IndiaFilings

Expert

Published on: Jun 24, 2026

Implications Of Cheque Bounce In India

In India, a person issuing a cheque will be committing a criminal offence if the cheque is dishonoured (cheque bounce) for insufficiency of funds. A cheque bounce offence is punishable with imprisonment for a term of up to two years or with a fine twice the amount of the cheque or both. Therefore, it is important for small & medium-sized businesses to understand their rights & responsibilities of a cheque bounce and maintain financial discipline to avoid such instances.

Cheque-Bounce-Section-138-Notice-Process

Cheque-Bounce-Section-138-Notice-Process

When a cheque is considered bounced?

In specific conditions, the bank may refuse payment of a cheque or will dishonour a cheque; the cheque will bounce in such cases. When the cheque is dishonoured for insufficiency of funds in the account of a customer, that cheque bounce is treated as an offence and action can be taken under Section 138 of The Negotiable Instruments Act.

What are the steps to initiate prosecution for a cheque bounce?

To initiate prosecution under Section 138, fulfil the three condition precedents as below:

- Provide the cheque to the bank within three months of its issue or within the period of its validity. (The validity of cheques were considered to be six months previously; however, Reserve Bank of India vide Notification No. RBI/2011-12/251DBOD.AML BC.No.47/14.01.001/2011-12 directed that the validity period of cheques to be reduced from six months to three months with effect from 1st April, 2012.).

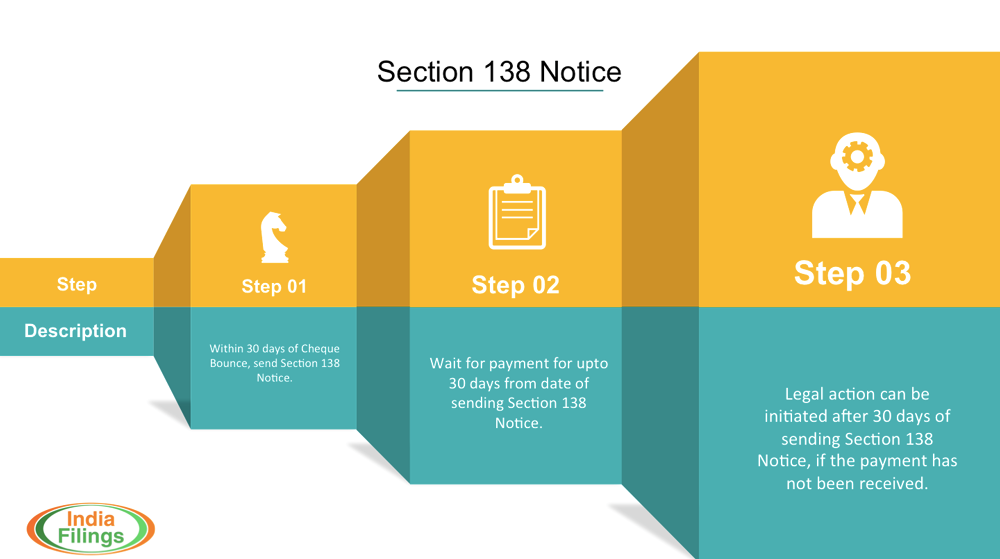

- The payee [Person who receive the money] should have made a demand to the Payor [Person who is liable to pay the money] for payment by registered notice after the cheque is returned unpaid.

- The Payor should have failed to pay the amount within 30 days of the receipt of the notice.

- Only on satisfying all the above three conditions, the prosecution can be launched for the offence under Section 138.

How and when to give notice of dishonour?

The payee has to make a demand for the payment of money to the payor by giving notice to the payor within 30 days of the receipt of information by him from the bank regarding the return of the cheque as unpaid. Therefore, to protect his rights under Section 138, the payee [affected party] has to make a demand to the payor within 30 days by giving notice that the person has a statutory obligation to make payment. As long as the payee sends a notice to the payor at the correct address, it considers fulfilling all the responsibilities of the payee.

When can prosecution be launched under Section 138?

A person can launch Prosecution against the payor under Section 138 if the payor failed to pay the amount within 30 days of the receipt of notice from the payee. A Cheque Bounce Notice under Section 138 can be found or generated using MakeMyDeed.

Who can the prosecution under Section 138 be launched against?

A person can launch Prosecution against the payor and in the case where a company has committed an offence under Section 138, then not only the company but also every person who at the time when the offence committed, was in charge of and was responsible to the company will deem to be guilty of the offence and be liable to be proceeded against.

What are the other implications of a cheque bounce?

In addition to the criminal offence, bounced cheques can also impact creditworthiness or credit history. Though bounced cheques don't usually show up on traditional credit reports, they reflect on the bank account statement. Banks both Nationalized & NBFC’s today require the customer to furnish their bank statement for a period of up to 1 year for any loan processing. The occurrence of many cheque bounces in a bank statement can affect loan eligibility and creditworthiness.

How to avoid cheque bounces?

The best policy to avoid a cheque bounce in your account is to NEVER write a cheque without money in your account. Providing a cheque to a person is a firm financial commitment, an individual can make to the person which has a lot of responsibilities and implication in case it is not honoured. Therefore, it is best not to provide a cheque to a person without money in your account- just to temporarily avoid financial pressure.

To know more about cheque bounces or to talk to our Business Consultants, visit IndiaFilings.com