Renu Suresh

Expert

Published on: Jul 30, 2026

Tmb Msme Credit Scheme

The Tamil Nadu Mercantile Bank Limited has launched Tmb Msme Credit Scheme. The primary objective towards the execution of this scheme is to provide Bank Credit to Micro Small and Medium Enterprise (MSME) at liberalised terms towards working capital and term loan for acquiring fixed assets. In this article, we will look at the Tmb Msme Credit Scheme in detail.Eligibility Criteria

All MSME units run by Individuals or HUFs, Proprietary concerns, Partnership Firm and Limited Companies are eligible for Tmb Msme Credit Scheme.Classification of MSME under MSME Credit Scheme

Micro (Manufacturing) Enterprises (Priority Sector)

Enterprises engaged in the manufacture or production or preservation of goods and whose investment in plants and machinery original cost excluding the property does not exceed Rs.25 lakhs, irrespective of the location of the unit.Small (Manufacturing) Enterprises (Priority Sector)

Enterprises engaged in the manufacture or production or preservation of goods and whose investment in the plant and machinery original cost excluding the land and building does not exceed Rs.5 crore.Micro (Service) Enterprises (Priority Sector)

Enterprises engaged in the rendering of services and whose investment in equipment original cost excluding property, furniture and fittings do not exceed Rs.10 lakh.Small (Service) Enterprises (Priority Sector)

Enterprises engaged in the rendering of services and whose investment in equipment (original cost excluding the land and building, fittings, furniture and other not directly related to the services rendered does not exceed Rs.2 crore. The Small and Micro (Service) Enterprises will also include the following enterprises:- Small Road & Water Transport Operators

- Small Business

- Professional & Self-Employed Persons

- Service Enterprises

Medium (Manufacturing) Enterprises ( Non – Priority Sector)

Enterprises engaged in the manufacture or preservation of goods and whose investment in the plant and machinery cost excluding property is more than Rs.5 crore but does not exceed Rs.10 crore.Medium (service) Enterprises( Non – Priority Sector)

Enterprises are providing services and whose investment in equipment original cost excluding the land and building and furniture, fittings are more than Rs.2 crore but do not exceed Rs.5 crore.Form of Advance

All type of fund based and Non-fund based limits to provide bank credit to Micro, Small & Medium Enterprises (MSME) at concessional rate of interest towards the working capital and term loan for acquiring any fixed assets for business development. Purchase of second-hand indigenous machinery and imported used machinery are allowed under the Tmb Msme Credit Scheme. All Sanctioning Authorities including the Branch Managers are authorised to sanction loans for purchase of second-hand indigenous machinery and imported used machinery under the Tmb Msme Credit Scheme.Maximum Amount of Loan

The maximum amount of loan under the Tmb Msme Credit Scheme is given here:- Single Borrower: Rs.25 Crore

- Group Borrowers: Rs.50 Crore

Assessment of Working Capital Limits

For Micro and Small Enterprises:

The Working Capital requirement is assessed upto Rs.5 crore in the case of Manufacturing Enterprises and upto Rs.2 croreFor Service Enterprises:

Projected Turnover Method of Assessment based on the minimum working capital limit at 20% of estimated annual turnover will be followed.All other cases

Projected balance Sheets method (Maximum Eligible Bank Finance) is providing for NWC at 25% of current assets will be followed. In the case of Service Enterprises like Contractors, the Cash Budget Method of Assessment should be followed.Conditions:

The borrowing unit should provide five per cent of the projected annual turnover as margin money. Increase in the projected turnover should typically not to exceed 25% of the actual turnover in the preceding years. A prudent decision in this regard it will be taken based on the capacity expansion, increased capacity utilisation and pricing of Inventory. In all such cases if the projected turnover is accepted for assessment is more than 25% of the previous years’ actuals, hard copies of the Sanction Appraisal Notes need to be sent to RO for scrutiny along with the MDP statement. The RO should look into the justification and advise comments if any to the branch.Term Loans

The quantum of the term loans will be based on the project cost and cost of machinery less margin as per the Loan Policy. The same will be linked to the repayment capacity of the borrower assessing the cash flows and ADSCR.Primary Security

- Working Capital Limits: Stock and Receivables

- Term Loan: Assets acquired and created out of Loan

Margin

The margin for the As per the Tamil Nadu Mercantile Bank Limited NormsCollateral Security

- Collateral security should not be obtained for Tmb Msme Credit Scheme loans upto 10.00 lakh extended to Micro and Small Enterprises (MSE) for both manufacturing and service enterprises.

- Collateral security should not be obtained for MSME loans upto Rs.100 lakhs under the Credit Guarantee Fund Trust for Micro and Small Enterprises scheme.

- Advances to Retail Trade, Educational Institutions, Training Centres and Self Help Groups cannot be covered under CGS)

- lIn respect of advances covered under the CGTMSE Scheme, the third-party guarantee should not be taken in any form

- Collateral securities need not be insisted for Key Loans, IBN and FBN facilities.

- Marketable and Tangible collateral security of at least 50% of the limit sanctioned should be acquired for Fund Based and Non-fund based limits sanctioned to the Medium Enterprises. The loans upto Rs.100 lakh, which are covered under CGS of CGTMSE are exempt from this requirement.

- Marketable and Tangible collateral security of at least 50% of the limit sanctioned should be obtained for the Fund Based and Non-fund based limits aggregating to above Rs.10 lakh sanctioned to Micro & Small Enterprises. The loans upto Rs.100 lakh, which are covered under CGS of CGTMSE are exempt from this requirement.

CGS Cover under CGSTMSE

Guarantee cover available under CGS scheme is given below:|

Sl.No |

Enterprises |

Guarantee cover |

| 1 | Upto Rs. 5.00 | 85% of the amount in default subject to a maximum of Rs.4.25 lakh |

| Above Rs.5 lakhs and upto Rs.50 lakhs | 75% of the amount in default and subject to a maximum of Rs.37.50 lakhs | |

|

2 |

Women Entrepreneurs/units located in the North East Region Other than Credit facility upto Rs.5 lakh to Micro Enterprises | 80% of the amount in default subject to a maximum of Rs.40 lakh |

|

3 |

All other categories of borrowers Upto Rs.50 lakh | 75% of the amount in default and subject to a maximum of Rs.37.50 lakh |

|

4 |

All limits above Rs.50 lakh and Upto Rs.100 lakh | 50% of the amount in default and subject to overall ceiling of Rs.50 lakh |

Rate of Interest (For Domestic Credit)

Interest Rates on Tmb Msme Credit Scheme is given in the document :Penal Interest

- Any irregularity in repayment will attract the penal interest of 2% per annum over and above the applicable rate of interests for the advance above Rs.25000.

- The existing instruction of no penal interests for credit scheme loans under priority sector up to Rs.25000 remain unchanged.

Working Capital

The working capital for Tmb Msme Credit Scheme is one yearTerm Loan

Maximum seven years excluding Holiday period (repayment holiday should not more than 12 months except in respect of the construction of civil structures, where it will go upto 18 months) BankGuarantees Details

The maximum period of BGs to be granted under sanctioned limits in force will be three years including the claim period. For Guarantee to be issued beyond three years, specific permission of the Regional Head should be obtained.Tmb Msme Credit Scheme Application Procedure

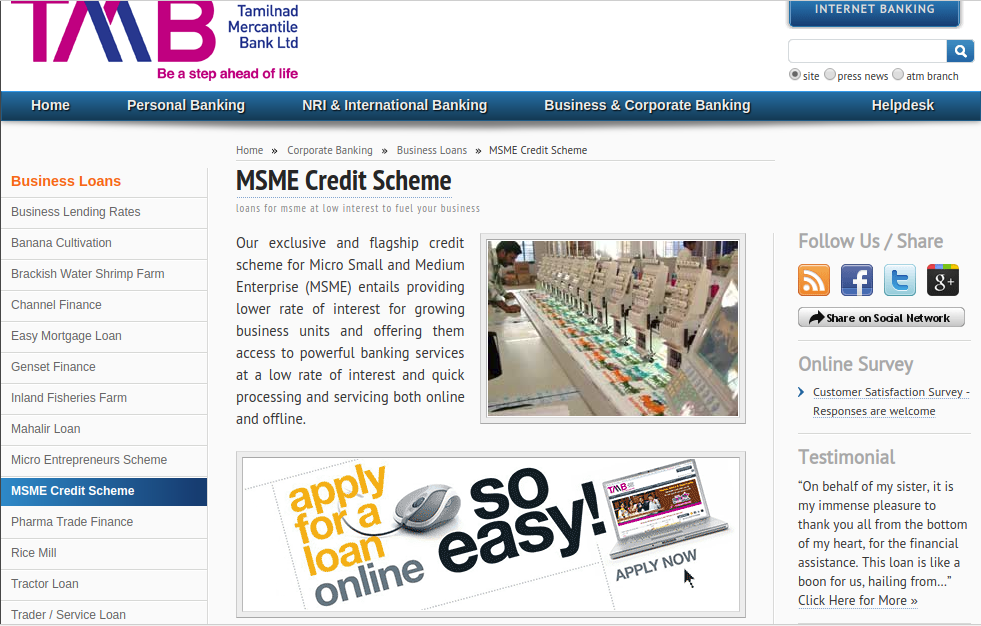

The application procedure to complete the Tmb Msme Credit Scheme is explained in detail below: Access the official webpage of Tamil Nadu Mercantile Bank Limited. From the menu bar, click on Business & Corporate Banking. Image 1 Tmb Msme Credit Scheme

From the list of Commercial Loan, select MSME Credit Scheme. The page will redirect to the new page.

Image 1 Tmb Msme Credit Scheme

From the list of Commercial Loan, select MSME Credit Scheme. The page will redirect to the new page.

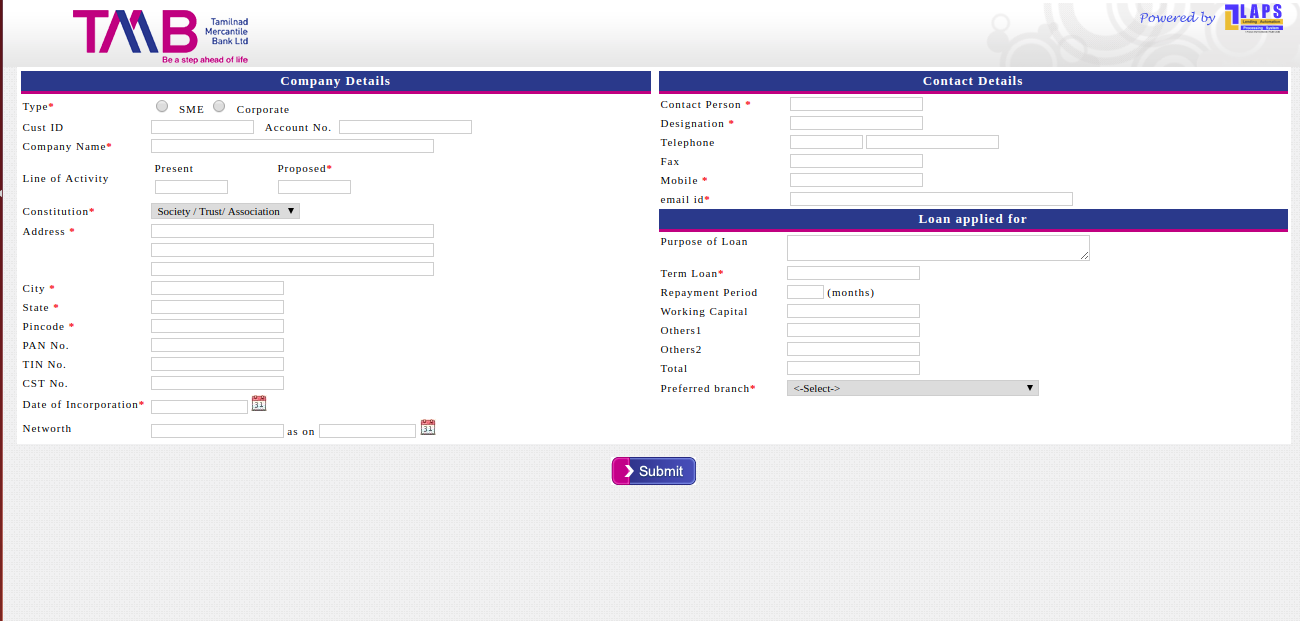

Image 2 Tmb Msme Credit Scheme

Click on the apply now an option; the link will redirect to the new page. The application form will be displayed. Provide the following details to complete the application form.

Image 2 Tmb Msme Credit Scheme

Click on the apply now an option; the link will redirect to the new page. The application form will be displayed. Provide the following details to complete the application form.

- Company Details

- Contact Details

- Loan Details

Image 3 Tmb Msme Credit Scheme

By clicking on the submit button, the application form will be forwarded to the respective TAB branch. After verification, the loan amount will be issued.

Image 3 Tmb Msme Credit Scheme

By clicking on the submit button, the application form will be forwarded to the respective TAB branch. After verification, the loan amount will be issued.