IndiaFilings

Expert

Published on: Jun 24, 2026

GST Input Tax Credit Scheme-For Existing Stock

The Ministry of Finance (MoF) announced the GST input tax credit (ITC) scheme in the Transitional Provisions rules to provide GST Input Tax Credit for unregistered persons. The scheme shall account the unaccounted goods or stock on hand during the GST rollout. In this article, let us look at the

GST Input Tax Credit Scheme for unregistered taxpayers and existing stock in detail.GST Input Tax Credit-For Central Excise

The GST input tax credit scheme for Central Excise mentioned in the Transitional Provisions rules targets unregistered persons who do not have any existing registration like central excise registration or evidence for payment of central excise duty while having stock on the GST implementation date. The Ministry allows claiming GST ITC for such persons on goods held in stock. Further, central excise or additional duties of customs shall apply on the date of GST implementation after payment of central tax. The framework of the GST input tax credit allows a 60% tax rate on goods which attract central tax at the rate of 9% or more. For all other goods, the central excise tax rate shall apply at 9% or less and GST input tax credit allows at 40%. Upon paying integrated tax on such goods, the amount of input tax credit shall apply at the rate of 30% and 20%, respectively. The system credits the GST input tax to the electronic credit ledger of the taxpayer after central tax payable on such supply.

Conditions to Avail ITC

The person shall follow the conditions below to avail the ITC under this scheme:

- Goods unconditionally exempted from the whole of the duty of excise specified in the First Schedule to the Central Excise Tariff Act, 1985. Further, the rate of the goods applies nil rated in the said Schedule.

- The registered person shall procure the documents for the said goods and make available in the records.

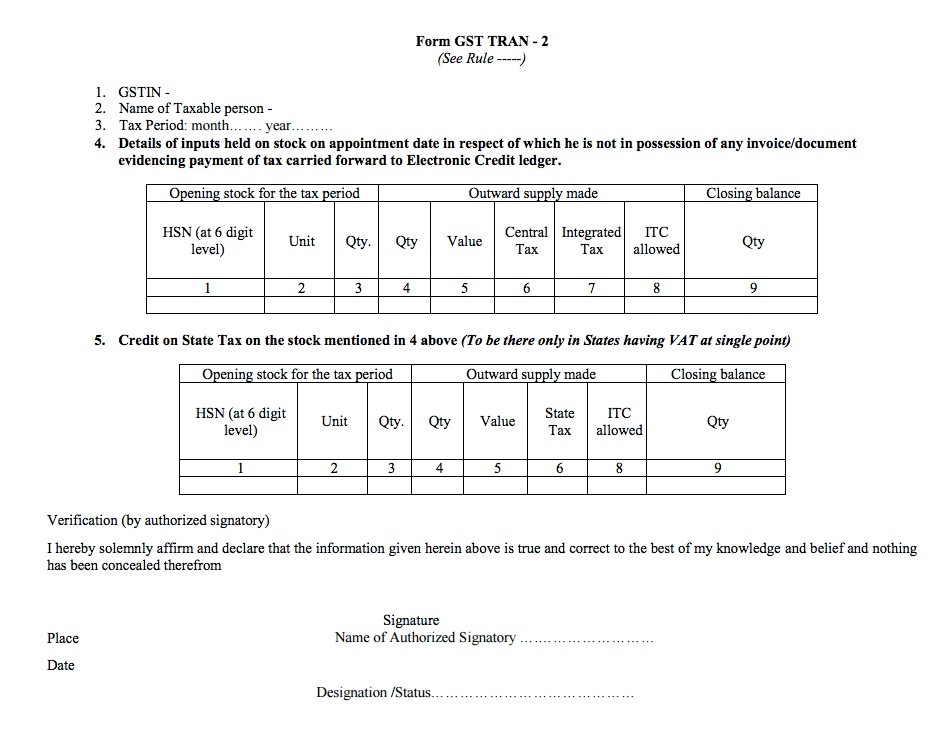

- The registered person availing this scheme and furnished the details of stock held by the taxpayers shall submit a statement in FORM GST TRAN 2. At the end of each of the six tax periods, the taxpayer shall detail the stock indicating the applicability of the scheme for such supply of goods effected during the tax period.

- The system shall credit the amount of credit to the electronic credit ledger of the applicant as maintained in FORM GST PMT-2 on the Common Portal.

- The concerned individual shall store the details of the stock of goods to identify easily by the registered person.

The scheme for claiming GST input tax credit against central excise would be available for 6 months from the date of GST implementation.

GST Input Tax Credit-For VAT

Any taxpayer having VAT registration and holding stock of goods on the GST implementation date for which VAT payment has been at the first point of sale in the State and the subsequent sales of which are not subject to tax in the State availing credit - would be allowed to avail GST input tax credit even if there is no document evidencing payment of value-added tax. The Act allows the GST input tax credit for such goods at the rate of 60% for goods which attract state tax at the rate of 9% or more. For goods having state tax at the rate of 9% or less, the input tax credit shall apply at the rate of 40% would be provided. If integrated tax is paid on such goods, the amount of credit shall be allowed at the rate of 30% and 20%. respectively. GST input tax credit would be credited to the electronic credit ledger of the taxpayer after the State tax payable on such supply has been paid.

Conditions to Avail GST ITC

The concerned individual shall meet the following criteria to claim the GST input tax credit under this scheme:

- Only part of the goods exempt from tax under the Value Added Tax Act of the concerned state.

- The registered person shall procure the documents for such goods and make available on records

- The registered person availing of this scheme and having furnished the details of stock held by the individual submits a statement in FORM GST TRAN 2. The taxpayer shall submit the form at the end of each of the six tax periods. The filing shall indicate the scheme operates with the details of supplies of such goods effected during the tax period.

- The amount of credit allowed shall be credited to the electronic credit ledger of the applicant maintained in FORM GST PMT-2 on the Common Portal.

- The stock of goods on which the credit is availed is so stored that it can be easily identified by the registered person.

The scheme for claiming GST input tax credit against VAT would be available for 6 months from the date of GST implementation.

GST TRAN-2 Form

GST TRAN-2 Form

GST Transitional Rules

To know more on the details to avail GST ITC scheme in the GST Transitional Rules, Scroll below: