IndiaFilings

Expert

Published on: Apr 22, 2026

Records to be Maintained under GST

GST Laws in India mandate that all taxable persons under GST maintain the GST records and accounts in a specified manner. In this article, let us look at the list of records to maintain under GST in detail.

Place of Business

Under GST, the "place of business" includes:

- A place from where the taxpayer conducts the business and includes a warehouse, a godown or any other place where a taxable person stores his goods, supplies or receives goods or services or both; or

- A place where a taxable person maintains the books of account; or

- A place where a taxable person engages the business through an agent, by whatever name called;

Under GST, all registered taxpayers shall maintain certain documents at their place of business.

List of Documents required under GST

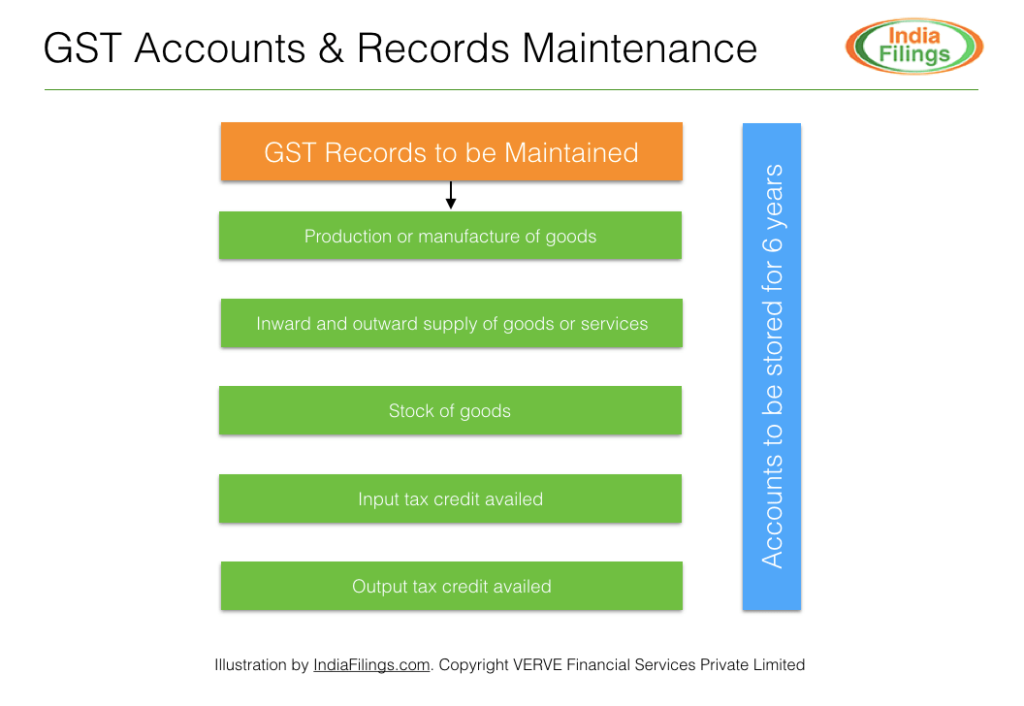

Under GST, all registered taxpayers are required to maintain the following accounts and records at the principal place of business:

- Details of production or manufacture of goods;

- Details of inward and outward supply of goods or services or both;

- The stock of goods;

- Input tax credit availed;

- Output tax payable and paid;

- Any other particulars as may be prescribed:

In case of more than one place of business, then the taxpayer shall keep the accounts relating to each of the places at that place of business. The taxpayer shall keep the accounts and records under GST in both electronic or book format.

GST Accounts & Records Maintenance

GST Accounts & Records Maintenance

Maintenance of Documents

The maintenance of records applies to both registered and unregistered persons. All the following persons shall maintain the records of

- Transporters of the consigner,

- Consignee and other details of the goods held or transported,

- Owners, operators of the warehouse,

- Godown or any other place used for storage of goods.

Further, transporters and owners of the godown or

warehouse shall obtain registration under GSTDuration for maintaining documents under GST?

All registered taxpayers shall maintain the book of accounts and other records for a period of 6 years from the due date of filing of annual return for the year. In case the taxpayer applied or involved in an appeal, revision or any other proceedings before any Appellate Authority or Revisional Authority or Appellate Tribunal or court, then the taxpayer shall maintain the accounts and books for a period of one year, after final disposal of such appeal or revision or proceedings or investigation, or for 6 years. The duration applies for the period that acts late.

To GST registration and documentation, click here