IndiaFilings

Expert

Published on: Jun 24, 2026

LLP Tax Filing - Income Tax Rate & Deadline

LLP or Limited Liability Partnership is a corporate entity formed under the Limited Liability Partnership Act, 2008. LLPs have a separate legal identity and are required to file MCA annual return (Form 8 and Form 11) and income tax return each year. In this article, we look at the compliances required for a LLP during the financial year 2018.2018 LLP Income Tax Rate

In the year 2018, the income tax return for FY2017-18 or AY2018-19 would be filed by the LLP. The income tax rate applicable for LLP registered in India is a flat 30% on the total income for the financial year 2017-18. In addition to the income tax, a surcharge is levied on the income tax payable at the rate of 10% when the total income exceeds Rs.1 crore. In addition to income tax surcharge, an education cess and secondary and higher education cess is also applicable on the income of a LLP.

Education Cess

Education cess of 2% is applicable on the amount of income tax and the applicable surcharge.

Secondary and Higher Education Cess

Secondary and higher education cess of 1% is applicable on the amount of income tax and the applicable surcharge.

Minimum Alternate Tax (MAT) for LLP

LLP is subject to minimum alternate tax. Hence, the income tax paid by a LLP having profits cannot be less than 18.5% of the adjusted total income of the LLP. The MAT is increased by income tax surcharge, education cess and secondary and higher education cess.

2018 Deadline for LLP Tax Filing - AY2018-19

The deadline for LLP income tax return for a LLP is July 31st if tax audit is not required. In the year 2018, the income tax return for FY2017-18 or AY2018-19 would be filed by the LLP. LLP whose turnover exceeded Rs. 40 Lakh or whose contribution exceeded Rs. 25 Lakh are required to get their accounts audited by a practising Chartered Accountant. The deadline for tax filing for LLP required to obtain audit is September 30th. Finally, LLPs that entered into an international transaction with associated enterprises or undertook certain

Specified Domestic Transactions are required to file Form 3CEB. Form 3CEB must be certified by a Chartered Accountant. LLPs required to file Form 3CEB have 3oth November as the deadline for LLP tax filing.ITR-5 LLP Income Tax Filing Form

LLPs must file income tax return using Form ITR 5. Form ITR 5 can be filed online through the income tax website using the

digital signature of the designated partner. After filing LLP tax return, it is advisable for the taxpayer to print two copies of Form ITR-V. One copy of ITR-V, signed by the assessee should be sent by ordinary post to Post Bag No. 1, Electronic City Office, Bengaluru–560100 (Karnataka). The other copy can be retained by the assessee for his record. The ITR-5 for AY2018-19 is reproduced below for reference:LLP Advance Tax Payment

LLPs are required to comply with

advance tax payment regulations. Hence, LLPs should have calculated their income tax liability and paid upto 100% of the advance tax payment on or before 15th March, 2018. The due dates for LLP advance tax payment are as follows:| Taxpayer Type | By 15th June | By 15th September | By 15th December | By 15th March |

| All types of taxpayers (other than those who opted for presumptive taxation scheme) | Upto 15% of advance tax | Upto 45% of advance tax | Upto 75% of advance tax | Upto 100% of advance tax |

| Taxpayers who opted for presumptive taxation scheme | NIL | NIL | NIL | Upto 100% of advance tax |

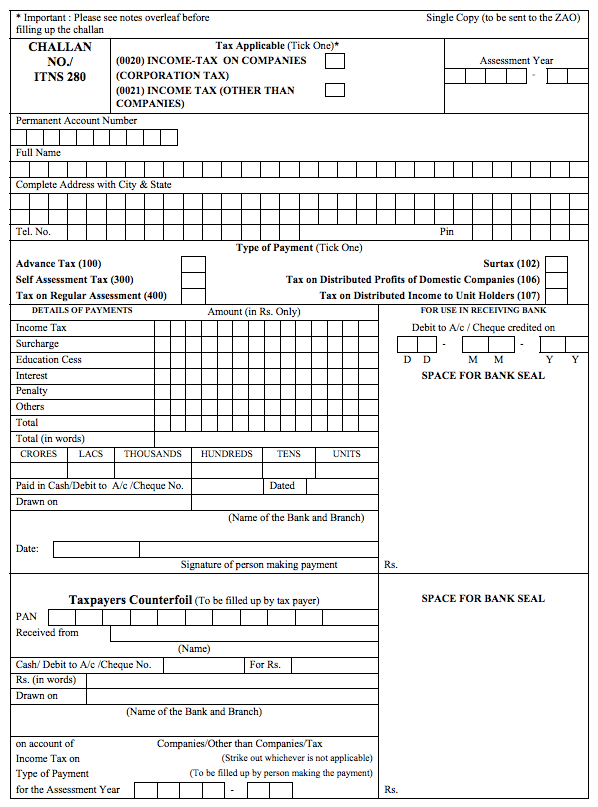

LLP tax payment can be made in physical mode through designated banks or through

e-payment mode. LLPs that are required to get its accounts audited are required to pay tax through e-payment mode only. To pay tax at designated banks, Challan ITNS 280 as provided below must be provided with the tax payment. Challan ITNS 280

Challan ITNS 280