Renu Suresh

Expert

Published on: Jun 24, 2026

Gst Exemption Limit In India

A common question among businesses in India is whether all businesses need to register for GST and if there are any exemptions. What is the minimum turnover limit for GST registration? To support smaller businesses and streamline the compliance process, the GST framework includes specific exemption limits. These thresholds are pivotal for small and medium-sized enterprises (SMEs), determining when a business is required to register and pay GST. Currently, businesses dealing in goods must register if their annual revenue exceeds Rs. 40 lakhs, while service providers have a threshold of Rs. 20 lakhs. In this article, we explore the GST registration limit for various businesses. We also delve into how to calculate annual turnover for GST and the potential disadvantages of non-compliance. Ensure your business is GST-compliant with ease. Start your GST registration today with IndiaFilings and benefit from our expert guidance and support!GST Exemption Limit

Under the Goods and Services Tax (GST) regime in India, businesses whose annual revenue exceeds specific thresholds are required to register and pay GST. Currently, the GST Exemption Limit is set at Rs. 40 lakhs for goods and Rs. 20 lakhs for services. Businesses with annual revenues below these limits are not mandated to register for GST; however, they may opt to do so voluntarily.- It's important to note that special category states in India have different threshold limits due to their unique economic environments.

- For these states, the GST exemption limit for the supply of goods is set at Rs. 20 lakhs and for services at Rs. 10 lakhs.

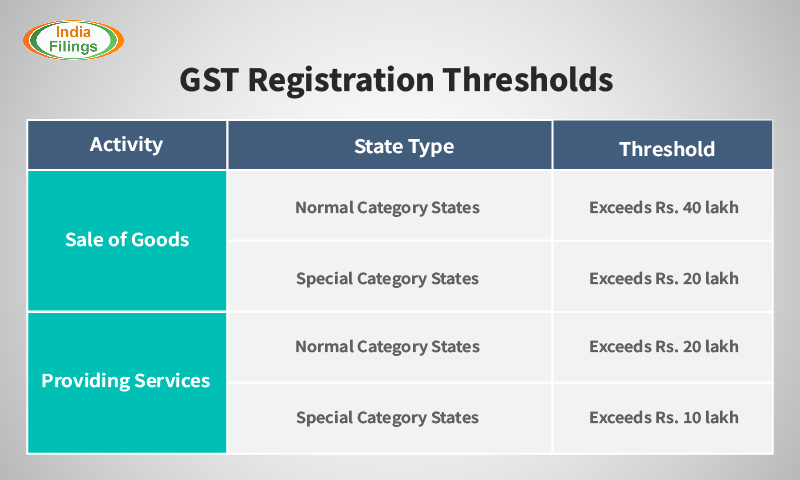

Overview of GST Registration Thresholds: Previous and Updated Limits

Previous Limits (Until March 31, 2019):

Sale of Goods/Providing Services:- Normal Category States: Registration is required if turnover exceeds Rs. 20 lakh.

- Special Category States: Registration is required if turnover exceeds Rs. 10 lakh.

Updated Limits (Effective from April 1, 2019):

For Sale of Goods:- Normal Category States: Registration is required if turnover exceeds Rs. 40 lakh.

- Special Category States: Registration is required if turnover exceeds Rs. 20 lakh.

- There has been no change in the registration thresholds for service providers. Registration is mandatory if turnover exceeds Rs. 20 lakh in normal category states and Rs. 10 lakh in special category states.

GST Thresholds

The following table provides a clear overview of the GST registration thresholds before and after the update on April 1, 2019, for both selling goods and providing services, across different state categories.

GST Thresholds

The following table provides a clear overview of the GST registration thresholds before and after the update on April 1, 2019, for both selling goods and providing services, across different state categories.

| Activity | State Type | Threshold Until Mar 31, 2019 | Threshold From Apr 1, 2019 |

| Sale of Goods | Normal Category States | Exceeds Rs. 20 lakh | Exceeds Rs. 40 lakh |

| Special Category States | Exceeds Rs. 10 lakh | Exceeds Rs. 20 lakh | |

| Providing Services | Normal Category States | Exceeds Rs. 20 lakh | Exceeds Rs. 20 lakh (No change) |

| Special Category States | Exceeds Rs. 10 lakh | Exceeds Rs. 10 lakh (No change) |

Classification of States for the Applicability of New GST Turnover Limits

In response to the changes in GST exemption limits, states and Union Territories (UTs) in India were given the option to adopt new limits or maintain the existing ones. Here’s a breakdown of the choices made by various states: Normal Category States/UTs Opting for New Limit of Rs. 40 Lakh The following states and UTs have opted to increase the GST registration exemption limit to Rs. 40 lakh for the sale of goods:- Kerala, Chhattisgarh, Jharkhand, Delhi & Bihar

- Maharashtra, Andhra Pradesh, Gujarat, Haryana & Goa

- Punjab, Uttar Pradesh, Himachal Pradesh & Karnataka

- Madhya Pradesh,Odisha, Rajasthan & Tamil Nadu

- West Bengal, Lakshadweep, Dadra and Nagar Haveli and Daman and Diu

- Andaman and Nicobar Islands, Chandigarh

- Telangana has chosen to maintain the earlier limit of Rs. 20 lakh.

- Jammu and Kashmir

- Ladakh

- Assam

- Puducherry, Meghalaya, Mizoram & Tripura

- Manipur, Sikkim, Nagaland, Arunachal Pradesh & Uttarakhand

Categories with Compulsory GST Registration Requirements

Regardless of turnover, certain categories of persons must compulsorily register under GST. These include:- Interstate Suppliers: Those who supply goods and services across state lines.

- Casual Taxable Persons: Individuals who occasionally undertake transactions involving the supply of goods or services, either in a state where they have no fixed place of business or from more than one state.

- Persons Taxable Under Reverse Charge Basis: Individuals who are liable to pay GST under the reverse charge mechanism.

- Non-resident Taxable Persons: Those who reside outside India but supply goods or services to residents within India.

- Persons Required to Deduct TDS Under GST: Entities that are mandated to deduct tax at source under GST regulations.

- Persons Required to Deduct TCS Under GST: Those required to collect tax at source.

- Input Service Distributors: Entities that receive invoices for services used at multiple locations, which are then distributed to these locations.

- Persons Making a Sale on Behalf of Someone Else: This applies whether acting as an agent or principal.

- E-commerce Operators: Those providing a platform for others to supply goods or services through it.

- Suppliers Who Supply Goods Through E-commerce Operators: These operators are responsible for collecting tax at source.

- Online Service Providers from Outside India: Providers who offer services from abroad to non-registered persons in India.

GST Exemption Limit for the GST Composition Scheme

The GST Composition Scheme is an alternative method of tax levy under the GST framework designed to simplify the compliance burden for small businesses. By opting for this scheme, eligible companies can benefit from lower tax rates and simpler procedural requirements. The scheme allows for quarterly tax payments and annual GST return filings, making it a viable option for small taxpayers seeking to reduce compliance complexity and administrative overhead.Updated Provisions in the Composition Scheme

Enhanced Turnover Limits: As of April 1, 2019, the threshold for eligibility under the Composition Scheme has been increased to Rs. 1.5 crore. This adjustment allows more businesses to opt for the scheme, enabling them to pay taxes on a quarterly basis and file returns annually. In contrast, the threshold for businesses in the North Eastern states and Uttarakhand remains at Rs. 75 lakh. This same enhanced threshold applies to restaurants that do not serve alcoholic beverages. Extension to Service Providers- Previously limited primarily to traders and manufacturers, the Composition Scheme has now been expanded to include service providers.

- This includes independent service providers and those who supply both goods and services with an annual turnover of up to Rs. 50 lakh in the previous financial year.

- Eligible service providers under this scheme are required to pay a fixed tax rate of 6%, divided equally between CGST and SGST at 3% each.

How to Determine if Your Business Meets the GST Threshold?

To determine if your business meets the GST registration threshold, you need to calculate your aggregate turnover. This calculation should include:- Revenue from Sales and Services: This encompasses all income derived from the sale of goods and provision of services domestically.

- Export Earnings: Includes all revenue from goods sold or services provided to international clients.

- Interstate Supplies: Accounts for all transactions that involve the transfer of goods or services across state boundaries.

Circumstances Requiring Mandatory GST Registration

There are specific situations where GST registration is compulsory, regardless of whether your business turnover falls below the exemption limit. These include:- E-commerce Operators: Any business that operates through an e-commerce platform must register for GST, irrespective of turnover.

- Inter-state Supply: Businesses involved in the supply of goods or services across state lines are required to register for GST, regardless of their annual revenue.

Consequences of Non-Compliance with GST Registration Requirements

Failing to register for GST after surpassing the threshold limit can have severe repercussions for a business, including:- Heavy Penalties

- Legal Actions

- Damage to Business Reputation

Benefits of GST Compliance

Being compliant with the GST regulations by understanding and adhering to the updated threshold limits offers several advantages for businesses:- Claim Input Tax Credits: GST compliance enables businesses to claim input tax credits, which means they can deduct the amount of GST paid on purchases from their tax liability on sales. This can significantly reduce overall tax expenses.

- Legal Recognition: Registering for GST provides legal recognition as a registered supplier, allowing businesses to operate legally across states and with various businesses.

- Enhanced Market Credibility: Compliance enhances a business’s credibility in the market, which can improve relationships with vendors and customers who may prefer or require dealing with GST-registered entities.