Jeyaraj Allwyn

Expert

Published on: Apr 21, 2026

Micro Financing Schemes Of NBCFDC

"The poor stay poor not because they are lazy but because they have no access to capital."

- Milton Friedman

This article deals about the Micro Financing schemes under the aegis of

National Backward Classes Finance & Development Corporation (NBCFDC). We will have a detailed look into salient features, eligibility criteria, and the pattern of finance of the micro-financing schemes under NBCFDC.Micro Financing

Microfinance recognises poor people as remarkable reservoirs of energy and knowledge and bring in people with limited income and give them the tools to help themselves. Microfinance is provided to the underprivileged people with the belief that giving a dole (charity, philanthropy, freebies, etc.) is not the solution to poverty.

National Backward Classes Finance & Development Corporation (NBCFDC)

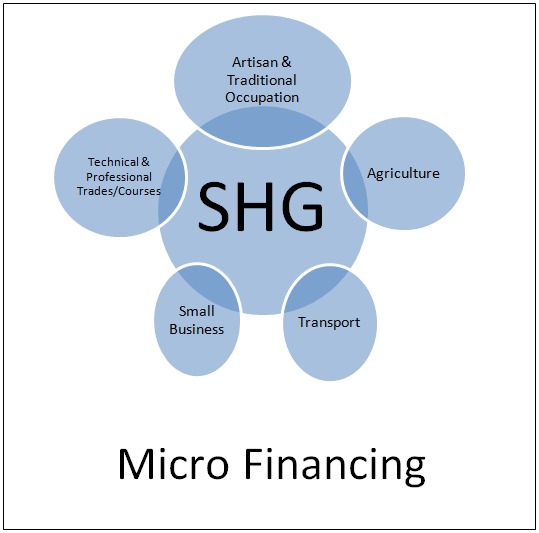

The National Backward Classes Finance & Development Corporation (NBCFDC), which is under the aegis of Ministry of Social Justice and Empowerment, works for promoting economic and developmental activities for the benefit of Backward Classes and assisting the weaker section of these classes in skill development and self-employment forays. They provide financial assistance through State Channelising Agencies (SCAs). NBCFDC also provides Micro Financing through SCAs/ Self Help Groups (SHGs). NBCFDC supports the weaker section of these classes in skill development and self-employment ventures under the following broad sectors:

- Agriculture and Allied Activities.

- Small Business.

- Artisan and Traditional Occupation.

- Technical and Professional Trades/Courses.

- Transport and Service Sector.

Financing Schemes of NBCFDC

Micro Finance Mahila Samriddhi Yojana Small Loan Scheme

Objectives

Micro Finance - To cater to the Micro Finance needs of small entrepreneurs belonging to the target group, through nominated Channelising Agencies. Mahila Samriddhi Yojana - Provide Micro Finance to women entrepreneurs who belong to the target group. Small Loan Scheme - Provide Micro Finance for any individual for starting a small business. Note: For all the above schemes there is a Maximum loan limit of Rs.60,000/- per beneficiary. The maximum number of women in an SHG is also limited to 20.Comparison of Schemes

|

MICROFINANCE |

MAHILA SAMRIDDHI YOJANA |

SMALL LOAN SCHEME |

|

| Implementation | Implemented through SCAs in rural and urban areas by way of financing the recipients either directly or through SHGs preferably in the areas untouched so far under any such scheme. | Implemented by the Channel Partners in rural and urban areas by way of financing the recipients either directly or through SHGs preferably in the areas untouched so far under any such scheme. | Implemented through State Channelising Agencies (SCAs)/Banks. |

| Eligibility of the Beneficiary | Members of Backward Classes who are living below double the poverty line (below Rs.3.00 Lakh) The SCAs/Banks are requested to release at least 50% of total funding to persons with annual family income up to Rs.1.50 Lakh. In an SHG 75% of members can be from Backward Classes and remaining 25% members may be from other weaker section like SC / Handicapped etc. | Women belonging to the Backward Classes and living below double the poverty line. Annual family income of the women is less than Rs.3.00 Lakh. The SCAs/Banks are requested to release at least 50% of total funding to persons with family income up to Rs.1.50 Lakh per annum. | An applicant who belongs to the Backward Classes and living below double the poverty line. Applicant's annual family income should be less than Rs.3.00 Lakh. The SCAs/Banks are required to release at least 50% of total released funds to the persons having an annual family income less than Rs.1.50 Lakh. |

| Pattern of Finance | 1. NBCFDC loan : 90% 2. SCA/Bank Loan: 05% 3. Beneficiary contribution: 05% | 1. NBCFDC loan : 95% 2. SCA/Beneficiary contribution: 05% | 1. NBCFDC loan : 85% 2. SCA/Bank Loan: 10% 3. Beneficiary contribution: 05% |

| Utilization Period | Four months from the date of disbursement | Four months from the date of disbursement | NA |

| Rate of Interest | 1. From NBCFDC to SCA : 2% p.a. 2. SCA to SHG 5% p.a. | 1. From NBCFDC to SCA : 1% p.a. 2. SCA to Beneficiary : 4% p.a. | 1. From NBCFDC to Channel Partner : 3% p.a. 2. SCA/Bank to Beneficiary : 6% p.a. |

| Repayment | A loan is to be repaid in quarterly instalments within 48 months | A loan is to be repaid in quarterly instalments within 48 months | Ten years |