IndiaFilings

Published on: Jun 24, 2026

Gst Return Due Date

Most businesses in India will need to GST returns each year to maintain GST compliance. In this article, we look at the list of returns to be filed by various types of businesses under GST along with GST return due date. Gst Return Due Dates are provided month-wise for all types of GST returns including GSTR-3B, GSTR 1, GSTR 5, and GSTR 6.

2018 September GSTR-3B Return Due Date Extended

The due date for filing September 2018 GSTR-3B return has been extended by the Government up to 25th October 2018. Originally, the due date for filing September GSTR 3B return was on 20th October. However, due to various issues, the Government has extended the due date today. The announcement was made through Twitter by the Hon'ble Minister of Finance Shri. Arun Jaitley as under: https://twitter.com/FinMinIndia/status/1053891571630907392

Official Communication on Extension

Ministry of Finance

Extension of due date to 25th October, 2018 for furnishing return in the FORM GSTR-3B for the month of September, 2018

Posted On: 21 OCT 2018 3:54PM by PIB Delhi It has been brought to notice that there have been apprehensions by trade and industry relating to the last date for availment of ITC for the period July, 2017 to March, 2018. In order to remove doubts, it was clarified that as per the law, the last date for availing ITC in relation to the period from July, 2017 to March, 2018 is the last date for the filing of return in the FORM GSTR-3B for the month of September, 2018. In view of the said apprehensions and with a view to give some more time to the trade and industry, the last date for furnishing return in the FORM GSTR-3B for the month of September, 2018 is being extended up to 25th October, 2018. Relevant notification will follow shortly. The extension of the said due date also implies that the last date for availment of ITC for the period July, 2017 to March, 2018 also gets extended up to 25th October, 2018. It may also be noted that the Government has extended the last date for furnishing of return in FORM GSTR-3B for the month of September, 2018 for certain taxpayers who have been recently migrated from erstwhile tax regime to GST regime vide notification No. 47/2018- Central Tax dated 10th September, 2018. For such taxpayers, the extended date i.e. 31st December, 2018 or the date of filing of annual return whichever is earlier will be the last date for availing ITC in relation to the said invoices issued by the corresponding suppliers during the period from July, 2017 to March, 2018. ********* DSM/RM

Due Date for Filing ITC Claim Extended

As provided in the Tweet above, the due date for filing ITC cliam has also been extended from 20th October to 25th October 2018.

Revised Due Dates For GST Return Filing

The Central Board of Indirect Taxes and Customs, vide notification no. 32/2018 – Central Tax dated 10th August, 2018, has clarified that the Commissioner, after the recommendation of the GST Council, has notified revised due dates for the registered person whose aggregate turnover is more than INR 1.5 Crore and are required to file return in form GSTR – 1 on monthly basis. The revised due dates for filing return in form GSTR – 1 for the period July, 2018 to March, 2019 would be 11th day of the month succeeding such month. Month-wise applicable due date as per the said notification for return in form GSTR – 1 is tabulated hereunder for ready reference –

| Period | Revised Due Dates For Filing Return In Form GSTR – 1 (Monthly) |

| July, 2018 | 11th August, 2018 |

| August, 2018 | 11th September, 2018 |

| September, 2018 | 11th October, 2018 |

| October, 2018 | 11th November, 2018 |

| November, 2018 | 11th December, 2018 |

| December, 2018 | 11th January, 2019 |

| January, 2019 | 11th February, 2019 |

| February, 2019 | 11th March, 2019 |

| March, 2019 | 11th April, 2019 |

Revised Due Dates For Return In Form GSTR – 1 (Quarterly Basis)

The Central Board of Indirect Taxes and Customs, vide notification no. 33/2018 – Central Tax dated 10th August, 2018, has clarified that the Central Government, on recommendation of the Council, has notified revised due dates for the registered person having aggregate turnover up to INR 1.5 Crore and are filing return in form GSTR – 1 on quarterly basis. The said revised due dates are tabulated hereunder –

| Period | Due Date For Filing Quarterly Return In Form GSTR – 1 |

| July – September, 2018 | 31st October, 2018 |

| October – December, 2018 | 31st January, 2019 |

| January – March, 2019 | 30th April, 2019 |

Revised Due Dates For Return In Form GSTR – 3B

The Central Board of Indirect Taxes and Customs, vide notification no. 34/2018 – Central Tax dated 10th August, 2018, has clarified that the Commissioner, after recommendation of the council, has specified that return in form GSTR – 3B for the period July, 2018 to March, 2019 should be furnished on or before the 20th day of the month succeeding such month. The return in form GSTR – 3B is to be furnished electronically through the common portal. Month-wise applicable due date as per the said notification for return in form GSTR – 3B is tabulated hereunder for ready reference –

| Month | Respective Due Date |

| July, 2018 | 20th August, 2018 |

| August, 2018 | 20th September, 2018 |

| September, 2018 | 20th October, 2018 |

| October, 2018 | 20th November, 2018 |

| November, 2018 | 20th December, 2018 |

| December, 2018 | 20th January, 2019 |

| January, 2019 | 20th February, 2019 |

| February, 2019 | 20th March, 2019 |

| March, 2019 | 20th April, 2019 |

It is further clarified, vide notification no. 34/2018 – Central Tax dated 10th August, 2018, that registered person who are required to file the return in form GSTR – 3B can discharge his tax, interest, penalty, fees or any other amount as payable by either debiting the electronic cash or the electronic credit ledger on or before the last day on which the assessee is required to furnished return in form GSTR – 3B. For example Mr. X is required to file return in form GSTR – 3B for the month of August, 2018, then, he can discharge his liability towards tax, interest, penalty, fees or any other amount by 20th September, 2018 i.e. the last date of filing return in form GSTR – 3B for the month of August, 2018.

GST Return Due in May 2018

In May, 2018 the following GSTR 3B return for the month of April 2018 will become due for taxpayers:

GSTR-3B Due Date Extended

The GSTR3B due date for April, 2018 has been extended upto 22 May, 2018. Normally, the GST3B returns are due on the 20th of each month. Hence, the GSTR3B return for the month of April would normally be 20th May 2018. However, due to a glitch in the GST Portal, the GSTR3B return due date for the month of April, 2018 has been extended upto 22nd May, 2018. The announcement for the due date extension was made through the official GST Twitter handle as follows: https://twitter.com/askGST_GoI/status/997434753962987520

Upcoming Gst Return Due Dates in May, 2018

GSTR-3B, GSTR-5, GSTR-6 and GSTR-5A should be filed in May, 2018. Regular taxpayers having GST registration would have to file GSTR-3B return only. GSTR-5 is only applicable for non-resident taxable persons and GSTR-6 is applicable only for Input Service Distributors.

- GSTR-3B (April 2018) - May 22nd, 2018

- GSTR-5 (April 2018) - May 20th, 2018

- GSTR-6 (Jul'17 - Apr'18) - May 31st, 2018

- GSTR-5A (April 2018) - May 20th, 2018

- GST TRAN-2 - Jun 30th, 2018

- RFD-10 - The individual shall claim the refund at the end of eighteen months (after end of the quarter)

Quarterly return for registered persons with aggregate turnover up to Rs. 1.50 Crores

- GSTR-1 (Jan-Mar, 2018) - Apr 30th, 2018

Turnover exceeding Rs. 1.5 Crores or opted to file monthly Return

- GSTR-1 (Mar 2018) - May 10th, 2018

- GSTR-1 (Feb 2018) - Apr 10th, 2018

GST Returns Due in April 2018

In April, 2018 the following GST returns will become due for taxpayers:

- April 10th 2018 - GSTR 1 return must be filed by taxpayers having GST registration with an annual turnover of more than Rs.1.5 crores.

- April 18th 2018 - GSTR 4 return must be filed by taxpayers registered under the GST Composition Scheme.

- On April 20th 2018 - GSTR-3B return must be filed by all taxpayers who have a GST registration irrespective of turnover.

- April 20th 2018 - GSTR-5 return must be filed by all taxpayers who have a non-resident taxable person GST registration irrespective of turnover.

- On April 20th 2018 - GSTR-5A return must be filed by all taxpayers who have a non-resident taxable person GST registration irrespective of turnover.

- April 30th 2018 - GSTR 1 return for the quarters of January to March 2018 must be filed by taxpayers having GST registration with a turnover of less than Rs.1.5 crores.

How to File GST Returns?

GST Returns can be filed online through the GST Common Portal or an

online GST accounting software. The proposed GST regime is backed by a technology platform maintained by the GSTN. GSTN has provided GSP Licenses for enabling businesses to file GST returns through various types of accounting software and ERP systems. Hence, GST return can be filed directly on the GST Common Portal or through a GST accounting software with the requisite features.

When to File GST Returns?

Under GST, a regular taxpayer needs to furnish three monthly returns and one annual return. However, the following taxpayers shall file other forms if:

- Registered under the composition scheme,

- Non-resident taxpayer

- Taxpayer registered as an Input Service Distributor

- Person liable to collect TDS or TCS or

- Granted UIN.

What is the penalty for late filing of GST Returns?

Any taxable person under GST who fails to file form GSTR 3B, GSTR-1, GSTR-2, GSTR-3 or Final Return within the due dates, will be fined a late fee of Rs. 50 per day. In case of NIL return, the penalty will be Rs.20 per day.

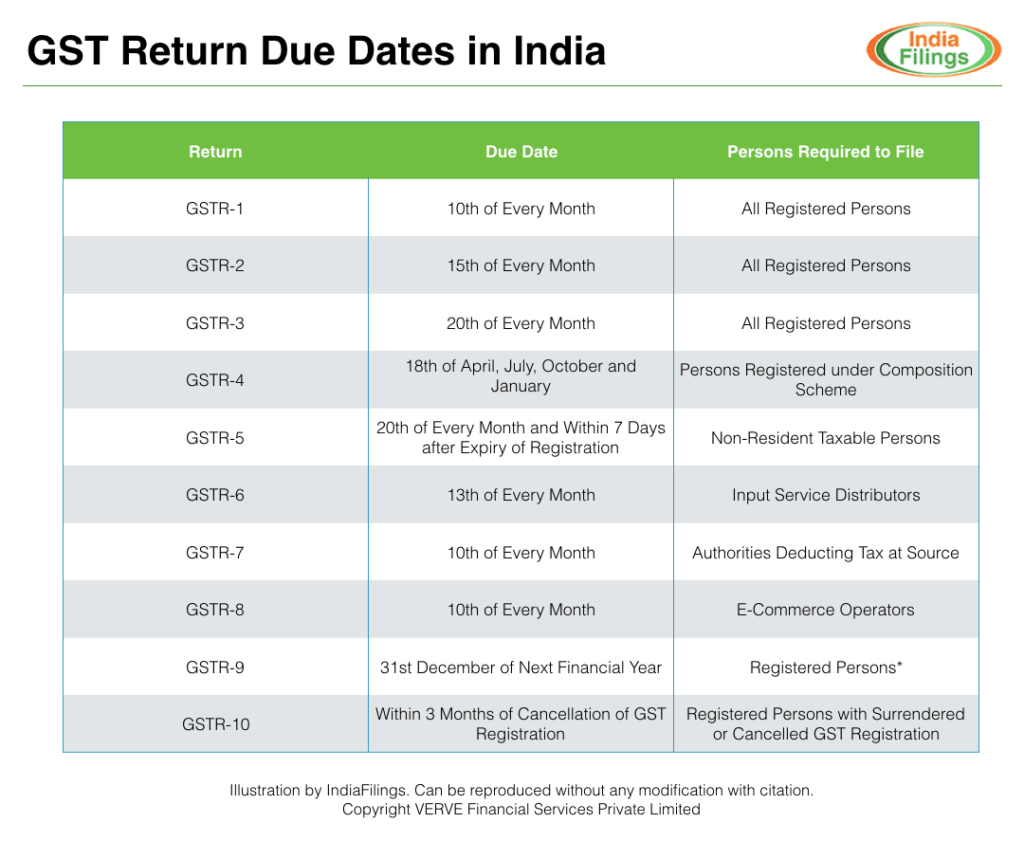

Gst Return Due Date for Regular Taxpayers

Most taxable persons registered under GST would be termed as regular taxpayers. Regular taxpayers must file 3 returns each month as follows:

GSTR 3B Return

GSTR-3B return must be filed by all persons having GST registration. GSTR-3B return is due on the 20th of each month.

GSTR-1 - Statement of Outward Supplies

GSTR-1 Returnor the statement of outward supplies is used to file details of all supplies made by a taxpayer in the previous month and record the tax liability of the supplier. The taxpayer shall file GSTR-1 on or before the 10th of every month with details of all supplies effected during the previous month.

GSTR-2 -Statement of Inward Supplies

GSTR-2or the statement of inward supplies is used to file and verify details of input tax credit accrual received during the previous month. The portal auto-populates the GSTR-2 details as per the information filed in GSTR-1. Hence, in the statement of inward supplies, the taxpayer must only provide minimal additional information like imports, and purchases from unregistered suppliers. The taxpayer shall file GSTR-2 on or before the 15th of every month with details of all supplies received during the previous month.

Note: The Ministry shall update the details regarding GSTR 2 and put on hold.GSTR-3 - Consolidated Return

All the taxpayers shall file the consolidated returns in Form GSTR-3 by 20th of every month. GSTR-3 consolidates the following information already provided by the taxpayer to arrive at final tax payable:

- Outward Supplies (Auto-Populated from GSTR-1)

- Inward Supplies (Auto-Populated from GSTR-2)

- Input Tax Credit availed

- Tax Payable

- Tax Paid (Using both Cash and ITC)

GSTR-9 - GST Annual Return

GSTR-9 or Annual GST returnmust be filed by 31st December of the next financial year by all taxable persons registered under GST. Information provided in GSTR-4 would include details of expenditure and details of income for the entire financial year. The taxpayer should provide the audited the GST Annual Return by a practising Chartered Accountant if the aggregate turnover of the registered person exceeded Rs. 2 crores during a financial year. Further, along with the GST annual return, a copy of audited annual accounts and a reconciliation statement, duly certified by a Chartered Accountant, in FORM GSTR-9C. The taxpayer shall file FORM GSTR-9C electronically through GST Common Portal.

Gst Return Due Date for Composition Scheme Taxpayers

The

GST Composition Schemeis designed to reduce the tax compliance burden for small businesses having an annual turnover of less than Rs.150 lakhs and doing sales only within the state. Taxable persons registered under the GST Composition Schemes should mandatorily file quarterly GST returns and GST annual return.

GSTR-4 - GST Return for Composition Scheme Suppliers

The taxpayer shall file GSTR-4 every quarter on the 18th of the month, succeeding the quarter. Hence, GSTR-4 would be due on the 18th of July, 18th of October, 18th of January and 18th of April.

GSTR-4 - GST Annual Return for Composition Suppliers

A composition supplier shall also file GST annual return on or before the 31st December of the next financial year. Annual return filed by a Composition Scheme supplier would not have to be audited, as the turnover would not be over Rs.75 lakhs.

GST Return Filing Due Dates

Gst Return Due Date for Foreign Companies

Foreign companies or non-resident taxable under GST are also required to

obtain GST registrationand

file GST returnsif they supply goods or services to persons located in India. All foreign companies or non-resident taxable persons should file GSTR-5 on the 20th of every month and within 7 days of the expiry of GST registration.

GSTR-5 - GST Return for Non-Resident Taxable Persons

Non-resident taxable persons shall file GSTR-5 with details of all outward supplies and inward supplies through the GST Common Portal. Based on the filing, the taxpayer should pay the tax, interest, penalty, fees or any other amount payable under the GST Act before 20th of every month or with 7 days of the expiry of GST registration.

GSTR-5A - GST Return for Non-Resident Taxable Persons providing OIDAR Services

A non-resident taxable person shall file Form GSTR-5A instead of GSTR-5 if involved in providing online information and database access or retrieval (OIDAR) services from a place outside India to a person in India. The concerned person shall file before the 20th of every month. A non-resident taxable person under GST is not required file GSTR-9 which is the GST annual return.

Gst Return Due Date for E-Commerce Operators

E-commerce operators are a taxable person under GST who own, operate or manage a digital or electronic facility or platform for electronic commerce. Electronic commerce operators shall collect the tax at source and file FORM GSTR-8 before the 10th of the next month. Hence, even if an electronic commerce operator is acting only as a marketplace, they must provide details of all supplies effected through them and the amount of tax collected. After the due date of FORM GSTR-8, the system provides the required details as provided by electronic commerce operators in an electronic mode in the GST Common Portal. The user can use those details when filing Form GSTR-2 o As per GST rules the electronic commerce operator shall file the GST returns every month such as GSTR-1, GSTR-2, GSTR-3, if involved in the supply of any taxable goods or services to the consumers.

Gst Return Due Date for Input Service Distributors

All person classified as an Input Service Distributor under GST is required to file FORM GSTR-6 on or before the 13th of each month. Details of tax invoices on which credit has been received would be made available to Input Service Distributors on FORM GSTR-6A and the input service distributor can if required, after adding, correcting or deleting the details, file the GST return electronically.

Gst Return Due Date for Authorities Deducting Tax at Source

Any authority deducting tax at source should file Form GSTR-7, on or before 10th of every month. The GST portal shall provide the details electronically to the supplier related to the tax deducted at source by the relevant authorities. The details shall reflect as mentioned in GSTR-7. The supplier can receive the details in FORM GSTR-2A and FORM-GSTR-4A.

Due Date for Filing GST Final Return

All taxable persons registered under GST shall file their final return irrespective of the registration stands surrendered or cancelled. GST Final Return or GSTR-10 must be filed within three months of the date of cancellation or date of the order of cancellation, whichever is later.