RENU SURESH

Expert

Published on: Jun 24, 2026

GSTR-9 Annual Return: Due Date, Applicability, Turnover Limit, Format, Documents Required & How to File

Filing GSTR-9 is an essential annual obligation for all individuals and businesses registered under the GST system. GSTR-9 comprises comprehensive details of outward and inward supplies, encompassing transactions conducted or received throughout the fiscal year. The return consolidates all the monthly or quarterly returns filed during the respective year into a single, unified record. This article will provide a comprehensive guide on GSTR-9, including its definition, eligibility, due dates, turnover limits, types, format, filing steps, consequences of non-filing, and a detailed step-by-step procedure for the financial year 2024-2025.

Time is running out! File your GSTR-9 before December 31st with IndiaFilings' expert guidance - Act now to avoid penalties!

GSTR-9 & GSTR-9C for FY 2024-25 Now Live on the GST Portal

What is the GSTR-9 Annual Return?

GSTR-9 is an annual return that must be filed every year by taxpayers registered under GST. Key points include:

- It contains details of all outward and inward supplies made or received during the financial year under various tax heads—CGST, SGST, IGST—along with cess and HSN codes.

- It serves as a consolidated summary of all monthly or quarterly returns (GSTR-1, GSTR-2A, GSTR-2B, and GSTR-3B) filed during the year. While it can be complex, GSTR-9 ensures thorough reconciliation of data and promotes complete transparency in reporting.

Law Governs GSTR-9

The regulations about GSTR-9 are overseen by Section 44 of the Central Goods and Services Tax (CGST) Rules, 2017, in conjunction with Rule 80 of the CGST Rules, 2017.

GSTR-9 Applicability: Who Should File the Annual Return?

All GST-registered taxpayers are required to file GSTR-9. However, the following categories are exempt from filing GSTR-9:

- Taxpayers under the composition scheme (they must file GSTR-9A)

- Casual taxable persons

- Input service distributors

- Non-resident taxable persons

- Persons paying TDS under Section 51 of the CGST Act

- Persons collecting TCS under Section 52 of the CGST Act

GSTR-9 Types

Under CGST Rule 80, the provisions for annual return forms are classified into four types:

- GSTR-9: Filed by regular GST taxpayers who submit GSTR-1 and GSTR-3B, especially if their annual turnover exceeds ₹2 crore during the financial year.

- GSTR-9A: Previously filed by composition scheme taxpayers until FY 2018-19. From FY 2019-20 onwards, it has been replaced by GSTR-4, due by 30th April of the following year.

- GSTR-9B: Applicable to e-commerce operators collecting TCS and filing GSTR-8 monthly. Currently, the filing of this return is on hold.

- GSTR-9C: The Annual Reconciliation Statement, which must be self-certified and filed by taxpayers whose aggregate turnover exceeds ₹5 crore in a financial year.

What is the GSTR-9 Turnover Limit?

GSTR-9 (Annual Return) is optional for businesses with an annual turnover of up to ₹2 crore from FY 2017-18 to FY 2023-24. Each year, the GST department notifies the threshold turnover limit, above which filing GSTR-9 becomes mandatory.

GSTR-9 Due Date

For FY 2024-25, the last date to file GSTR-9 is 31st December 2025. Generally, the GSTR-9 due date is the 31st of December of the following financial year for which the annual return is being filed.

Click here to know more about the GSTR 9 Due Date

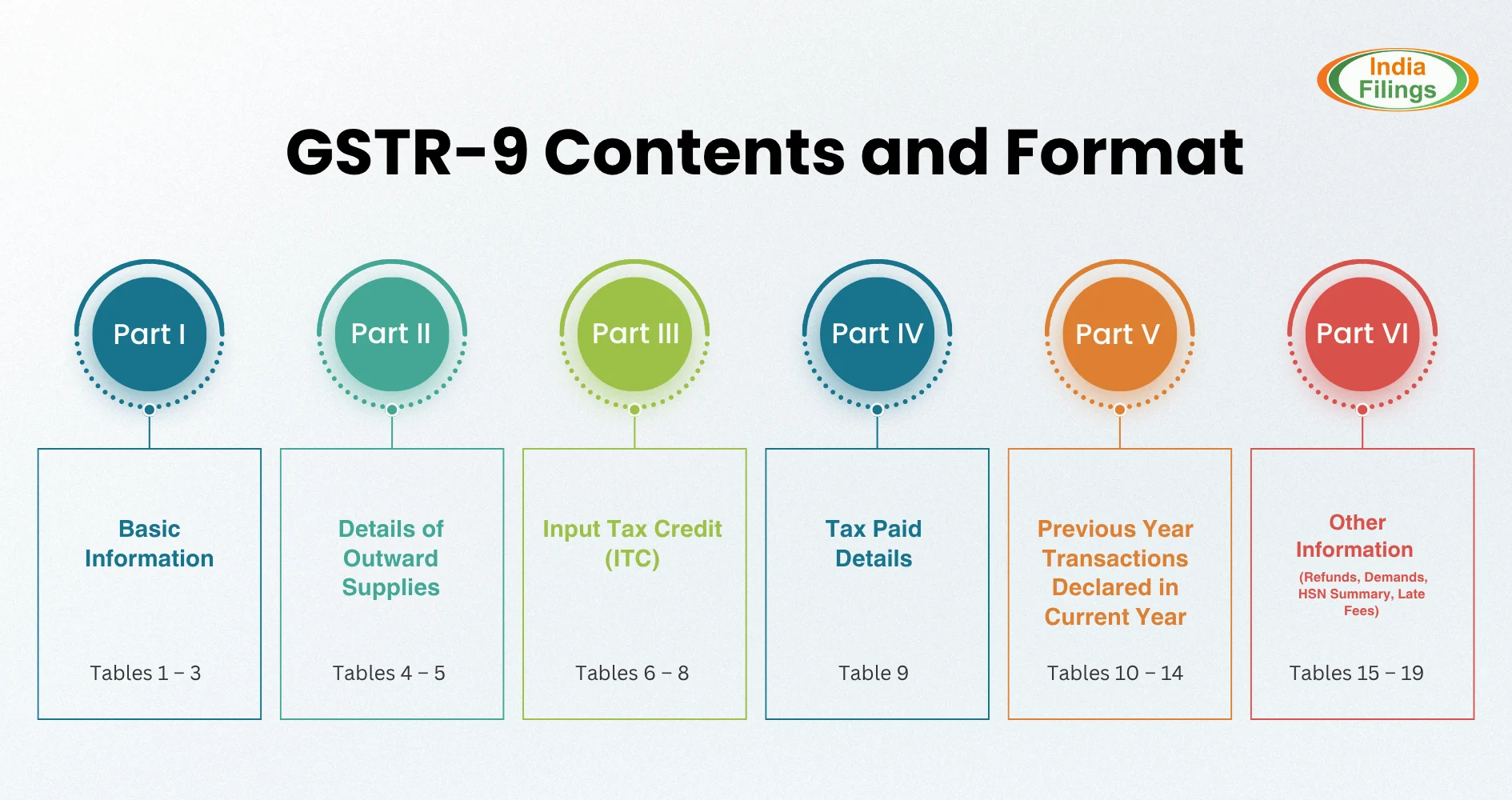

GSTR-9 Contents and Format

The GSTR-9 form is divided into 6 main parts and 19 sections, with each part requiring information that can largely be obtained from previously filed returns and accounting records.

- Outward Supplies: Annual sales, separated into taxable and non-taxable categories.

- Inward Supplies & ITC: Total purchases and input tax credit availed, including classification as inputs, input services, and capital goods.

- Reversals: ITC that is ineligible for claim must also be reported.

PART 1 – Basic Details

Includes auto-populated information from GST records:

- GSTIN

- Financial Year

- Legal Name

- Trade Name

PART 2 – Details Related to Outward Supplies

Requires comprehensive information about outward supplies:

- Supply to registered and unregistered persons

- Exports and supplies to SEZs with tax payment

- Taxes paid on advances

- Inward supplies liable to reverse charge

- Credit and debit notes, including amendments

- Nil-rated, exempted, and non-GST supplies

- Zero-rated supplies

- Credit/debit notes on nil-rated, exempted, and non-GST supplies

PART 3 – Details of Input Tax Credit (ITC)

Covers the total ITC claimed during the year:

- ITC bifurcation: inputs, input services, and capital goods

- ITC under reverse charge mechanism (from registered and unregistered persons)

- ITC on import of goods/services

- Reversal of ITC as per various rules

- Reconciliation of ITC between GSTR-3B and GSTR-2B

PART 4 – Details of Tax Payable

Shows details of tax liability set off against ITC as per GSTR-3B.

- The Tax Payable column is editable, allowing taxpayers to increase liability and pay through DRC-03.

PART 5 – Adjustments Made in Subsequent Financial Year

- Adjustments related to the current financial year made in the following year within the timeline of Section 16(4)

- Includes adjustments for both input and output supplies

PART 6 – Refunds Claimed and Demands Raised (Optional for FY 2023-24)

- Details of refunds claimed during the financial year

- Details of any demands raised

PART 7 – HSN/SAC Code-wise Summary and Late Fees

- Summary of inward and outward supplies by HSN/SAC codes

- Must be reconciled with actual outward and inward supplies

Late Fee and Penalty for Not Filing GSTR-9

The GST department imposes late fees for delayed filing of GSTR-9 based on the taxpayer’s turnover, effective from FY 2022-23:

S.No | Turnover Limit | Late Fee per Day | Maximum Late Fee |

1 | Up to ₹5 crore | ₹50 (₹25 each under CGST & SGST) | 0.04% of turnover in state/UT (0.02% each under CGST & SGST) |

2 | More than ₹5 crore and up to ₹20 crore | ₹100 (₹50 each under CGST & SGST) | 0.04% of turnover in state/UT (0.02% each under CGST & SGST) |

3 | More than ₹20 crore | ₹200 (₹100 each under CGST & SGST) | 0.50% of turnover in state/UT (0.25% each under CGST & SGST) |

Previous Financial Years (up to FY 2021-22):

- Late fee was ₹100 per day under CGST and ₹100 per day under SGST, totaling ₹200 per day.

- Maximum liability was 0.25% of turnover per Act.

- No late fee was levied on IGST.

GST Amnesty Scheme for GSTR-9 (2023)

The CBIC introduced a scheme in 2023 offering partial waiver of late fees for delayed filing of GSTR-9 for previous financial years, encouraging taxpayers to comply without facing heavy penalties.

Click here to know more about the GST Amnesty Scheme

Documents Required for GSTR-9

To file Form GSTR-9, you'll typically need:

- Monthly GST Returns (GSTR-1, GSTR-2A, GSTR-3B): These show your monthly sales, purchases, and tax calculations.

- Annual Financial Statements: Your yearly profit and loss statement and balance sheet.

- Reconciliation Statement (GSTR-9C): This helps match your financial data with your GST returns.

Prerequisites for filing the annual return (GSTR-9)

The prerequisites for filing the annual return (GSTR-9) are as follows:

- Taxpayer Registration: The taxpayer must be registered as normal under the Goods and Services Tax (GST) for at least one day during the financial year in question.

- Filing of GSTR-1 and GSTR-3B: Before filing the annual return (GSTR-9), the taxpayer must have filed GSTR-1 and GSTR-3B for the entire financial year. This is because GSTR-9 compiles data from these two returns.

- Auto-Filled Tables: Some tables in GSTR-9 are auto-filled with data based on the information provided in GSTR-3B and GSTR-2A:

- Table 6A is auto-filled with information from GSTR-3B and is not editable.

- Table 8A is auto-filled based on details from GSTR-2A and is also not editable.

- Table 9, which contains details of tax paid as declared in returns filed during the financial year, will be auto-filled based on the information provided by the taxpayer in Form GSTR 3B for the relevant fiscal year.

These prerequisites ensure that the annual return (GSTR-9) accurately reflects the taxpayer's GST-related transactions and tax payments for the financial year.

GSTR-9 Filing Steps

The process to file GSTR-9 for a financial year (e.g., FY 2024-25) can be summarized as follows:

- Complete GSTR-1 and GSTR-3B filings up to date for the financial year.

- Perform reconciliation of Input Tax Credit (ITC) and sales from the beginning of the financial year.

- Communicate with vendors and customers to resolve any discrepancies identified during reconciliation.

- Disclose FY 24-25 details in the government’s offline tool or via cloud-based software (e.g., Clear) for easier auto-fills and end-to-end filing.

- Pay any shortfall of tax or adjust excess ITC claims for FY 24-25 through DRC-03.

- File GSTR-9 on the GST portal.

For detailed, step-by-step instructions on portal filing, refer to the page ‘Step-by-step guide to file GSTR-9’.

Latest Update

7th June 2025

The GSTN issued an advisory restricting taxpayers from filing GSTR-3B after the expiry of three years from its due date. This change will be implemented on the GST portal starting July 2025 tax period.

55th GST Council Meeting (21st December 2024)

The Council will issue a circular clarifying the late fee applicable under Section 47(2) of the CGST Act, 2017 for delays in filing:

- GSTR-9 (annual return)

- GSTR-9C (reconciliation statement) The clarification will be effective through the relevant circulars/notifications.

53rd GST Council Meeting (22nd June 2024)

The Council recommended a relaxation from filing GSTR-9/9A for FY 2023-24 for taxpayers whose aggregate turnover is below ₹2 crore. This was notified via CGST Notification 14/2024 dated 10th July 2024.

Why Choose IndiaFilings for Filing GST Annual Return?

- Expert Assistance: Professional guidance from GST experts ensures accurate filing.

- Time-Saving: Streamlined process reduces the complexity and time involved in preparing GSTR-9.

- Error-Free Filing: Automated checks and reconciliations minimize mistakes.

- End-to-End Support: From ITC reconciliation to payment of dues and filing, the entire process is handled.

- Compliance Guarantee: Helps you stay fully compliant with GST regulations and avoid penalties.

- Cloud-Based Convenience: File returns online anytime with easy access to all past records.

Using IndiaFilings simplifies the GSTR-9 filing process, making it fast, reliable, and hassle-free.

Related Articles on GSTR Filing

- GSTR-1 Filing

- GSTR-2 Filing

- GSTR-3 Filing

- GSTR-3B Filing

- GSTR-4 Filing

- GSTR-5 Filing

- GSTR-5A Filing

- GSTR-6 Filing

- GSTR-7 Filing

- GSTR-8 Filing

- GSTR-10 Filing

- GSTR-11 Filing