IndiaFilings

Expert

Published on: Apr 22, 2026

GSTR 1 Return Format 2019-2020

GSTR 1 return is due on the 11th of every month. After filing GSTR 3B returns, registered taxpayers belonging to all business shall file GSTR 1 return. The applicable taxpayers shall file GSTR 1 every month. The Form contains the details of outward supplies as performed by the business entity. In this article, we look at the procedure for filing GSTR 1 return along with the format.

Due Dates for 2020

The Ministry of Finance classified the filing of GSTR 1 into two categories:

|

S.No. |

Applicable for |

Month |

Due Date |

|

1 |

For taxpayers having an aggregate turnover of up to Rs.1.5 cr |

January - March 2020 |

April 30th 2020 |

|

2 |

For taxpayers having an aggregate turnover exceeding Rs.1.5 cr |

Feburary 2020 |

March 11th 2020 |

Due Dates Modified for 2019

The following modified due date for the year 2019 shall apply to registered taxpayers with a turnover of above Rs.1.5 cr.:

- April 2019 – 11th May 2019

- May 2019 – 11th June 2019

- June 2019 – 11th July 2019

- July 2019 – 11th August 2019

- August 2019 – 11th September 2019

- September 2019 – 11th October 2019

- October 2019 – 11th November 2019

- November 2019 – 11th December 2019

It can be inferred from the above that the due dates for filing these returns fall on the 11

th of every succeeding month of filing. The deadline for the filing quarterly GSTR 1 for the quarter of April-June is 31st July 2019.Import of E-way Bill Data

It is essential for taxpayers to validate the data of their transactions before proceeding with the process of filing returns, as it saves time and unnecessary data entry. To cater to this purpose, the GST portal has now been integrated with the E-way Bill Portal (EWB). The integration enables the users to import the B2B and B2C invoice sections and the HSN-wise-summary of outward supplies section. Using these details, the taxpayers may verify the data and complete the filing. The feature has been introduced considering the major data gaps between self-declared liability in Form GSTR 1 and Form GSTR 3B. A similar rule also applies to Input Tax Credit (ITC) claimed in GSTR 3B, as it could be compared with the credit available in Form GSTR 2A. Data validation and comparison can be pursued through the following tabs of the portal:

- Liability other than export/reverse charge

- Liability due to reverse charge

- Liability due to export and SEZ supplies.

- ITC credit claimed and due

On a more precise note, the newly launched facility takes away the taxpayer’s need to make specifications connected with the e-way bill transactions specified in GSTR 3B as it allows the taxpayers to import data in Form GSTR 1 for all invoices for which the e-way bill has been generated. The particulars so imported would include the details of the supplier, receiver, invoice number, the date of invoice, the type and quantity of goods, HSN Code, etc. These details are then transferred to the GST portal and classed into three categories to be used in GSTR 1 – namely, Business to Business Supplies (B2B), Business to Consumer (B2C) supplies (covering values of above Rs.2.5 lakhs) and HSN (Harmonized System of Nomenclature Code for goods and services) wise consolidated supply data. Taxpayers with more than 50 invoices but not more than 500 may download the data of the sections mentioned above in the ‘CSV’ file format, which can be imported into the GSTR1 offline tool. The form could then be filed through the offline tool after adding sufficient data and generating a JSON file, which can be uploaded on to the GST portal. If the number of invoices is above 500, the invoice details pertaining to these sections can be imported from the ‘Return’ Dashboard on the GST portal as a zip file. This can later be unzipped to three files and extracted in Excel format. The taxpayer may then add more invoices and fill the other sheets to upload in the offline tool.

No Late Fee for GSTR-1 & GSTR-3B Return

The biggest relief extended to small business by the 31st GST Council is the waiver of late fee for filing GSTR-1 and GSTR-3B return. The GST Council has announced: “Late fee shall be completely waived for all taxpayers in case FORM GSTR-1, FORM GSTR-3B &FORM GSTR-4 for the months/quarters July 2017 to September 2018, are furnished after 22.12.2018 but on or before 31.03.2019.” Thus, filing of Form GSTR-1, GSTR-3B and GSTR-4 will not attract any late fee penalty until 31st March 2019.

GST Annual Return Due Date Extended

All entities having GST registration are required to file GST annual return in form GSTR-9. The due date for filing GST annual return is usually 31st December of each year for the financial year ended on 31st March of the same calendar year. As GST is newly introduced in India, the Government has decided to extend the due date for GST annual return filing to 30th June 2019. The due date for filing GST annual return was originally extended upto 31st March 2019, which has been further extended to 30th June 2019 by the GST Council.

Who should file GSTR 1 Return?

GSTR 1 must be filed by all regular taxpayers having

GST registration. Only dealers registered under Composition Scheme, Non-Resident Taxable person and casual taxable persons are not required to file GSTR 1 return.What is the due date for filing GSTR 1 Return?

GSTR 1 return must be filed on or before the 11th of each month. In the GSTR 1 return, the taxpayer would provide details of all supplies made during the previous month. Hence, in the GSTR 1 return filed on December, details of outward supplies in the month of November would be submitted.

What is the penalty for not filing GSTR 1 Return?

If a taxpayer does not file GSTR 1 return on or before the due date, penalty of Rs.20 shall apply for nil returns. For other taxpayers, Rs.50 shall apply per day. The penalty shall max up to Rs.10000.

GSTR 1 Format

In the following sections, we have broken down the GSTR 1 format into various sections to help you prepare GSTR 1 return. Instead of preparing the return manually, you can also click on the link below to signup for LEDGERS and prepare the GSTR 1 return automatically using the GST software.

[crumina_label style="success" ]Prepare GSTR 1 using LEDGERS GST Software[/crumina_label]

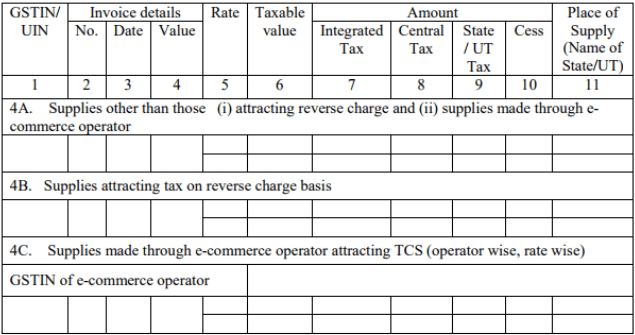

Taxable Supplies Made to Registered Persons

In the first table of the GSTR 1 return, as shown below, details of taxable supplies made to registered persons including UIN holders must be provided. Registered taxpayer is anyone having a GST registration and UIN holder is an embassy and consulate having

GST Unique ID. Taxable Supplies Made to Registered Persons

In the first table, the following information must be provided for each of the GST invoice issued by the taxpayer to a person having GSTIN (i.e., B2B Transaction) during the previous month.

Taxable Supplies Made to Registered Persons

In the first table, the following information must be provided for each of the GST invoice issued by the taxpayer to a person having GSTIN (i.e., B2B Transaction) during the previous month.

- GSTIN or UIN of the Customer

- Invoice Number

- Invoice Date

- Invoice Value

- GST Rate

- Taxable Value

- Amount of IGST Applicable

- Amount of CGST Applicable

- Amount of SGST Applicable

- Amount of GST Cess Applicable

- Place of Supply

In the second table, the same information as above must be provided. However, the information provided would relate to invoices where

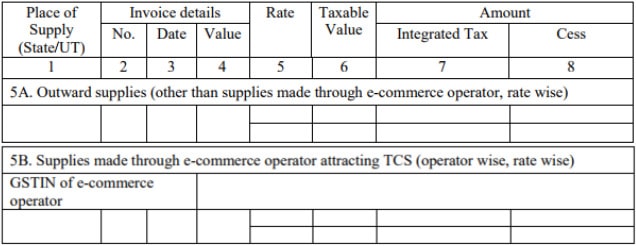

reverse charge is applicable. If reverse charge is applicable for an invoice, then the customer would be liable for payment of GST. In the third table, the invoice details of all supplies made through an e-commerce operator must be provided. In this table, GSTIN of the customer and the GSTIN of the e-commerce operator should be provided along with invoice number, invoice date, invoice value and other data as shown above. The GSTIN of the e-commerce operator must be provided operator wise and rate wise.Taxable Inter-State Supplies to Unregistered Persons (Invoice Value >Rs.2.5 Lakhs)

Interstate supplies to unregistered persons

In the above table, information about taxable inter-State supplies to un-registered persons where the invoice value is more than Rs 2.5 lakh must be provided. Hence, this table would contain only information of invoices wherein the value is more than Rs.2.5 lakhs and the customer is not registered under GST (i.e., B2C Transaction).

The information in this part must be divided into supplies normally made by the taxpayer and supplies made through an e-commerce operator. For both types, the following information must be provided:

Interstate supplies to unregistered persons

In the above table, information about taxable inter-State supplies to un-registered persons where the invoice value is more than Rs 2.5 lakh must be provided. Hence, this table would contain only information of invoices wherein the value is more than Rs.2.5 lakhs and the customer is not registered under GST (i.e., B2C Transaction).

The information in this part must be divided into supplies normally made by the taxpayer and supplies made through an e-commerce operator. For both types, the following information must be provided:

- Place of supply (State or Union Territory)

- Invoice number

- Invoice date

- Invoice value

- GST rate applicable

- Taxable value

- Amount of Integrated Tax

- Amount of GST Cess

Since inter-state supply does not attract CGST and SGST, the fields have been left out and only IGST tax applicable must be submitted.

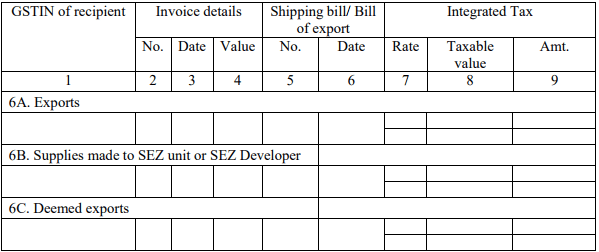

Zero Rated Supplies and Deemed Exports

GSTR-1 Zero rated supplies

In the above table, information about zero rated supplies and deemed exports must be provided along with GSTIN of the customer. Under GST, exports and supplies to SEZ units are treated as zero-rated supplies. For all zero-rated supplies and deemed exports, the following information must be provided in GSTR 1 filing.

GSTR-1 Zero rated supplies

In the above table, information about zero rated supplies and deemed exports must be provided along with GSTIN of the customer. Under GST, exports and supplies to SEZ units are treated as zero-rated supplies. For all zero-rated supplies and deemed exports, the following information must be provided in GSTR 1 filing.

- GSTIN of customer

- Invoice number

- Invoice date

- Invoice value

- Shipping bill or bill of export number

- Shipping bill or bill of export date

- Integrated tax rate

- Integrated tax applicable

- Taxable amount

The above information must be provided in GSTR 1 under the three categories of exports, supplies made to SEZ units and SEZ developers and deemed exports.

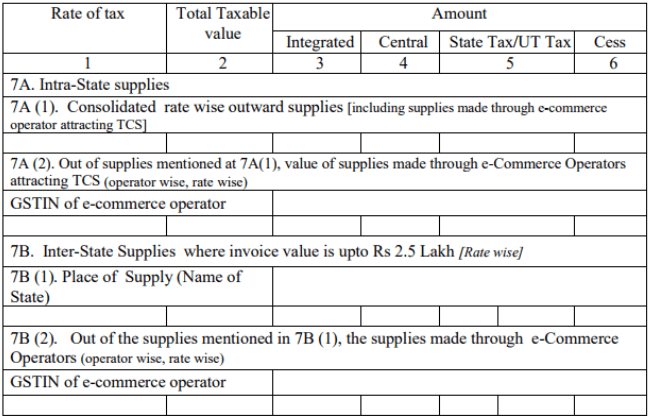

Taxable Supplies Made to Unregistered Persons

GSTR 1 Supplies to Unregistered Persons

In this table, consolidated information about all supplies made by the taxpayer to persons not having GST registration must be provided. For most businesses like restaurants, grocery stores, salons and other types of consumer-facing businesses, this table would be significant as majority or all sales would fall under the above category.

Also, this table contains only information wherein the tax invoice value is less than Rs.2.5 lakhs. If the value of the invoice was over Rs.2.5 lakhs, then it must be reported under taxable inter-State supplies to un-registered persons where the invoice value is more than Rs 2.5 lakh.

GSTR 1 Supplies to Unregistered Persons

In this table, consolidated information about all supplies made by the taxpayer to persons not having GST registration must be provided. For most businesses like restaurants, grocery stores, salons and other types of consumer-facing businesses, this table would be significant as majority or all sales would fall under the above category.

Also, this table contains only information wherein the tax invoice value is less than Rs.2.5 lakhs. If the value of the invoice was over Rs.2.5 lakhs, then it must be reported under taxable inter-State supplies to un-registered persons where the invoice value is more than Rs 2.5 lakh.

7.A Intra-State Supplies

Intra-state supplies are supplies made within the state. In the case of restaurants, grocery stores and other kind of shops, the supplies undertaken in the normal course of business would be intra-state supplies. For such sales within the state of the taxpayer, the following consolidated information must be provided rate-wise.

- Rate of tax

- Total Taxable value

- Amount of CGST applicable

- Amount of SGST applicable

- Amount of GST Cess applicable

For example, if an air-conditioned restaurant in Tamil Nadu sold 10 lakhs worth of food and beverages in a month to multiple customers, then the following information would. be submitted:

- Rate of tax = 18%

- Total Taxable value = Rs.10,00,000

- Amount of CGST applicable = Rs.90,000

- Amount of SGST applicable = Rs.90,000

- Amount of GST Cess applicable

On the other hand, for example, if a grocery store sold Rs.20 lakhs worth of grocery products in a month to multiple customers attracting multiple 1, then the following information would. be submitted:

- Rate of tax = 5%

- Total Taxable value = Rs.10,00,000

- Amount of CGST applicable = Rs.25,000

- Amount of SGST applicable = Rs.25,000

- Amount of GST Cess applicable - Rs.0

- Total Taxable value = Rs.10,00,000

Supplies through E-Commerce Operators

If any taxpayer supplies goods or services through an e-commerce operator, then the details must be provided for separately along with the GSTIN of the e-commerce operator, rate wise. In the grocery store example, if the supplies were made by the taxpayers to customers in Tamil Nadu through Amazon and Flipkart, then the following information should be provided.

- Supplies through Amazon (Amazon GSTIN)

- Rate of tax = 5%

- Total Taxable value = Rs.10,00,000

- Amount of CGST applicable = Rs.25,000

- Amount of SGST applicable = Rs.25,000

- Amount of GST Cess applicable - Rs.0

- Rate of tax = 12%

7.B Inter-State Supplies

Inter-state supplies apply to supplies made by a taxpayer outside of the state. Any taxpayer undertaking inter-state supplies is required to obtain

GST registration mandatorily, irrespective of aggregate annual turnover. In this section, the taxpayer must submit information about all supplies made out of state during the previous month. For example, if a tools manufacturer based in Tamil Nadu, made supplies to Karnataka and Maharashtra, then the following information should be provided.- Supplies to Karnataka

- Rate of tax = 5%

- Total Taxable value = Rs.10,00,000

- Amount of IGST applicable = Rs.50,000.

- Amount of GST Cess applicable - Rs.0

- Rate of tax = 12%

In addition to the above data provided state-wise under the place of supply, the taxpayer must also provide details of supplies made through an e-commerce operator based on e-commerce operator's GSTIN and GST rates.

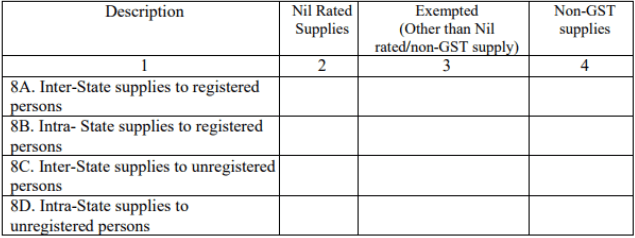

Nil, Exempt and Non-GST Supplies

GSTR 1 - Nil and Exempt Supplies

During the previous month, if the taxpayer supplied any goods or services at 0% GST rate or goods exempted from GST or any other non-GST supplies, then such information must be provided in the above section.

All nil rates supplies, exempted supplies and non-GST supplies must be categories and submitted under the following heads:

GSTR 1 - Nil and Exempt Supplies

During the previous month, if the taxpayer supplied any goods or services at 0% GST rate or goods exempted from GST or any other non-GST supplies, then such information must be provided in the above section.

All nil rates supplies, exempted supplies and non-GST supplies must be categories and submitted under the following heads:

- Inter-state supplies to registered persons

- Inter-state supplies to unregistred persons

- Intra-state supplies to registered persons

- Intra-state supplies to unregistered persons

This article is continued under

[crumina_text_highlight style="colored" size="default"]GSTR 1 Return Filing[/crumina_text_highlight]