IndiaFilings

Expert

Published on: Apr 22, 2026

Limited Liability Partnership - LLP Taxation

Limited liability partnership (LLP) is a relatively new type of business entity in India. Previously, there used to be concerns whether a LLP would be taxed like a Private Limited Company or Partnership Firm. However, the Finance Act, 2009 has amended the Income Tax Act and confirmed that LLP would be taxed like a Partnership Firm. In this article, we look at the major aspects of LLP taxation in India.

Private Limited Company Taxation Policy

To compare and contrast, we first look at Private Limited Company taxation policy. A private limited company is treated as a separate legal entity and its income is taxed at the rate of 30%. In addition to the income tax, education cess of 2% and 1% secondary and higher education cess is also levied. A surcharge of 5% is applicable when the taxable income exceeds Rs.1 crore.

In addition to the income tax, if the private limited company declares dividends, then the dividend payable attracts dividend tax of 15% plus 2% education cess and 1% secondary and higher education cess plus surcharge of 10%. The total dividend tax works out to 16.995% under Section 1150. Once the dividend tax is paid by the company, the dividend received by the shareholder of the company is exempt from Income Tax.

LLP Taxation Policy

The LLP taxation policy is similar to that of a Partnership firm. From assessment year 1993-94, a partnership firm is treated as a separate taxable entity and has to pay tax on its income. Income of a partnership firm is taxed at 30% plus 2% education cess plus 1% secondary and higher education cess - similar to a private limited company.

Taxation on LLP Partner Remuneration & Interest

A partner can claim deduction for remuneration and interest on capital provided by them to the LLP while arriving at the taxable income for the Limited Liability Partnership. However, to claim partner remuneration and interest on capital, there must be specific provision in the LLP Agreement. The LLP Agreement must specially and unambiguously have clauses that allow for payment of remuneration and interest on capital and loan provided by the Partners. The remuneration is payable only to individual LLP Partner who are actively engaged in conducting the affairs of the business or profession of the LLP firm.

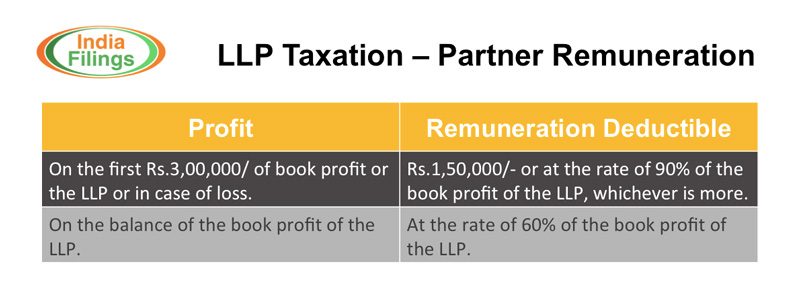

Remuneration for LLP Partner can be deducted from the LLP as follows:

LLP Taxation Partner Remuneration

LLP Taxation Partner Remuneration

LLP Partner Income

The receipt of remuneration and/or interest from the LLP is taxed as business income in the hands of the LLP Partner. Hence, the expenses incurred by the LLP partner for business purpose like interest payments and business loss of propriety business, if any, can be set off against receipt of interest and remuneration. No TDS deduction is necessary from the LLP while making payment of interest and remuneration payment to LLP Partners.

LLP Income Tax Surcharge

With effect from Financial Year 2013-14, assessment year 2014-15, a surcharge of 10% is applicable if the income of the Partnership firm or Limited Liability Partnership exceeds Rs.1 crore.

LLP Tax Return Filing

All LLPs are required to file Income Tax return each year on or before 30th September. The income tax return of a LLP must be signed by the Designated Partner. If the designated partner is not able to sign the income tax return of the LLP for any unavoidable reason, then it can be signed by any of the other Partners.