Renu Suresh

Expert

Published on: Apr 20, 2026

Opting-in for Composition Scheme for the Financial Year 2021-2022

The Goods and Service Tax Network (GSTN) has issued a notification for taxpayers opting into the

GST composition scheme for the financial year 2021-2022. The notification dated 24th March 2021 directs all the regular taxpayers eligible for the composition scheme to file form CMP-02 by 31st March 2021 for opting into the scheme for the financial year 2021-22. In the present article, we would look into the aspects of opting in the composition scheme.Synopsis of GSTN Notification

All the businesses that have already opted in to the past composition scheme and intend to continue for FY 2021-2022 need not file the declaration by3 1st March 2021.

- New Taxpayers who intend to join the scheme must file form CMP-02 by 31st March 2021.

- Newly eligible taxpayers can opt into the composition scheme after logging into the GST portal by filling the form CMP-02.

- The composition scheme will be available for taxpayers with effect from 1st April 2021 upon the filing of the form CMP-02

GST Composition Scheme

The composition scheme under

GST is an optional and alternative method specially designed for the small taxpayers whose turnover is up to 1.5 Crore. The primary objective of the scheme is to reduce the compliance cost (fewer returns, maintaining books of account, and no-issuance of tax invoices), tedious formalities under the law, and limited tax liability. The eligible taxpayer opting for this scheme shall be required to pay tax quarterly at a defined percentage of his turnover.Eligibility for opting-in for Composition Scheme

The notification also informs the taxpayers about the eligibility to join the Composition Scheme. Any regular taxpayer not wishing to claim input tax credit may benefit from the scheme if the turnover criterion is met.

- A dealer or manufacturer of goods must have aggregate turnover ( at PAN-level) of up to Rs.1.5 crore in the previous financial year.

- This limit is relaxed in a few states such as Tripura, Manipur, Meghalaya, Mizoram, Nagaland, Arunachal Pradesh, Sikkim, and Uttarakhand.

- If the taxpayer is supplying services or is into mixed supplies, the aggregate turnover of the previous financial year has to be equal to or below Rs.50 lakhs for him to be eligible under the scheme

Businesses Not eligible for opting in Composition Scheme

There are a few exceptions where businesses will not be eligible for the composition scheme

- Suppliers of the goods or services who are not liable to pay tax under GST will not be eligible for the scheme

- Inter-State outward suppliers of goods/service also not eligible for the scheme

- Taxpayers supplying goods through e-commerce operators who are required to collect tax under section 52 of the GST act

- The composition scheme will not be applicable for The manufacturers of notified goods like Ice cream and other edible ice, whether or not containing cocoa, tobacco and manufactured tobacco substitutes, Pan Masala, and Aerated water

Prescribed Date to Opt for the Composition Scheme

To avail of this scheme, the taxpayer needs to file an online application to Opt for Composition scheme with the tax authorities. Taxpayers who can opt for this scheme can be categorized as below:

- New Taxpayers: Any person who becomes liable to register under GST Act, after the appointed day, needs to file his option to pay the composition amount in the Application for New Registration in Form GST REG-01.

- Existing Taxpayers: Any taxpayer who is registered as a normal taxpayer under GST needs to apply to opt for Composition Levy in Form GST-CMP-02 at GST Portal before the commencement of financial year for which the option to pay tax under the aforesaid section is exercised.

With this notification, GSTN informed that all the businesses that have already opted in to the past composition scheme and intend to continue for Financial Year 2021-2022 need not file the declaration by 31st March 2021. New Taxpayers who intend to join the scheme must file form CMP-02 by 31st March 2021.

Online Procedure For Composition Scheme

As mentioned above, any taxpayer who is registered as a normal taxpayer under GST needs to apply to opt for Composition Levy in Form GST-CMP-02 at GST Portal before the commencement of the financial year. The procedure to opt for a composition scheme for the financial year 2021-2022 is as follows:

- To opt for the composition scheme, the taxpayer needs to access the official website of GST. The GST Home page will be displayed.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Home Page

Log in to the GST Portal by entering the login Credentials.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Home Page

Log in to the GST Portal by entering the login Credentials.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Login Page

Opting-in for Composition Scheme for the Financial year 2021-2022 - Login Page

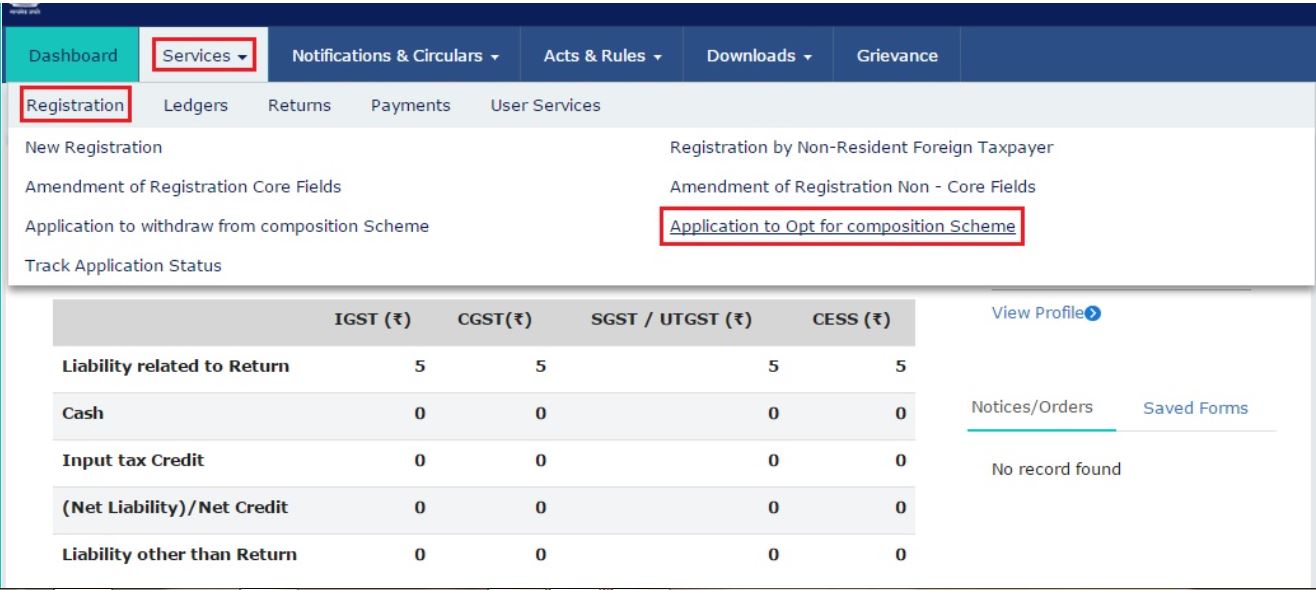

- After login to the portal, select ‘Application to Opt for Composition Levy’ from the Registration Menu.

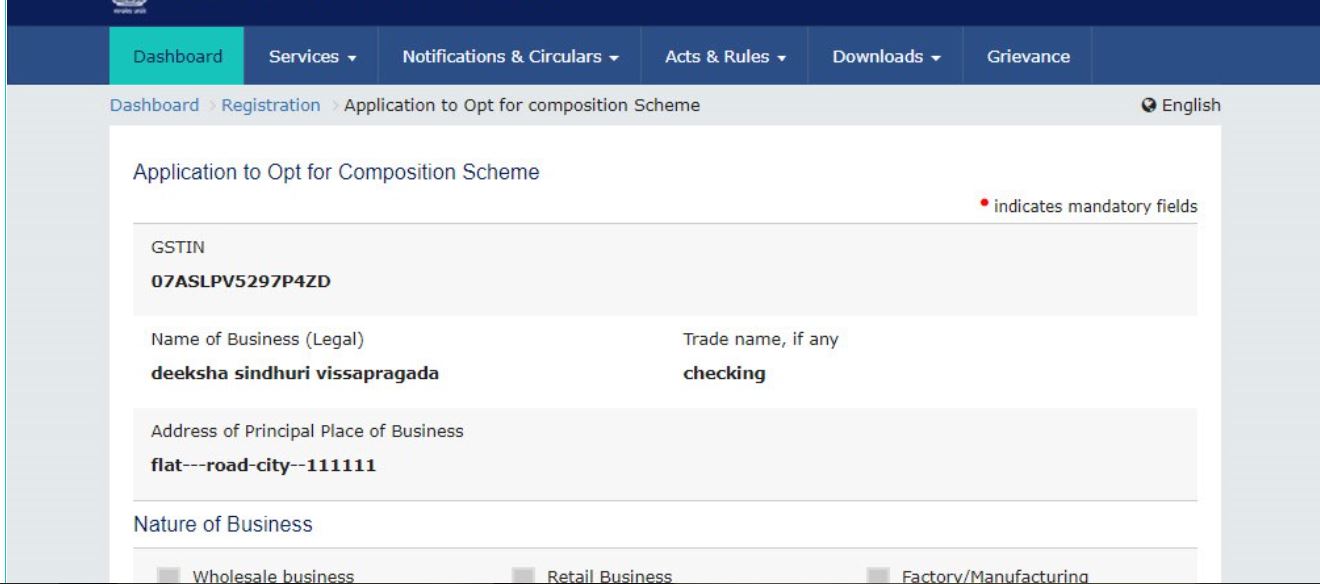

- The link will be redirected to a new screen – Application to Opt for Composition Levy. The GSTIN, Legal Name of Business, Trade Name, and Address of Principal Place of Business will be displayed.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application1

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application1

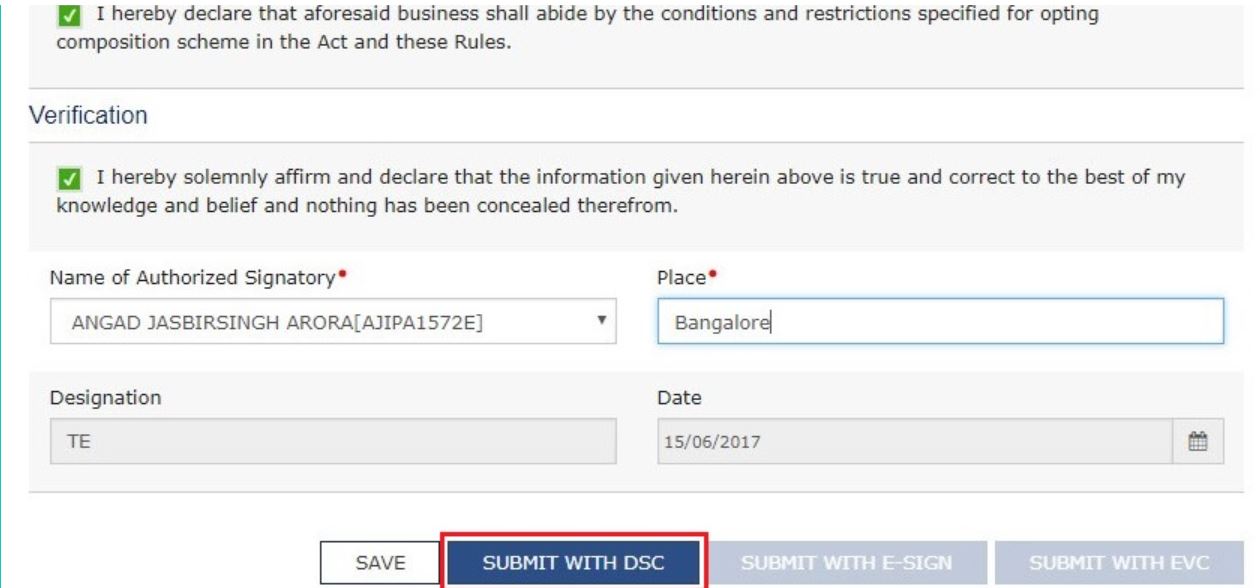

- There is a Composition Declaration that must check to pledge to abide by the conditions and restrictions for Taxpayers who are under the Composition Scheme

- Before submission, the taxpayer must check the box for Verification (below the Composition Declaration) that states that all the information given is true and that nothing has been concealed from the authority.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application2

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application2

- After selecting the Authorized Signatory and enter the Place, the options to submit the form will get activated. Select the desired mode – DSC, E-sign, or EVC – and click the corresponding submission option.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application4

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application4

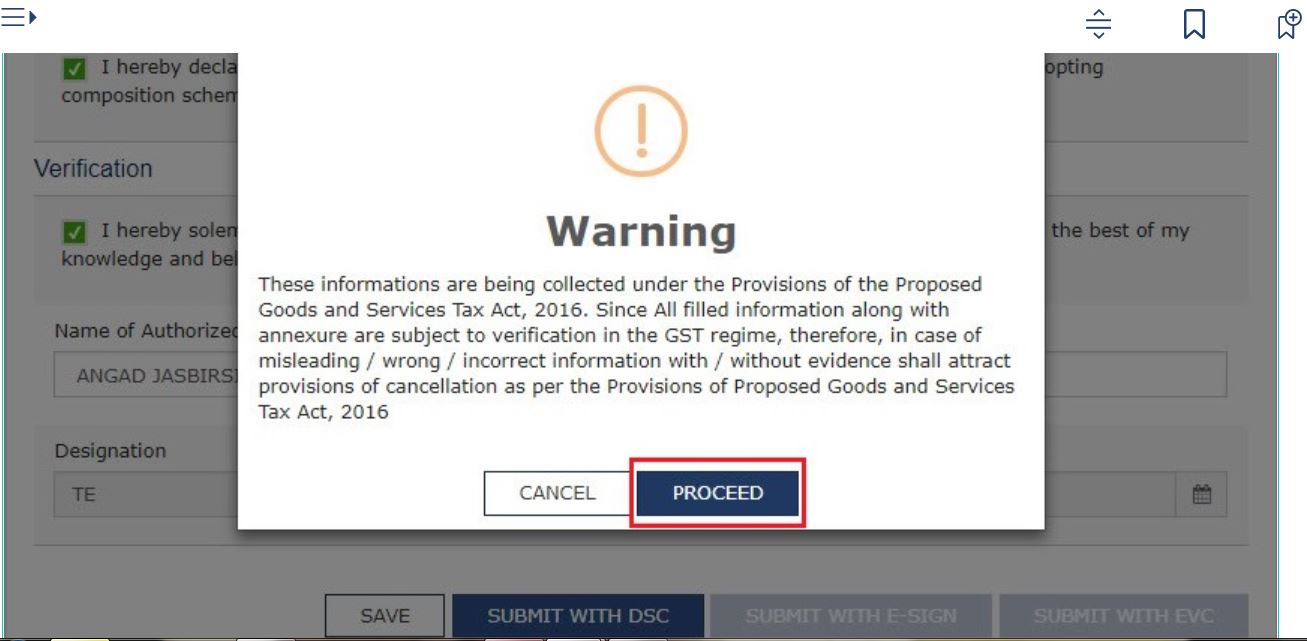

- The taxpayer will get a prompt to confirm your action, click on PROCEED to move forward.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application5

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application5

- The system will retrieve the installed digital signatures available on the system using the e-Signer and the taxpayer will get a pop-up to select the desired DSC. Select the desired signature.

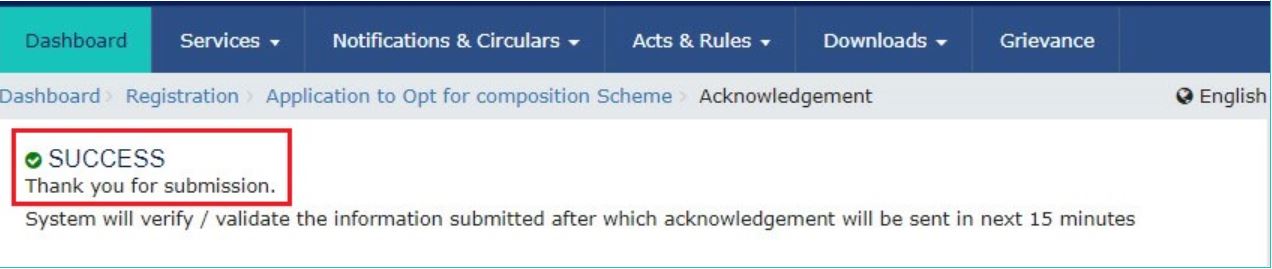

- After selecting the desired digital signature (it will get highlighted in blue) and click the Sign option. If the digital signature is authenticated, the taxpayer will get a SUCCESS message.

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application6

Opting-in for Composition Scheme for the Financial year 2021-2022 - Application6

- The system will perform some validations and if they are successful the ARN for the work item will be generated and sent to the taxpayer via e-mail and SMS within the next 15 minutes.

Filing of Stock Intimation is Mandatory

In addition to applying to opt for Composition scheme, the taxpayer also requires to file a Stock Intimation to provide the details of stock including inward supply of goods from unregistered persons, held by the taxpayer on the day preceding the date from which you opt to pay the composition amount. The taxpayer needs to file Stock Intimation details within 30 days of the date from which Composition Levy is sought. Defined Tax Rate under Composition Scheme The eligible taxpayer opts the scheme shall be required to pay tax quarterly at a defined percentage of his turnover:

| S.No. | Eligible Taxpayers | Rate of Tax |

| 1 | Manufacturers, other than manufacturers of such goods as may be notified by the Government (Ice cream, Pan Masala, Tobacco products etc.) | 1% (0.5% CGST + 0.5% SGST) of the turnover |

| 2 | Restaurant Services (only this service is covered under this scheme) | 5% (2.5% CGST + 2.5% SGST) of the turnover |

| 3 | Traders or any other supplier eligible for composition levy | 1% (0.5% CGST + 0.5% SGST) of the turnover |

| 4 | Goods & Services (As composite supply) | 1% (0.5% CGST + 0.5% SGST) of the turnover |

| 5 | Goods or Services (As mixed supplies) | 6% (3% CGST + 3% SGST) of the turnover |