Bonded Manufacturing Scheme

To support the “Make in India” program, the Central Board of Indirect Taxes and Customs has implemented a revamped and streamlined program called Bonded Manufacturing Scheme. This scheme is expected to attract investments into India and strengthen Make in India through manufacturing and other operations. The bond scheme is under the Customs Act 1962. Section 65 of the Customs Act, 1962, through which the conduct of manufacture and other operations in a customs bonded warehouse is implemented.

Please refer notification from the Ministry of Finance, dated 15th October 2019, below:

Overview

Through the Bonded Manufacturing Scheme, the Government of India is promoting India as a manufacturing hub through which the scheme allows duty-free import of raw materials and goods for manufacturing and other operations in a customs-bonded manufacturing facility.

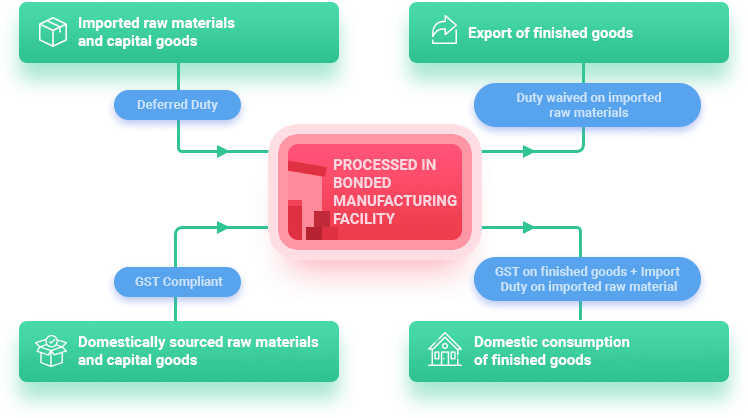

The import duty on them is deferred when the raw materials or capital goods are imported.

- If the imported inputs are utilized for exports, the deferred duty is entire.

- The import duty is applicable only when the finished goods are transferred to the domestic market. Also, the import duty applies only to the raw materials used in production.

Eligibility

The applicant should adhere to the applicable provisions of the Customs Act 1962 and other relevant rules and regulations issued by the Government of India for business within India. Refer below image to understand the applicability of import duty or tax.

Bonded Manufacturing Scheme. Courtesy:

Bonded Manufacturing Scheme. Courtesy:

Advantages of Bonded Warehousing

Deferred duty on capital goods - The import duty on capital goods used in manufacturing or other operations is deferred until the finished products are cleared from the bonded facility. Also, capital goods can be sold to foreign manufacturers (i.e., exported) after utilization, and deferred duty can be avoided or adjusted with the other applicable taxes.

Deferred duty on imported raw materials - Duty on imported raw materials used in manufacturing or other operations is deferred until the manufactured goods are cleared to domestic markets. And also, the deferred duty is waived if the finished goods are exported.

Seamless warehouse-to-warehouse Transfer - Goods can be transferred from the bonded facility to another facility without payment of duty.

No fixed export obligation - There is no limit on the export and domestic market share to clear the finished goods. A business entity can manufacture in a bonded facility and sell 100% of the output in the domestic market.

Ease of Bonded Manufacturing

- Approval of a unit - Commissioner of Customs acts as the single point of contact for all approvals

- Common application form - Single common application form is available online to get a license for a private bonded facility. The same application covers permission for manufacturing and other operations as well.

- Unlimited period of warehousing - Capital and non-capital goods (raw materials, components, etc.) can remain warehoused until clearance by export or by domestic consumption

- No geographical restriction - The manufacturing facility can be set up, or an existing facility can be converted into a bonded manufacturing facility, and the location can be anywhere in India.

- Easy compliance - Maintain all manufacturing and other operations records digitally in a single format as per Annexure B, which is provided below for quick reference.

Annexure B_Bonded Manufacturing Scheme

Types of Beneficiaries

Export: All businesses can avail of exemption on customs duty on imported inputs used in the production of finished goods to be exported through bonded manufacturing.

Domestic: The duty on imported inputs is deferred until the finished goods are cleared to the domestic market.

- As explained above, the manufacturer benefits from deferred duty on imported inputs, leading to reduced production cost.

- There is no timeline to store the goods in the warehouse as the goods can be stored until it moves to other storage units or till the manufacture gets over, or till the manufactured goods are exported.

- The duty on imported goods can be paid only when the finished goods are cleared from the facility to the domestic market.

Two different scenarios are covered under this scheme, and they are:

- Steps to Start Manufacturing

- Steps for Clearance of Warehoused Goods

The methodology of availing the benefits when a unit takes part through the above mentioned different scenarios are explained below.

Steps to Start Manufacturing

Step-1

- Fill Online Application

- Fill online application as per Annexure-A along with the following details:

- Nature of manufacturing goods - Automobile, FMCG, etc.

- Particulars of imported goods

- Expected volume of trade, etc.

- List of documents required:

- Details of the company like Certificate of Incorporation or AoA or Partnership Deed, etc. (depends on the nature of the company)

- ID proofs of proprietors/partners/directors

- Aadhar Card of Authorised Signatory

- Property documents or Rental agreement

- Warehouse license, if issued earlier

- Ground plan of the site with details

- Audit certificate from fire department

Step-2

- Bond Execution

- A bond to be executed as per Annexure-C (Refer below) and to be submitted to the Commissioner of Customs under the jurisdiction of the business.

- Details as per Annexure-B

Note: A Customs Officer will visit the facility to evaluate the compliances in order to issue the license b

efore the execution of a Bond.

Step-3

- Grant of Sanction

- Permission is granted by the Commissioner of Customs for manufacturing or other operations in the bonded facility

- Permission also includes:

- Manufacturing process or other permitted operations

- Conditions regarding manufacturing

Step-4

Start Manufacturing or Other Operations

Note: The processes for availing the license for a private bonded facility (as per Section 58) and manufacturing or performing other operations (as per Section 65) are combined under single application as per

Annexure A.

Steps for Clearance of Warehoused Goods

- To the domestic market for consumption - When warehoused goods are used for manufacturing or other operations & finished goods are domestically consumed

- To a Customs Station for Export - When warehoused goods are used for manufacturing, or other operations & finished goods are exported

- To another bonded manufacturing facility - When imported goods are stored and used as raw materials by another industry

Warehoused goods are permitted for clearance after:

- The owner of goods meets all compliances as per the executed bond.

- Deferred duty on imported raw materials or capital goods is paid.

- GST is paid on the finished goods.

- Any other compliance as per the Customs Act or any other applicable regulations are met.

Follow Simple Steps to Transport Warehoused Goods

- Form for Transfer of goods to be filled from a facility appended as per Warehouse Goods (Removal) Regulations Act, 2016 to transport stored/warehoused goods.

- The authorized licensee of the originating warehouse should get permission from the respective Commissioner of Customs and had to disclose the nature of goods and mode of transport.

- ‘Acknowledgement’ received from the licensee of the recipient warehouse stating the arrival of goods to the Bond Officer of the originating warehouse to be produced.

- Acknowledgment is to be produced within one month.

*When the goods are transferred from one bonded facility to another, the responsibility of the deferred duty is also transferred to the new facility.

Requirements for Record-keeping

- Maintenance of records

-

- Receipts of handling, storing, and removal of goods into/from the facility as per Annexure B.

- Record each activity, operation, or action carried out to the stored goods.

- Copies of the following documents:

- Entry Bills

- Transport documents

- Forms for Transfer of goods from the warehouse

- Shipping Bills

- Export Bills

- Documents on receipt/removal of goods from the warehouse, if applicable

- Preservation of physical and digital records

-

- Per policy, the records of accounts should be preserved for a minimum of 5 years from the date of removal of goods from the warehouse.

- Digital copies of records should be preserved at a place other than a manufacturing or warehousing facility.

- Filing monthly returns

-

- File monthly returns within ten days of the closing of the month.

Note: If the licensees fail to comply with any of the provisions of the regulations, they are liable to a penalty as per the Customs Act, 1962.

Contact

INVEST INDIA

Vigyan Bhavan Annexe,

Maulana Azad Road,

New Delhi 110001, +91-11-23048155

To know more about this scheme, the entrepreneurs are requested to contact respective zonal Customs or Central Excise offices.

Revised Guidelines of Bonded Manufacturing Scheme

The Central Board of Indirect Taxes and Customs (CBIC) has notified the Revised Guidelines of

Bonded Manufacturing Scheme, which applies to the units under Section 65 of the Customs Act, 1962. This new guideline stipulates the procedure for establishing and operating a customs warehouse.