RENU SURESH

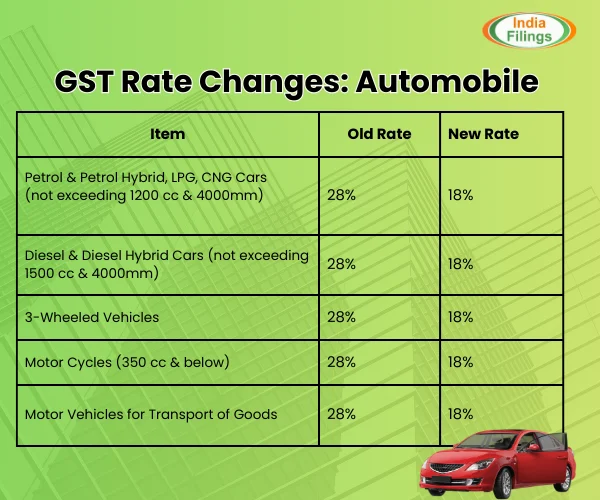

Expert

Published on: Jul 30, 2026

Next Generation Gst Reforms: New GST Rates, Slabs, and Key Changes

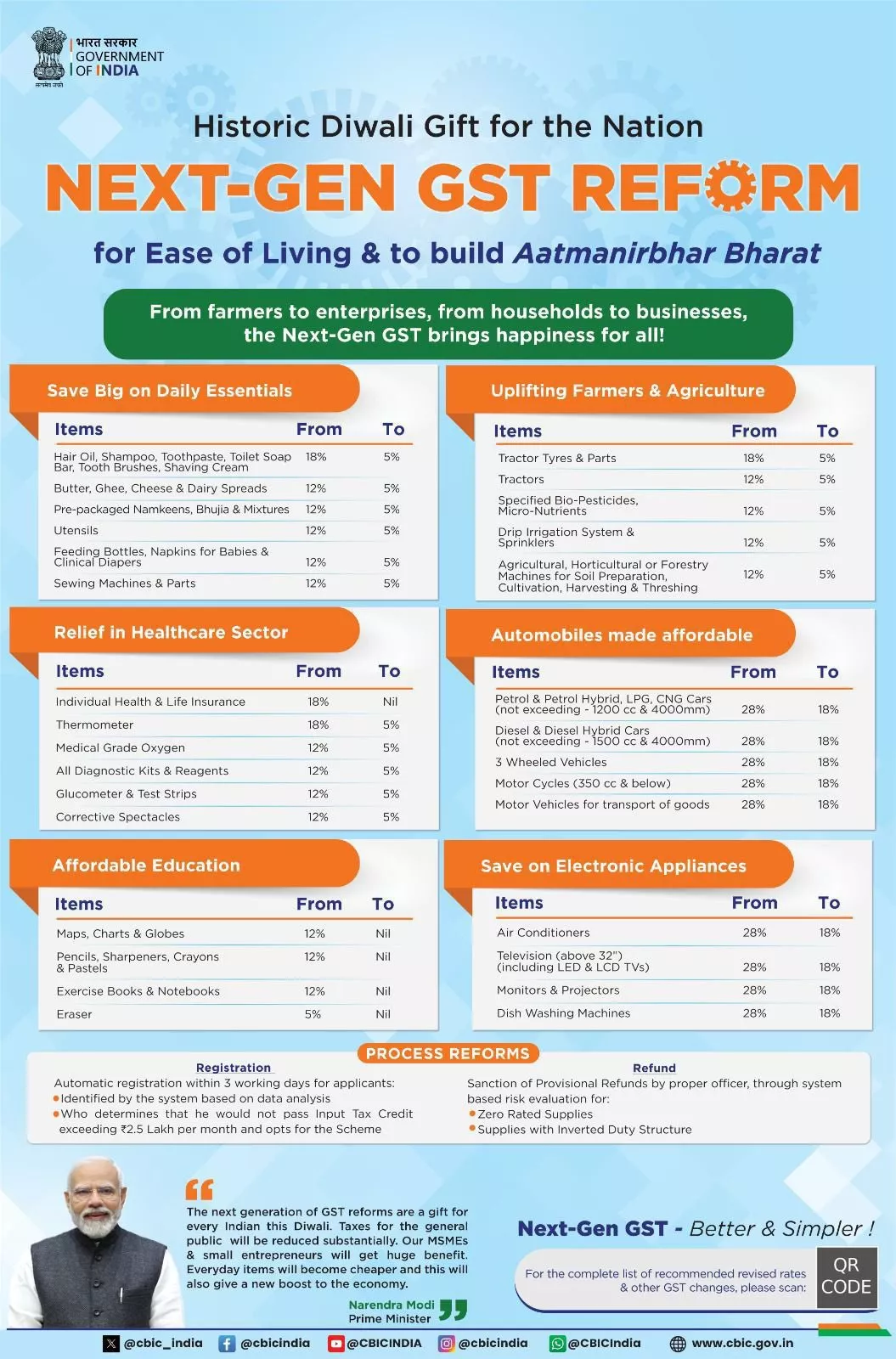

On 3rd September 2025, Union Finance Minister Nirmala Sitharaman announced major changes to India’s Goods and Services Tax (GST) at the 56th GST Council meeting. Dubbed the “Next-Gen GST Reforms”, these reforms aim to simplify the tax system, reduce the burden on citizens, and boost economic activity.

Next Generation Gst Reforms

The Next Generation Gst Reforms refer to a major overhaul of India’s Goods and Services Tax system, aimed at making it simpler, more transparent, and citizen-centric. Announced by Prime Minister Narendra Modi on 15th August 2025, these reforms focus on:

- Simplifying the GST Rate Structure: Reducing the multi-tier system into three main rates:

- Reducing Tax Burden on Citizens: Lower GST rates on daily essentials, healthcare, education, agriculture, and certain services to make them more affordable.

- Correcting Inverted Duty Structures: Addressing anomalies in sectors like textiles, footwear, fertilizers, and packaging to ensure fair taxation.

- Encouraging Ease of Doing Business: Streamlining registration, returns, refunds, and dispute resolution through GSTAT and automated systems.

- Promoting Economic Growth: Supporting farmers, MSMEs, and domestic production through rationalized rates and targeted exemptions.

In short, these reforms aim to simplify taxation, provide relief to the common man, strengthen compliance, and boost economic activity across sectors.

Implementation of New GST Rate

Following the recommendations of the GST Council at its 56th meeting, revised GST rates on goods and services - excluding cigarettes, chewing tobacco products such as zarda, unmanufactured tobacco, and beedis—will come into effect from 22nd September 2025.

GST Rate Rationalisation

New Simplified Rate Structure:

- Standard Rate: 18%

- Merit/Essential Rate: 5%

- De-merit / Select Goods & Services: 40%

The 12% and 28% GST slabs have been merged into the 18% standard rate

Changes in GST Rates of Goods

The 56th GST Council meeting has implemented major changes to GST rates on goods, aiming to simplify the tax structure, reduce the burden on essential items, and align similar products under uniform rates.

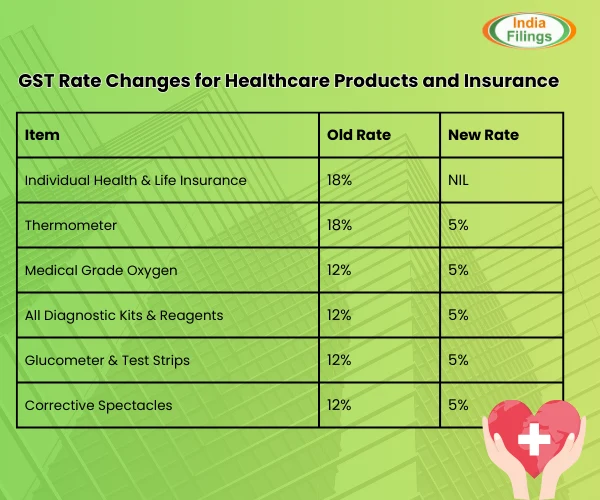

Exemptions on Life and Health Insurance

- All individual life insurance policies (term life, ULIPs, endowment) – fully GST exempt

- All individual health insurance policies (including family floater and senior citizen plans) – fully GST exempt

GST Rate on Medicines

All drugs and medicines are levied a concessional GST rate of 5%, except for certain items that are exempt and charged at a nil rate.

GST on Medical Devices

A GST rate of 5% applies to all medical devices, instruments, and apparatus used for medical, surgical, dental, and veterinary purposes, except for items that are specifically exempted.

GST on Small Cars

The GST rate on all small cars has been reduced from 28% to 18%. Under GST, “small cars” are defined as:

- Petrol, LPG, or CNG cars with an engine capacity up to 1,200 cc and a length up to 4,000 mm.

- Diesel cars with an engine capacity up to 1,500 cc and a length up to 4,000 mm.

GST on ‘Other Non-Alcoholic Beverages’

As part of the recent GST rate rationalisation, similar goods have been aligned under the same tax rate to prevent misclassification and disputes. This principle has been applied to ‘other non-alcoholic beverages,’ which are now taxed at 40%.

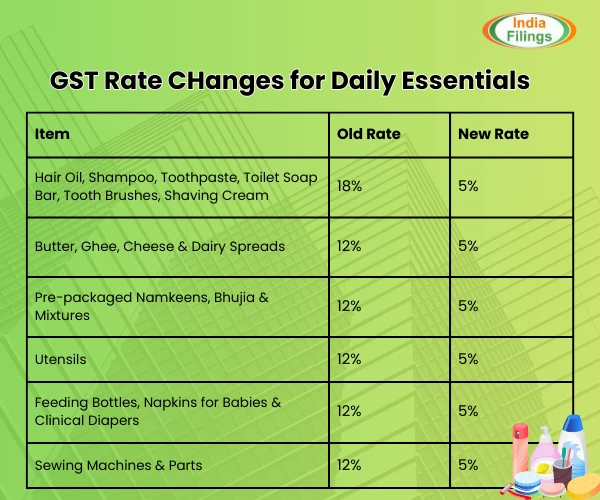

GST Rate on Daily Essentials

The 56th GST Council meeting announced significant relief on daily-use items by reducing their GST rates to 5%. Products such as shampoo, hair oil, toothpaste, soaps, dairy items like butter and ghee, pre-packaged namkeens, feeding bottles, and even baby care products have become more affordable.

GST on Indian Breads

Earlier, bread was already exempt from GST, while products such as pizza bread, roti, porotta, and paratha were subject to varying tax rates. Under the recent reforms, all Indian breads regardless of name, are now fully exempt from GST. The examples provided are illustrative, not exhaustive, ensuring broad coverage under the exemption.

GST on Carbonated Beverages and Fruit Drinks

The GST rate on carbonated beverages and fruit drinks has been increased to maintain the pre-rationalisation tax level. Previously, these items were subject to both GST and compensation cess. With the decision to remove the compensation cess, the GST rate has been adjusted accordingly.

GST Treatment of Paneer vs. Other Cheeses

Paneer sold in non-pre-packaged and unlabelled form already attracted a nil GST rate. The recent changes now apply only to pre-packaged and labelled paneer. As an Indian cottage cheese largely produced in the small-scale sector, this measure is intended to support and promote domestic production of paneer.

GST on Vehicles Exceeding 1500 cc or 4000 mm

The GST rate on all mid-size and large cars—vehicles with engine capacity above 1,500 cc or length exceeding 4,000 mm—is set at 40%. This rate also applies to Utility Vehicles (UVs), including Sports Utility Vehicles (SUVs), Multi-Utility Vehicles (MUVs), Multi-Purpose Vehicles (MPVs), or Crossover Utility Vehicles (XUVs) with engine capacity over 1,500 cc, length above 4,000 mm, and ground clearance of 170 mm or more, without any additional cess.

GST on Motorcycles

- Motorcycles up to 350 cc: 18% GST

- Motorcycles above 350 cc: 40% GST

GST on Air Conditioners, TVs, Monitors, and Dishwashers

- Air conditioners and dishwashers: Reduced from 28% to 18% GST

- TVs and monitors: All sizes now uniformly taxed at 18% GST (earlier, up to 32 inches at 18%, larger sizes at 28%)

GST on Batteries (Heading 8507)

All batteries under heading 8507, including lithium-ion and other types, will now be uniformly taxed at 18% GST (earlier lithium-ion at 18% and others at 28%).

GST on Passenger Air Transport

The two-rate option is not available for air travel. GST is charged at 5% for economy class and 18% for other classes.

GST on Beauty and Physical Well-Being Services

Services such as health clubs, salons, barbers, fitness centres, and yoga will attract a GST rate of 5% without ITC, down from the previous 18%.

GST on UHT and Plant-Based Milk

UHT (Ultra High Temperature) milk has been exempted from GST, aligning it with other dairy milk products. Plant-based milk drinks, previously taxed at 18% (except soya milk drinks at 12%), will now be taxed uniformly at 5%.

Other Changes Relating to Goods

- GST on Pan Masala, Gutkha, Cigarettes, Unmanufactured Tobacco, Chewing Tobacco like Zarda will be levied on Retail Sale Price (RSP) instead of transaction value.

- Ad hoc IGST and compensation cess exemption granted on the new armoured sedan imported for the President of India.

Changes in GST Rates of Services

The GST Council has revised service tax rates to simplify compliance and provide relief to consumers.

- Beauty & Physical Well-Being Services (salons, gyms, barbers, yoga) – 5% GST without ITC (previously 18%)

- Passenger Air Transport – economy class 5%, other classes 18%

Other Changes Relating to Services

Clarifications added to “specified premises” for restaurant services; stand-alone restaurants cannot declare themselves as such to avail 18% GST with ITC.

- Valuation rules aligned with changes in lottery ticket taxation.

- Remaining items will continue at existing rates until compensation cess obligations are cleared.

- Union Finance Minister may decide the transition date for these items.

Measures for Facilitation of Trade

The GST Council has introduced several process and procedural reforms to simplify compliance, reduce administrative burdens, and enhance ease of doing business.

E-Way Bills for Goods in Transit

According to Rule 138 of the CGST Rules, 2017, an e-way bill must be generated before the commencement of the supply or transport of goods. There is no mandatory requirement to cancel and reissue e-way bills for goods already in transit when new GST rates come into effect. Existing e-way bills will remain valid for their original validity period.

Process Reforms

- Pre-filled GST returns and automated refund mechanisms will be implemented (dates to be notified).

- Simplified registration and withdrawal processes for low-risk applicants.

- Operationalisation of GST Appellate Tribunal (GSTAT)

- Accept appeals before end of September 2025

- Commence hearings by end of December 2025

- Backlog appeals filing deadline: 30th June 2026

- Principal Bench also serves as National Appellate Authority for Advance Ruling

- Provisional GST Refunds

- CBIC to implement 90% provisional refunds for inverted duty structure and zero-rated supplies using automated data analysis and risk evaluation.

For detailed notifications and clarifications, please refer to the official Press Release on the Recommendations of the 56th Meeting of the GST Council, attached here for reference :

Conclusion

The 56th GST Council meeting introduces a simpler, more citizen-friendly tax system. With rationalised rates, insurance exemptions, reduced GST on essentials, and process reforms, the Next Generation Gst Reforms aim to ease compliance, promote economic growth, and make daily life more affordable for citizens.