Renu Suresh

Expert

Published on: Apr 21, 2026

Pradhan Mantri Awas Yojana (PMAY)

PMAY or Pradhan Mantri Awas Yojana Programme is a scheme launched by the Ministry of Housing and Urban Poverty Alleviation (MoHUPA) to provide housing for all by 2022. In order to empower people to get their dream home, Honourable Prime Minister of India has announced this comprehensive and progressive mission on 17 June, 2015. In this article, we look at the PMAY scheme in detail.Objective of PMAY Scheme

The Mission seeks to address the housing requirement of urban poor including slum dwellers through following programme verticals:- Slum rehabilitation of Slum Dwellers with participation of private developers using land as a resource. (Slum is a compact area of at least 300 populations or about 60-70 households of poorly built congested tenements, in unhygienic environment usually with inadequate infrastructure and lacking in proper sanitary and drinking water facilities)

- Promotion of affordable housing for weaker section through credit linked subsidy.

- Affordable housing in partnership with Public & Private sectors.

- Subsidy for beneficiary-led individual house construction or enhancement.

PMAY Scheme Beneficiaries

The Pradhan Mantri Awas Yojana Beneficiaries are discussed below.- Mani focus of the schemes is woman, economically backward groups of Indian society.

- To protect transgender and widows, members of the lower income groups and urban poor.

- Scheduled Castes and Scheduled Tribes shall be granted preference when they try to avail the affordable housing scheme.

- Older and Differently abled persons will be given preference in the allotment of ground floors under the Pradhan Mantri Awas Yojana scheme.

Benefits under PMAY Scheme

- Interest subsidy of 6.5 percent on housing loan will be provided for 15 years to the beneficiaries.

- Eco friendly and sustainable technologies will be used during the construction process.

- The scheme covers entire urban areas in the country which includes 4041 statutory towns with the first priority given to 500 Class I cities. This will be done in 3 phases.

- The credit linked subsidy aspect of the PM Awas Yojana gets implemented in India in all statutory towns from the initial stages itself.

PMAY Scheme Subsidy

The credit linked subsidy scheme (CLSS) on home loans under the Pradhan Mantri Awas Yojana – Housing for all, for purchase/ construction/ extension/ improvement of house to cater Economical Weaker Section (EWS)/Lower Income Group (LIG)/Middle Income Group (MIG). Beneficiaries can seek housing loans from Primary Lending Institutions (PLI) for new construction and enhancement to existing dwellings as incremental housing. The credit linked subsidy will be available only for loan amounts up to Rs 6 lakhs and such loans would be eligible for an interest subsidy at the rate of 6.5 % for tenure of 20 years or during tenure of loan whichever is lower. Total interest subsidy available to each beneficiary under this component is Rs.2.30 lakhs.Economical Weaker Section (EWS)

EWS households are defined as households having an annual income up to Rs. 300000 (Rupees Three Lakhs). States/UTs shall have the flexibility to redefine the annual income criteria as per local conditions in consultation with the Centre.Low Income Group (LIG):

LIG households are defined as households having an annual income between Rs.3,00,001 (Rupees Three Lakhs One) up to Rs.6,00,000 (Rupees Six Lakhs). States/UTs shall have the flexibility to redefine the annual income criteria as per local conditions in consultation with the Centre.Middle Income Group (MIG)

Under CLSS, middle income beneficiaries with annual household income between Rs.6 lakh and Rs.12 lakh (categorised as MIG I) would get an interest subsidy of 4.00% on a 20-year loan component of up to Rs.9 lakhs. Those with annual household incomes of more than Rs12 lakh and up to Rs18 lakh (categorised as MIG II) would get interest subsidy of 3.00% on a 20-year loan component of up to Rs12 lakh. Additional loans beyond the specified limit, if any, will be at the non-subsidized rates.Primary Lending Institutions (PLI)

PLI are Scheduled Commercial Banks, Housing Finance Companies, Regional Rural Banks (RRBs), State Cooperative Banks, Urban Cooperative Banks.Eligibility for CLSS

- The scheme is offered to families, comprising of husband, wife and unmarried children.

- An adult earning member irrespective of marital status can be treated as a separate household in MIG category.

- The family should not own a pucca house in his/ her name or in the name of any member of the family, in any part of India.

CLSS scheme details

| Scheme Type | Eligibility Family Income (Rs.) | Carpet Area-Max (sq. m.) | Subsidy calculated on a max loan of | Interest Subsidy (%) | Max Subsidy (Rs.) | Validity of scheme | Woman Ownership |

| EWS | 0 to 300000 | 30 | 600000 | 6.50 | 2.67 Lakh | 31/3/2022 | Mandatory |

| LIG | 300001 to 600000 | 60 | 600000 | 6.50 | 2.67 Lakh | 31/3/2022 | Mandatory |

| MIG- I | 600001 to 1200000 | 120 | 900000 | 4.00 | 2.35 Lakh | 31/3/2022 | |

| MIG-II | 1200001 to 1800000 | 150 | 1200000 | 3.00 | 2.30 Lakh | 31/3/2022 |

Note: The House constructed/acquired should be in the name of female head of the household or in the joint names of male head of the household and his wife. Only in cases, where there is no adult female member in the family, the house can be in the name of male member of the household. However this stipulation is applicable only for new purchases and not for new construction (on an existing piece of land).

PMAY Scheme Online Application

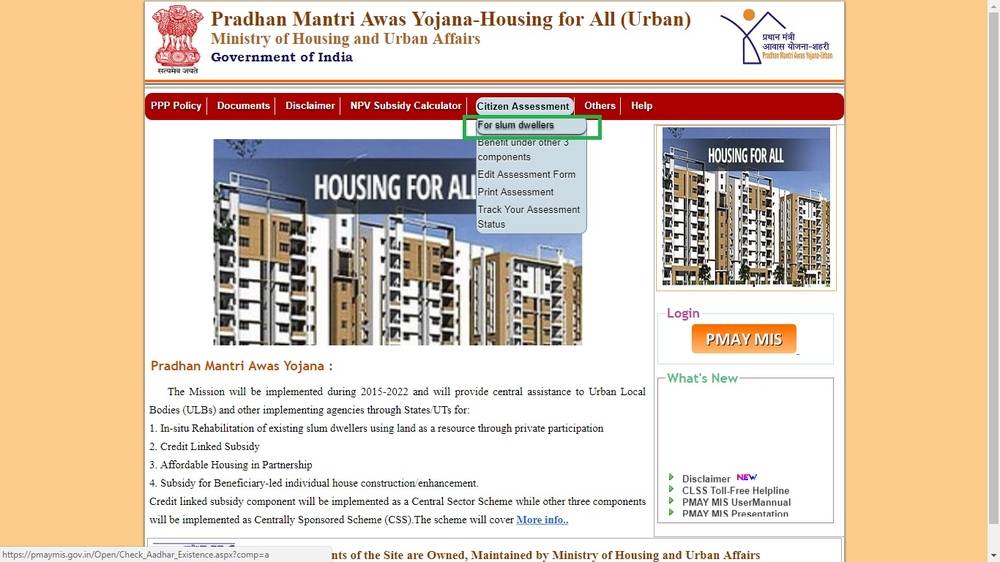

Step 1: Visit the PM Awas Yojana official website Step 2: Under the “Menu” section, find the “Citizen Assessment” option Step 3: Select For slum dwellers Image 1 PMAY

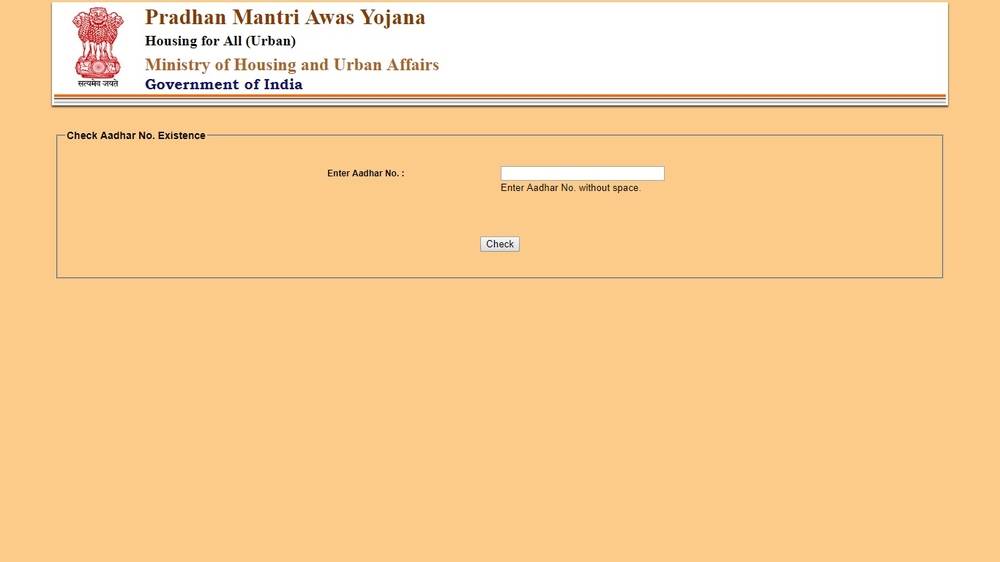

Step 4: Enter your 12-digit Aadhaar card number

Image 1 PMAY

Step 4: Enter your 12-digit Aadhaar card number

Image 2 PMAY

Step 5: Once you have entered your Aadhar information, you will be redirected to the application page

Stew 6: You will be asked to enter your personal details, income details, current residential address, and your bank account details

Step 7: Enter all information in the application

Step 8: Click on “I am aware of” option at the end of the page and click the “Save” button

Step 9: Once you click the “save” option, you will see a system generated application number which you can save for future reference

Step 10: Download and print the duly-filed application

Step 11: Submit the form at your nearest CSC office centres and financial institution/banks along with the required documents.

Step 12: If eligible for subsidy, your application will be forwarded to the Central Nodal Agency (CNA).

Step 13: If it's approved, the CNA will disburse the subsidy amount to the lender.

Step 14: This will be credited to your account, thus reducing the total loan amount.

For instance, if your annual income is Rs 7 lakhs and the loan amount is Rs 9 lakhs, the subsidy will be Rs 2.35 lakhs. If the loan amount is higher than the maximum amount eligible for subsidy, the excess will attract interest at the prevalent rate.

Image 2 PMAY

Step 5: Once you have entered your Aadhar information, you will be redirected to the application page

Stew 6: You will be asked to enter your personal details, income details, current residential address, and your bank account details

Step 7: Enter all information in the application

Step 8: Click on “I am aware of” option at the end of the page and click the “Save” button

Step 9: Once you click the “save” option, you will see a system generated application number which you can save for future reference

Step 10: Download and print the duly-filed application

Step 11: Submit the form at your nearest CSC office centres and financial institution/banks along with the required documents.

Step 12: If eligible for subsidy, your application will be forwarded to the Central Nodal Agency (CNA).

Step 13: If it's approved, the CNA will disburse the subsidy amount to the lender.

Step 14: This will be credited to your account, thus reducing the total loan amount.

For instance, if your annual income is Rs 7 lakhs and the loan amount is Rs 9 lakhs, the subsidy will be Rs 2.35 lakhs. If the loan amount is higher than the maximum amount eligible for subsidy, the excess will attract interest at the prevalent rate.

Check PMAY Beneficiary List

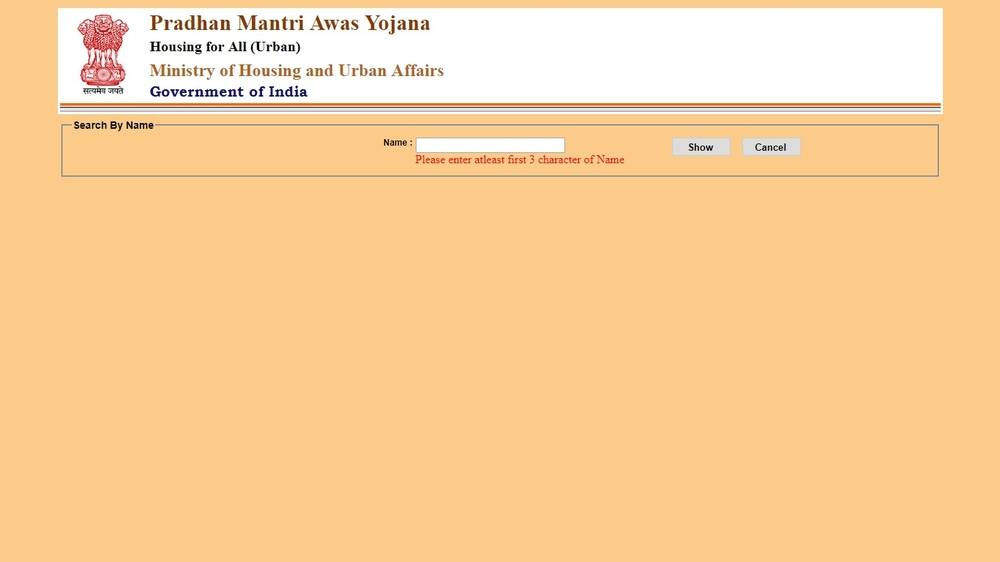

The list of beneficiaries of PM Awas Yojana is however not available to download but one can verify whether his/her name is present in the list of beneficiary or not. There is a simple procedure to check your name in the PMAY beneficiary list as below. Step 1: Search Name Image 3 PMAY

Step 2: Enter the name or the first three letters of the name and click “SHOW” button.

Step 3: After clicking the “SHOW” button, a list of PMAY beneficiaries matching your name would be displayed.

Now you can verify your existence in the list by matching your name against your father’s name, gender, religion, city or state name.

Step 4: You can view the complete details by clicking the beneficiary name and then entering your mobile number and verifying it with the OTP.

Image 3 PMAY

Step 2: Enter the name or the first three letters of the name and click “SHOW” button.

Step 3: After clicking the “SHOW” button, a list of PMAY beneficiaries matching your name would be displayed.

Now you can verify your existence in the list by matching your name against your father’s name, gender, religion, city or state name.

Step 4: You can view the complete details by clicking the beneficiary name and then entering your mobile number and verifying it with the OTP.