IndiaFilings

Expert

Published on: Apr 22, 2026

GST Registration for Non-Resident Taxable Person

Non-resident taxable person (NRI) under GST is any person or business or not-for-profit who occasionally undertakes transactions involving the supply of goods or services or both, whether as principal or agent or in any other capacity, but who has no fixed place of business or residence in India. Hence, any foreign person or foreign business or organisation supplying goods or services to India would be a non-resident taxable person - requiring compliance with all GST regulations in India.

GST Registration for Non-Resident Taxable Person

All non-resident taxable persons are required to

obtain GST registration in India, irrespective of aggregate annual turnover or any other criteria. Further, the GST Act and Rules specify that all non-resident taxable persons must obtain GST registration 5 days prior to the commencement of business. Hence, it is important for foreign businesses supplying goods and services to India to obtain GST Registration at the earliest.Procedure for Applying for GST Registration - Non-Resident Taxable Persons

Prior to beginning the process for applying for GST registration, foreign businesses or foreign applicants must identify a person in India to act as its authorised representative for GST compliance and obtain a PAN in India for the foreign entity (optional). As per the GST rules, a non-resident taxable person should acquire attestation in the GST registration application. The rules state that the applicant shall acquire attestation from an authorized signatory and resident of India with a valid PAN. Hence, once the authorised signatory is engaged, the Indian GST registration process can be started for non-resident taxable persons (NRIs). To apply for GST registration as a non-resident taxable person, an application must be submitted in FORM GST REG-09. GST registration is PAN-based for regular taxpayers. However, in the case of non-resident taxable persons, the GST registration application can be submitted with a tax identification number or unique number on the basis of which the entity is identified by the Government of that country or its PAN, if available.

GST Registration Procedure - OIDAR Service Providers

In case of a non-resident taxable person supplying online information and database access or retrieval (OIDAR) services to a non-taxable online recipient, then application in FORM GST REG-10 must be submitted electronically. Note: IndiaFilings can help foreign businesses

obtain GST registration in India.Documents Required for GST Registration

The following documents must be provided by the non-resident taxable person during the GST registration process:

Proof of Principal Place of Business

- For own premises – Any document in support of the ownership of the premises, like the Latest Property Tax Receipt or Municipal Khata copy or copy of the Electricity Bill.

- Rented or Leased premises – A copy of the valid Rent / Lease Agreement with any document in support of the ownership of the premises of the Lessor, like the latest Property Tax Receipt or Municipal Khata copy or copy of the Electricity Bill.

- For premises not covered above – A copy of the Consent Letter with any document in support of the ownership of the premises of the Consenter like a Municipal Khata copy or Electricity Bill copy. For shared properties also, the same documents may be uploaded.

Identity Proof

- A scanned copy of the passport of the non-resident taxable person with VISA details. In the case of a business entity incorporated or established outside India, the application for registration shall be submitted along with its tax identification number or unique number on the basis of which the entity is identified by the Government of that country, or its PAN, if available.

- In case of Company/Society/LLP/FCNR/ etc. person who is holding power of attorney with an authorization letter.

- A scanned copy of the Certificate of Incorporation if the Company is registered outside India or in India.

- A copy of the license is issued by a foreign country, if available.

- Scanned copy of the Clearance certificate issued by the Government of India, if available.

Bank Account Proof

- A scanned copy of the first page of the Bank passbook / one page of the Bank Statement Opening page of the Bank Passbook held in the name of the Business – containing the Account Number, Name of the Account Holder, MICR and IFSC and Branch details.

Authorisation for Authorised Representative in India

Non-resident taxable persons are required to appoint an authorised representative in India. An authorization or copy of the Resolution of the Managing Committee or Board of Directors authorising the authorised representative must be provided in the following format:

Declaration of Authorised Signatory

Know more about the documents required for GST registration.

Declaration of Authorised Signatory

Know more about the documents required for GST registration.

GST Deposit for Non-Resident Taxable Persons (NRI)

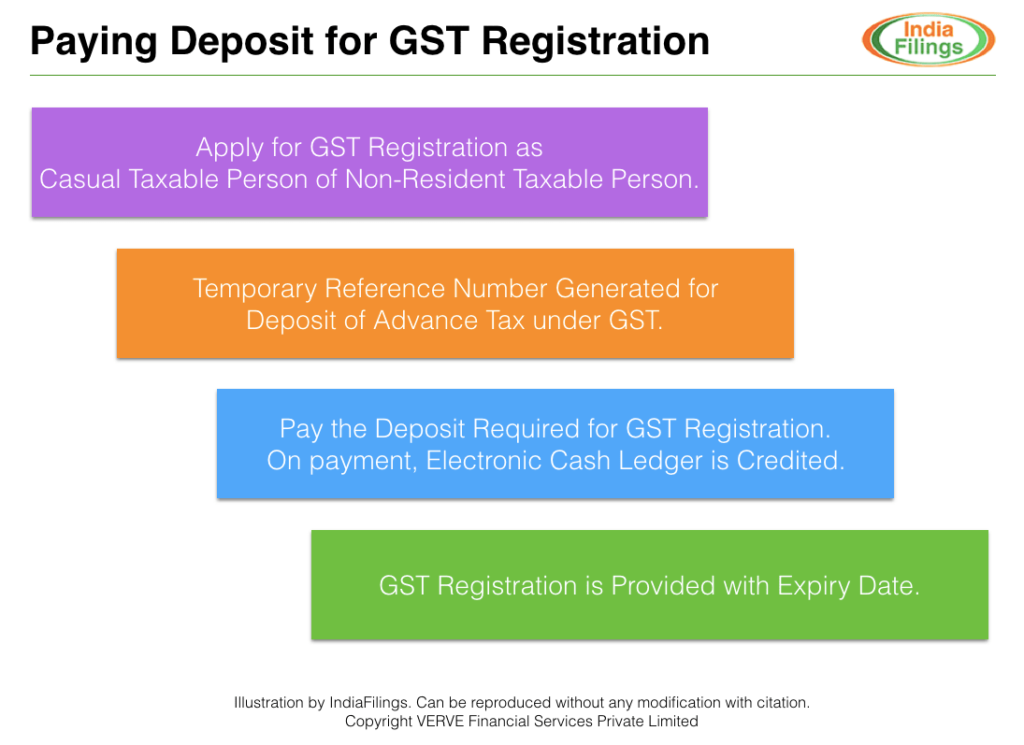

Non-resident taxable persons and casual taxable persons under GST are required to remit a deposit for GST registration. The amount of deposit for GST registration would equal the expected tax liability during the validity of the registration. Further, in case a non-resident taxable person requests for extension of GST registration, then tax must be deposited in advance based on the expected tax liability of the extension period. Once the non-resident taxable person files the application for GST registration, the portal generates a reference number for the application on the payment of advance tax. On payment of tax, the system credits to the electronic cash ledger of the taxpayer and then provides the GST registration certificate. The illustration below shows the process of obtaining GST registration for non-resident taxable persons.

Paying Deposit for GST Registration

Paying Deposit for GST Registration

Validity of GST Registration for Non-Resident Taxable Persons (NRI)

GST registration for casual taxable persons and non-resident taxable persons is provided with a validity period. The validity period would be based on the request of the taxable person and the amount of the GST deposit remitted. If a non-resident taxable person intends to extend the validity period of GST registration, the individual shall make an application in FORM GST REG-11 before the end of the validity of the registration.

Important Instructions for Non-Resident Taxpayers (NRI)

- The name of the Applicant should reflect the passport.

- It is mandatory for the applicant to apply for GST registration on the common portal by filing form GST REG-09 at least 5 days before commencement of the business.

- The applicant should submit the Tax identification number or unique identification number (as identified by the respective Government) or PAN (if applicable) along with the application in case of a business entity incorporated or established outside India.

- The applicant shall provide the application duly signed or verified by EVC

In the case of NRI, in order to obtain GST registration, a two-step procedure needs to be followed:

- Provisional registration

- Final registration

Provisional Registration

The Non-resident taxable person (NRI) shall submit an application in Form GST REG-09 through online. The applicant shall also submit a self-attached copy of a valid passport along with the application. The applicant shall submit the application 5 days prior to the commencement of business. In the case of foreign entity, the concerned individual shall submit the application for GST registration along with tax identification number or unique number or PAN (if applicable). Such advance payment of tax would be based on self-estimation. Hence, the applicant should mandatorily make the advance tax deposit along with the application.

Final Registration

The final registration of a Non-resident taxable person (NRI) would be carried out in the same line as that of the resident taxpayer in India. The following details the procedure:

- The applicant shall submit the FORM GST REG-26 electronically. In addition, the concerned applicant shall submit all the information related to tax and GST within a period of 3 months from the provisional registration.

- The applicant shall receive the GST certificate in FORM GST REG-06 upon providing accurate and complete details. Upon any discrepancies or incomplete information, the authorized may cancel the application for registration through FORM GST REG-28.

- However, if the applicant provides an appropriate reply to the show cause notice issued and the officer accepts the said reply, the officer shall cancel the show cause notice by issuing an order in FORM GST REG-20.

- The authorized signatory of the applicant should duly sign the application for registration. The said authorized signatory should be a person resident in India and he would have a valid PAN.