April to the 13th. Apart from this, the following are the due dates for filing GSTR 1 for the months of April, May and June 2019:- April 2019 – 11th May 2019

- May 2019 – 11th June 2019

- June 2019 – 11th July 2019

It can be inferred from the above that the due dates for filing these returns fall on the 11

th of every succeeding month of filing. The deadline for the filing quarterly GSTR 1 for the quarter of April-June is 31st July 2019.Import of E-way Bill Data

It is essential for taxpayers to validate the data of their transactions before proceeding with the process of filing returns, as it saves time and unnecessary data entry. To cater to this purpose, the GST portal has now been integrated with the E-way Bill Portal (EWB). The integration enables the users to import the B2B and B2C invoice sections and the HSN-wise-summary of outward supplies section. Using these details, the taxpayers may verify the data and complete the filing. The feature has been introduced considering the major data gaps between self-declared liability in Form GSTR-1 and Form GSTR-3B. A similar rule also applies to Input Tax Credit (ITC) claimed in GSTR-3B, as it could be compared with the credit available in Form GSTR-2A. Data validation and comparison can be pursued through the following tabs of the portal:

- Liability other than export/reverse charge

- Liability due to reverse charge

- Liability due to export and SEZ supplies.

- ITC credit claimed and due

On a more precise note, the newly launched facility takes away the taxpayer’s need to make specifications connected with the e-way bill transactions specified in GSTR-3B as it allows the taxpayers to import data in Form GSTR-1 for all invoices for which the e-way bill has been generated. The particulars imported would include the details of supplier, receiver, invoice number, the date of invoice, the type and quantity of goods, HSN Code, etc. These details are then transferred to the GST portal and classed into three categories to be used in GSTR-1 – namely, Business to Business Supplies (B2B), Business to Consumer (B2C) supplies (covering values of above Rs. 2.5 lakhs) and HSN (Harmonized System of Nomenclature Code for goods and services) wise consolidated supply data.

How to prepare GSTR 1 Return?

GSTR-1 return can be easily prepared using LEDGERS GST Software. Once the GSTR-1 return is prepared, it can be filed online in the

GST Portal. As the taxpayer must provide details of supplies under various categories in the GSTR-1 return, the process can be simplified using a GST software.[crumina_label style="success" ]Prepare GSTR 1 using LEDGERS GST Software[/crumina_label]

Amendments to Taxable Supplies

In the section shown below, details of amendments to taxable outward supply details furnished in returns for earlier tax periods in Table 4, 5 and 6 [including debit notes, credit notes, refund vouchers issued during current period and amendments thereof]. Table 4, 5 and 6 contain details of outward supplies made by the taxpayer as follows:

- Table 4: Taxable outward supplies made to registered persons (including UIN-holders) other than supplies covered by Table 6

- Table 5: Taxable outward inter-State supplies to unregistered persons where the invoice value is more than Rs 2.5 lakh

- Table 6: Zero rated supplies and Deemed Exports

GSTR 1 Amendments to taxable supplies

GSTR 1 Amendments to taxable supplies

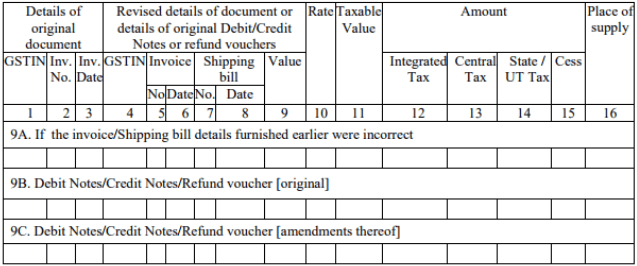

Amendments to Invoice or Shipping Bill

9A. If the invoices/Shipping bill details furnished earlier were incorrect, is applicable if the taxpayer issued revised invoice or revised shipping bill during the current tax period. For example, if a taxpayer issued an invoice to a taxpayer for Rs.1 lakh in the month of July and filed GSTR 1 return on the 10th August and discovered an error on 15th of August, then a revised invoice can be issued in August. In the GSTR 1 return filed in September, the details of the original invoice issued in July and details of revised invoice issued in August must be filed with the following information:

- GSTIN of customer mentioned in the original invoice

- Original invoice date

- Original invoice number

- GSTIN of customer mentioned in the revised invoice

- Revised invoice date

- Revised invoice number

- Revised shipping bill date, if applicable

- Revised shipping bill number, if applicable

- Revised invoice value

- Revised invoice rate

- Revised invoice taxable value

- Revised invoice IGST applicable

- Revised invoice CGST applicable

- Revised invoice SGST applicable

- Revised invoice GST Cess applicable

- Place of supply mentioned on the revised invoice.

Debit Notes/Credit Notes/Refund Vouchers [Original]

Following the details of amendments to invoice or shipping bill, details of debit notes, credit notes and refund vouchers issued must be provided. Debit notes and credit notes are issued under GST in case of refund or returns.

Debit Notes/Credit Notes/Refund Vouchers [Amendments]

In case there were any amendments to debit notes, credit notes or refund vouchers, the details of such amendments must be provided under 9C. Debit Notes/Credit Notes/Refund voucher [amendments thereof].

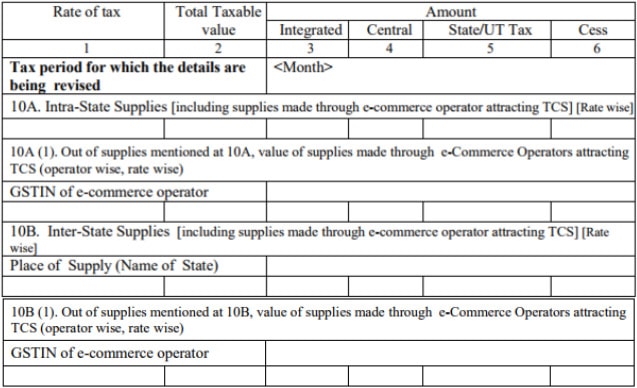

Amendments to Outward Supplies to Unregistered Persons

GSTR 1 Amendments to Invoice

In the table above, details of all amendments to taxable outward supplies to unregistered persons should be furnished. Hence, the table above is used for correcting invoices for which details were furnished under GSTR 1 Table 7, Taxable supplies (Net of debit notes and credit notes) to unregistered persons other than the supplies covered in Table 5. GSTR 1 Table 5 relates to Taxable outward inter-state supplies to unregistered persons where the invoice value is more than Rs 2.5 lakh.

In this section, only details of amendments must be provided along with the tax period for which the details are being revised. Further, the amendments must be provided rate-wise and e-commerce operator wise in case of supplies made through e-commerce operator. In the section amendments to outward supplies to unregistered persons, the following information must be provided:

GSTR 1 Amendments to Invoice

In the table above, details of all amendments to taxable outward supplies to unregistered persons should be furnished. Hence, the table above is used for correcting invoices for which details were furnished under GSTR 1 Table 7, Taxable supplies (Net of debit notes and credit notes) to unregistered persons other than the supplies covered in Table 5. GSTR 1 Table 5 relates to Taxable outward inter-state supplies to unregistered persons where the invoice value is more than Rs 2.5 lakh.

In this section, only details of amendments must be provided along with the tax period for which the details are being revised. Further, the amendments must be provided rate-wise and e-commerce operator wise in case of supplies made through e-commerce operator. In the section amendments to outward supplies to unregistered persons, the following information must be provided:

- 10A. Intra-State Supplies [including supplies made through e-commerce operator attracting TCS] [Rate wise]

- 10A (1). Out of supplies mentioned at 10A, value of supplies made through e-Commerce Operators attracting TCS (operator wise, rate wise)

- 10B. Inter-State Supplies [including supplies made through e-commerce operator attracting TCS] [Rate wise]

- 10B (1). Out of supplies mentioned at 10B, value of supplies made through e-Commerce Operators attracting TCS (operator wise, rate wise)

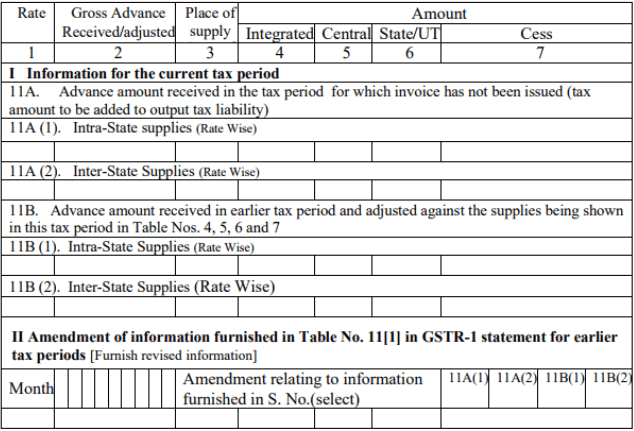

Statement of Advances Received

GSTR 1 Statement of Advances Received

Under GST, a receipt voucher is issued by the taxpayer whenever advance payment is taken for supply of goods or services. A receipt voucher or advance receipt can be issued when payment is received but the supply of goods or services has not yet started. Details of all receipt voucher issued by the taxpayer must be submitted under the head "Consolidated Statement of Advances Received/Advance adjusted in the current tax period/ Amendments of information furnished in earlier tax period" in GSTR 1 return.

In this section, details of all advance payment received by the taxpayer must be provided under the following heads:

GSTR 1 Statement of Advances Received

Under GST, a receipt voucher is issued by the taxpayer whenever advance payment is taken for supply of goods or services. A receipt voucher or advance receipt can be issued when payment is received but the supply of goods or services has not yet started. Details of all receipt voucher issued by the taxpayer must be submitted under the head "Consolidated Statement of Advances Received/Advance adjusted in the current tax period/ Amendments of information furnished in earlier tax period" in GSTR 1 return.

In this section, details of all advance payment received by the taxpayer must be provided under the following heads:

- Rate of tax

- Gross or adjusted amount of advance received

- Place of supply

- Amount of IGST applicable

- Amount of CGST applicable

- Amount of SGST applicable

- Amount of GST cess applicable

For the previous month, the above data must be submitted under the following categories in GSTR 1 return:

- Advance amount received in the tax period for which invoice has not been issued (tax amount to be added to output tax liability)

- Intra-State supplies (Rate Wise)

- Inter-State Supplies (Rate Wise)

- Intra-State supplies (Rate Wise)

Finally, in case there are changes to the above section for which return was filed previously, then such details must be provided under "Amendment of information furnished in Table No. 11[1] in GSTR-1 statement for earlier tax periods [Furnish revised information]".

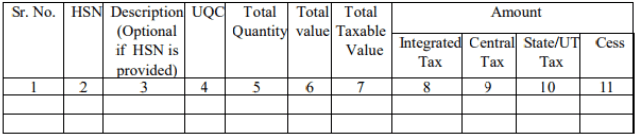

GSTR 1 HSN Summary

GSTR 1 HSN Summary

All entities with a taxable turnover of over Rs.1.5 crores are required to mandatorily declare HSN or SAC code on the tax invoice. In GSTR 1 the taxpayer must file details of all supply along with HSN code. The following information must be declared under HSN-wise summary of outward supplies:

GSTR 1 HSN Summary

All entities with a taxable turnover of over Rs.1.5 crores are required to mandatorily declare HSN or SAC code on the tax invoice. In GSTR 1 the taxpayer must file details of all supply along with HSN code. The following information must be declared under HSN-wise summary of outward supplies:

- HSN Code

- Description, if HSN is not provided

- UQC

- Total quantity

- Total value

- Total taxable value

- Amount of IGST applicable

- Amount of CGST applicable

- Amount of SGST applicable

- Amount of GST Cess applicable

Know more about the requirement for displaying

HSN code on invoices.Documents Issued During the Tax Period

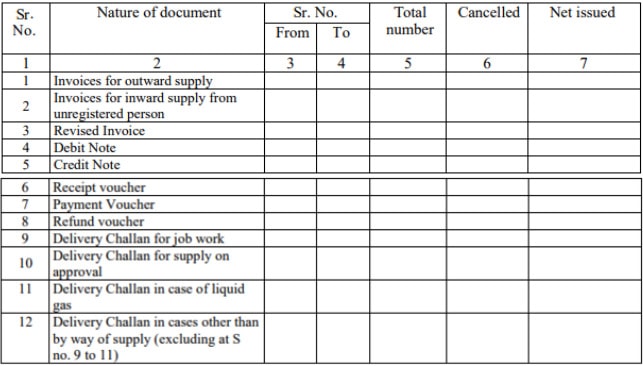

GSTR 1 Documents Issued

Finally, the GST taxpayer must provide details of all GST related documents issued during the taxpayer with from and to serial number, total number issued, total cancelled and net issued during the tax period. Details of the following documents issued must be provided in GSTR 1 filing.

GSTR 1 Documents Issued

Finally, the GST taxpayer must provide details of all GST related documents issued during the taxpayer with from and to serial number, total number issued, total cancelled and net issued during the tax period. Details of the following documents issued must be provided in GSTR 1 filing.

- Invoices for outward supply

- Invoices for inward supply from unregistered persons

- Revised invoice

- Debit note

- Credit note

- Receipt voucher

- Payment voucher

- Refund voucher

- Delivery challan for job work

- Delivery challan for supply on approval

- Delivery challan in case of liquid gas

- Delivery challan in case other than by way of supply