Renu Suresh

Expert

Published on: Jun 24, 2026

Revised Guidelines Of Bonded Manufacturing Scheme

The Central Board of Indirect Taxes and Customs (CBIC) has notified the Revised Guidelines of

Bonded Manufacturing Scheme, which applies to the units under Section 65 of the Customs Act, 1962. This new guideline stipulates the procedure used for establishing and operating a customs warehouse. The current article briefs the Revised Guidelines Of Bonded Manufacturing Scheme in detail.Bonded Manufacturing Scheme

Bonded Manufacturing Scheme was introduced based on Section 65 of the Customs Act, 1962, which enables

manufacturers and other operations in a Customs bonded warehouse. The program has been launched vide the Manufacture and Other Operations in Warehouse Regulations, 2019. As part of this program, a unit can import goods (both inputs and capital goods) under customs duty deferment with no interest liability. There is no investment threshold or export obligation, and the duties are fully remitted if the goods resulting from such operations are exported. Import duty is payable only if the resulting goods or imported goods are cleared in the domestic market (ex-bonding).Salient features of the Bonded Manufacturing Scheme

The Salient features of the program areas explained in detail below:

- No geographical limitation on where such units can be set up

- A single application cum approval form for uniformity of practice with a single point of approval to set up the operations of such units

- Allows procurement of GST-compliant goods from the domestic market for use in the manufacture and other operations in a Section 65 unit

- Improved liquidity with the postponement of import duty and no interest liability

- A single digital account for ease of doing business and easy compliance

- Enables efficient capacity utilization, as there is no limit on the quantum of clearances that can be exported or cleared to the domestic market

Eligibility for applying for Manufacture and Other operations in a bonded warehouse

The following persons are eligible to apply for manufacture and other operations in a bonded warehouse:

- A person who has been granted a license for a warehouse under Section 58 of the Customs Act, following Private Warehouse Licensing Regulations, 2016

- A person can also make combined applications for a license for a warehouse under Section 58 of the Customs Act, along with permission to undertake manufacturing or other operations in the warehouse under Section 65 of the Customs Act.

Note: The persons must be a citizen of India or an entity incorporated or registered in India.

Eligibility Criteria for Factory

Any factory can avail of a license under Section 58 of the Customs Act and permission under Section 65 if they intend to import goods without upfront payment of Customs duty at the point of import and deposit them in the warehouse, either as capital goods or as inputs for further processing. Any unit in the Domestic Tariff Area (DTA) eligible for making an application for manufacture and other operations in a bonded warehouse that is an old factory in DTA is suitable for applying.

Prerequisite to obtaining a License

- The site or building should be suitable for the secure storage of goods and discharge of compliances.

- Depending on the nature of the goods used, the operations and the industry can operate without fully closed structures.

Note: The Principal Commissioner of Customs will consider the nature of the premises, the facilities, and equipment while considering the grant of license.

Renewal of the License

The license and permission for the unit are valid unless it is canceled or surrendered or the permit issued under Section 58 of the customs act is canceled or abandoned. Thus no renewal of the license under Section 58 or permission under Section 65 is required

Frequency of audit in unit operating in Customs Warehouse

The audit of units operating under Section 65 would also be based on risk criteria. There is no prescribed frequency for such an audit

Customs Document for the movement of imported goods

Following are the customs document for the training of imported goods on which duty has been deferred to a unit undertaking manufacture and other operations in a bonded warehouse:

- Customs Station to Section 65 unit: Bill of entry for warehousing

- From another warehouse (non-section 65) to a Section 65 Unit: Form for transfer of goods from a warehouse as prescribed under the Warehoused Goods (Removal) Regulations, 2016.

- From Section 65 Unit to another warehouse such as a Section 65 unit or a non-Section 65 warehouse: Form prescribed in Manufacture and Other Operations in Warehouse Regulations, 2019

Export of imported capital goods

The imported capital goods (on which duty has been deferred) after use in a Section 65 unit can be exported without payment of duty as per Section 69 of the Customs Act.

Warehouse Keepers’ Appointment

A warehouse keeper needs to be appointed for a premise to be licensed as a private warehouse under Section 58 of the Customs Act.

- The warehouse keeper needs to discharge duties and responsibilities, maintain accounts and sign the documents on behalf of the licensee.

- The warehouse keeper needs to supervise and satisfy himself about the integrity of the declaration/accounts he is signing.

- The inspection of goods by customs at the stage of ex-bonding would be done only if there is an indication of risks and not as a routine practice.

- Approval of the bond officer is not required for clearance of the goods from the warehouse.

Procedure and Documentation for re-entry of goods

Once the goods are cleared from the warehouse, they will no longer be treated as warehoused goods. Thus if the resultant goods removed from the warehouse are returned by the customer for repair, they will be entered as DTA receipts. After restoration, when the same is cleared from the warehouse, the same will be entered in the prescribed accounting form. If the goods were exported and subsequently rejected or sent back for repair by the customer, the goods upon re-import have to be entered as Imports receipts in the accounting firm. The relevant customs notification for re-imports must be followed while filing the Bill of Entry for re-importing the goods.

Hazardous cargo operation under Section 65

Hazardous cargo has to comply with all extant laws. Operating under Section 65 does not exempt units from compliance with any applicable laws.

Procedure for termination of operations in the bonded warehouse/ surrender of license

The procedure for surrendering the license will be per regulation 8 of the Private Warehouse Licensing Regulations, 2016.

- A licensee may, therefore, surrender the license granted to him by requesting in writing to the Principal Commissioner of Customs or Commissioner of Customs.

- On receipt of such request, the license will be canceled subject to payment of all dues and clearance of remaining goods in the such warehouse.

- Thus, duty on the remaining bonded inventory must be paid before surrendering the license.

- In case the bonded goods are desired to be exported, the exact needs to be done before surrendering the license.

Documents required

- Certificate of Incorporation (For companies)

- MoO and AoA (For partnership firm)

- Partnership Deed (For partnership firm)

- Copy of ID proofs of proprietors/ partners/ directors

- Copy of Aadhar Card of Authorised Signatory

- Documents supporting property-holding rights, such as rent agreement

- Copy of warehouse license, if issued earlier

- Ground plan of the site with details

- Fire safety audit certificate

Procedure to get a License to Start Manufacturing

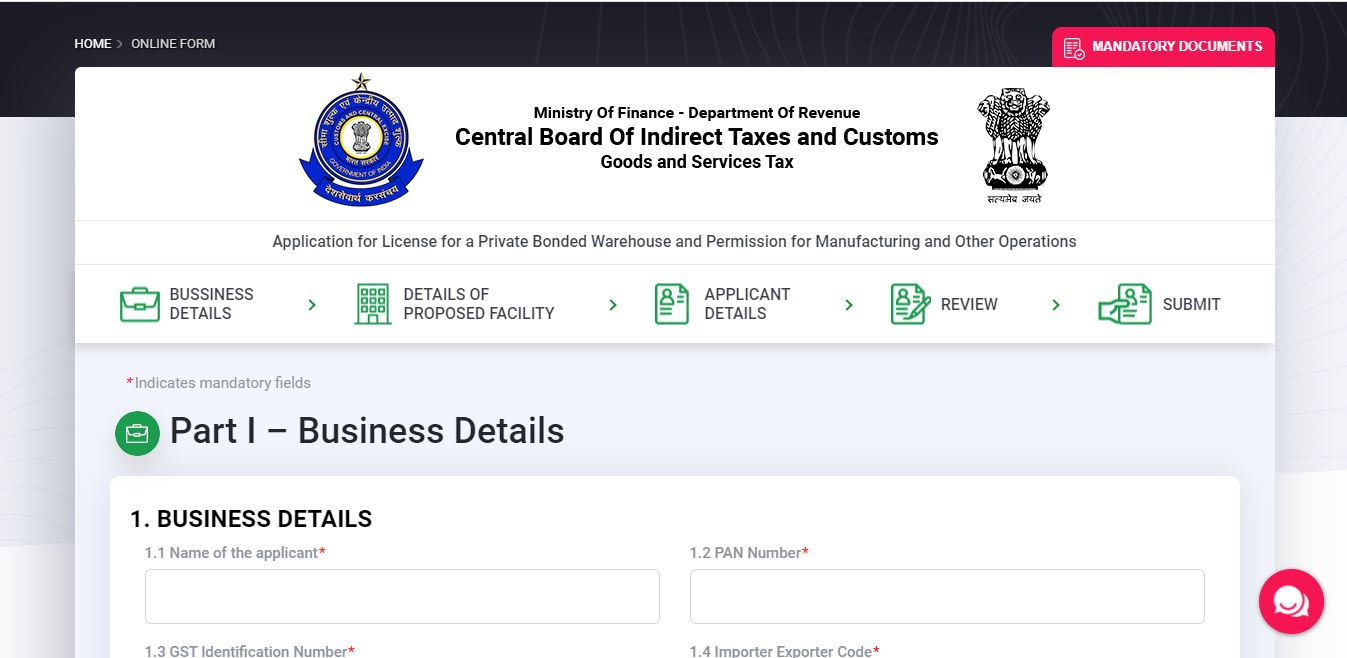

Access the official website of Invest India and Click on the new application option under the

Bonded manufacturing scheme page. Provide the following details Revised Guidelines Of Bonded Manufacturing Scheme - Application1

Revised Guidelines Of Bonded Manufacturing Scheme - Application1

- Business Details

- Constitution of Business

- Registered Office Details

- Bank Details

- Details Of Proprietor/Partner/Director

- Authorized Signatory

- Details Of Existing Manufacturing Facility In India

- Details Of Proposed Facility

- Warehouse License Issued Earlier

- Description of Premises:

- Goods Proposed To Be Manufactured or Other Operations Proposed To Be Carried Out

- Security Facilities at the Premise, Existing Or Proposed

- Applicant Details

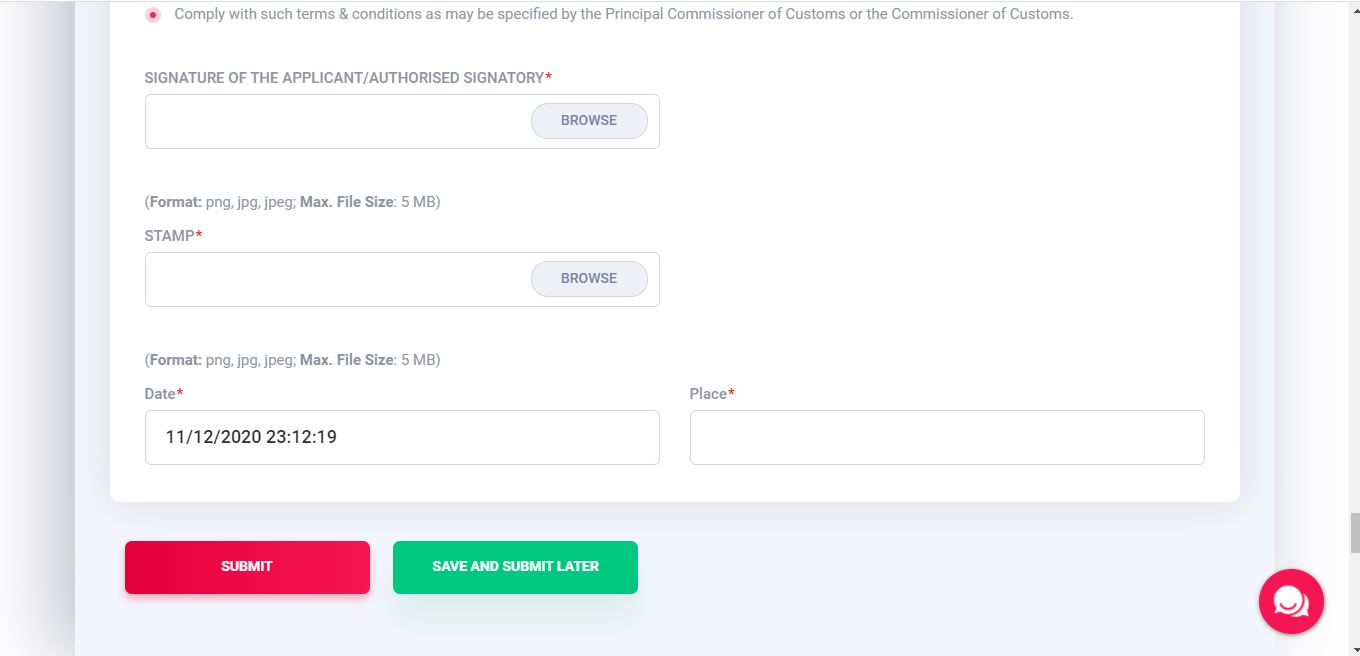

Revised Guidelines Of Bonded Manufacturing Scheme - Application2

After providing the details, click on the submit option. After verification of more information, the license will be issued to the applicant.

Revised Guidelines Of Bonded Manufacturing Scheme - Application2

After providing the details, click on the submit option. After verification of more information, the license will be issued to the applicant.

Revised Guidelines of Bonded Manufacturing Scheme - Application3

The official notification about the Revised Guidelines Of Bonded Manufacturing Scheme is as follows:

Revised Guidelines of Bonded Manufacturing Scheme - Application3

The official notification about the Revised Guidelines Of Bonded Manufacturing Scheme is as follows: