DINESH P

Expert

Published on: Jun 24, 2026

Types Of Tds in India - A Complete Guide

Tax Deducted at Source (TDS) is a part of the Indian tax system, ensuring tax deduction at the source of income for individuals and businesses. Different types of income applicable to TDS, such as salary, interest income, rent, professional fees, commission, contracts, dividends, and lottery winnings, are governed by specific sections of income tax rules. Understanding threshold limits, applicable TDS rates, and compliance requirements, including TDS returns and certificates like Form 16/16A, is essential for maintaining financial accuracy and adhering to tax regulations. This article will give a complete overview of the different Types Of Tds in India.

IndiaFilings streamlines your TDS return filing with expert assistance, ensuring full compliance with tax laws!

What is TDS (Tax Deducted at Source)?

TDS (Tax Deducted at Source) is a system by the Income Tax Department of India that collects tax directly from income sources. It follows the "pay as you earn" principle, where tax is deducted before the income reaches the taxpayer. TDS applies to payments like salaries, interest, dividends, rent, and professional fees. The payer deducts the tax and remits it to the government, with the deducted amount shown in the recipient’s Form 26AS for claiming credit while filing their income tax return. TDS rates vary based on the payment type and recipient’s status.

What are the Types Of Tds?

We have given below several Types Of Tds in India and the respective threshold limit, TDS rate, and more:

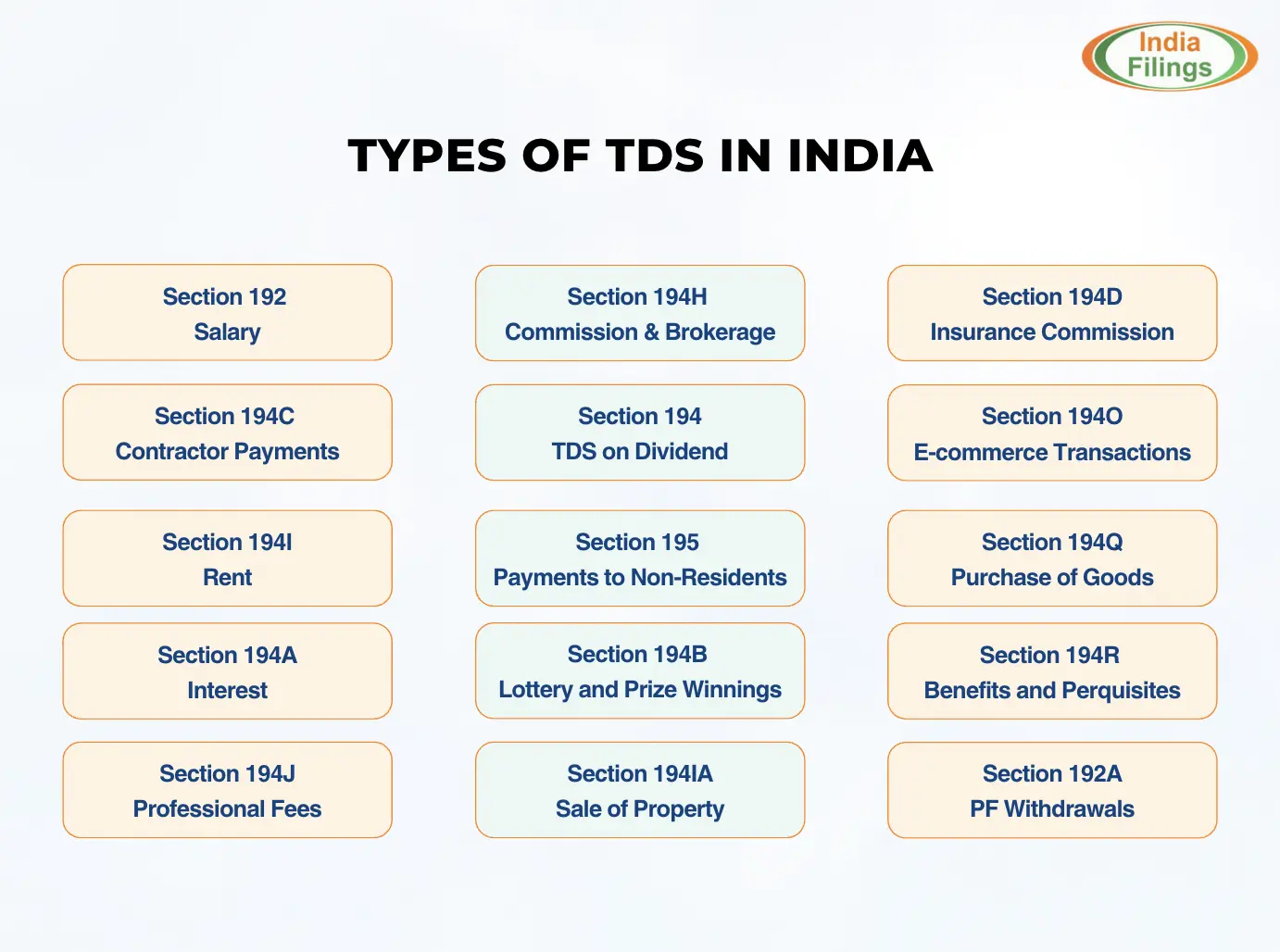

1. Section 192 - TDS on Salary

Section 192 of the Income Tax Act requires the deduction of tax at source (TDS) on salary payments made to an employee by the employer. The TDS is calculated based on the applicable income tax slabs for the financial year, considering the employee’s income, exemptions, deductions, and other applicable factors. The employer is responsible for calculating the TDS amount, deducting it from the salary, and remitting it to the government on behalf of the employee. The TDS deduction is made monthly, and a certificate (Form 16) is issued to the employee at the end of the financial year, detailing the amount of TDS deducted.

2. Section 194C - TDS on Contractor Payments

Section 194C of the Income Tax Act mandates tax deduction at source (TDS) on payments made to contractors for carrying out work contracts. This applies to both individual and corporate contractors, including those providing services like transport, construction, and labour supply. The TDS rate under Section 194C is 1% for individual or Hindu Undivided Family (HUF) contractors and 2% for others. The threshold limit for TDS deduction is ₹30,000 in a financial year, which applies when the payment is made to the contractor for work or a supply contract exceeding this limit.

3. Section 194I - TDS on Rent

Section 194I of the Income Tax Act requires tax deduction at source (TDS) on payments made for the use of land, building, machinery, or equipment under a lease, tenancy, or similar arrangement. The TDS rate for rent payments is 10% for land or buildings and 2% for rent on machinery or equipment. TDS is applicable when the total annual rent paid exceeds ₹2.4 lakh. If the payment is made to a resident, the person paying the rent is responsible for deducting and depositing the tax with the government. This provision aims to ensure that tax is collected at the source of rental income.

4. Section 194A - TDS on Interest

Section 194A of the Income Tax Act mandates the deduction of tax at source (TDS) on interest payments made to a resident, excluding interest on securities. TDS is applicable when the interest paid in a financial year exceeds ₹40,000 for individuals and ₹50,000 for senior citizens. The TDS rate under Section 194A is 10%, provided the recipient provides their Permanent Account Number (PAN). If PAN is not provided, the TDS rate increases to 20%. This provision ensures that tax is collected at the source on interest income, which applies to various forms of interest, such as bank deposits, fixed deposits, and loans.

5. Section 194J - TDS on Professional Fees

Section 194J of the Income Tax Act requires tax deduction at source (TDS) on professional or technical fees paid to a resident. This applies to payments made for legal, medical, technical, consultancy, or other professional services. The TDS rate under Section 194J is 10% for payments exceeding ₹30,000 in a financial year. If the payment is made for technical services, the rate remains the same, but for professional services, it applies to both individuals and businesses. The payer is responsible for deducting and remitting the TDS to the government within the prescribed time frame.

Also read: Guide to making online TDS payment

6. Section 194H - TDS on Commission and Brokerage

Section 194H of the Income Tax Act mandates tax deduction at source (TDS) on commission or brokerage payments made to a resident. This applies to any payment made during a business or profession, including commission, brokerage, or remuneration for services rendered. The TDS rate under Section 194H is 5% for payments exceeding ₹15,000 in a financial year. The person making the payment is responsible for deducting and remitting the TDS to the government within the prescribed time frame. This provision collects tax on income derived from commissions and brokerage services.

7. Section 194 - TDS on Dividend

Section 194 of the Income Tax Act requires tax deduction at source (TDS) on dividend payments made by a company or mutual fund to its shareholders or unit holders. The TDS rate under Section 194 is 10% if the dividend exceeds ₹5,000 in a financial year. This provision applies to all types of dividends, including those from equity shares, preference shares, or mutual fund units. The person responsible for the dividend must deduct and remit the tax to the government. If the recipient does not provide their Permanent Account Number (PAN), the TDS rate increases to 20%.

8. Section 195 - TDS on Payments to Non-Residents

Section 195 of the Income Tax Act mandates tax deduction at source (TDS) on payments made to non-residents, including foreign companies, for any income arising in India. This applies to various types of payments, such as interest, royalties, technical fees, dividends, and other income. The TDS rate under Section 195 depends on the nature of the payment and the provisions of any applicable Double Taxation Avoidance Agreement (DTAA) between India and the non-resident's country of residence. The person making the payment is responsible for deducting and remitting the TDS to the government. TDS must be deducted when making the payment, and the amount must be deposited within the prescribed time frame.

9. Section 194B - TDS on Lottery and Prize Winnings

Section 194B of the Income Tax Act mandates tax deduction at source (TDS) on winnings from lotteries, crossword puzzles, and other similar games or competitions. The TDS rate under Section 194B is 30% on the total winnings if the amount exceeds ₹10,000 in a financial year. The payer, such as the lottery organiser or competition, deducts the TDS before paying the winner. This provision ensures that tax is collected at the source on income from winnings, which is subject to the applicable tax rates.

10. Section 194IA - TDS on Sale of Property

Section 194IA of the Income Tax Act requires tax deduction at source (TDS) on the sale of property, specifically when the sale consideration exceeds ₹50 lakh. The buyer of the property is responsible for deducting 1% of the sale amount as TDS when paying the seller. This provision applies to residential and commercial property transactions and all transactions involving immovable property, excluding agricultural land. The deducted TDS must be remitted to the government within the prescribed time, and the buyer must obtain a TDS certificate for the seller.

Learn more: TDS Return Filing GuideGuide to TDS return filing in India

11. Section 194D - TDS on Insurance Commission

Section 194D of the Income Tax Act mandates tax deduction at source (TDS) on insurance commission payments made to a resident. The TDS rate under Section 194D is 5% when the commission paid exceeds ₹15,000 in a financial year. This provision applies to commissions agents or intermediaries earn from selling insurance policies. The person making the payment, typically the insurer, is responsible for deducting and remitting the TDS to the government. The TDS must be deducted at the time of payment, and if the recipient does not provide a Permanent Account Number (PAN), the TDS rate may be higher.

12. Section 194O - TDS on E-commerce Transactions

Section 194O of the Income Tax Act requires tax deduction at source (TDS) on payments made to e-commerce participants (sellers) through e-commerce platforms. The TDS rate under Section 194O is 1% for the sale of goods or services facilitated through e-commerce platforms, and the threshold limit for TDS deduction is ₹5 lakh in a financial year. This provision applies to e-commerce operators responsible for deducting and remitting TDS on the amount payable to the e-commerce participants. The TDS must be deducted when crediting or paying the seller, whichever is earlier. The TDS rate may be higher if the seller does not provide a Permanent Account Number (PAN).

13. Section 194Q - TDS on Purchase of Goods

Section 194Q of the Income Tax Act mandates the deduction of tax at source (TDS) on the purchase of goods by a buyer from a resident seller. The provision applies when the total purchases from a seller exceed ₹50 lakh in a financial year. The buyer is responsible for deducting TDS at 0.1% on the purchase amount exceeding ₹50 lakh. This section applies only to purchasing goods and applies to individuals, Hindu Undivided Families (HUF), or businesses that must deduct tax. The TDS must be deducted at the time of payment or credit, whichever occurs first, and remitted to the government.

14. Section 194R - TDS on Benefits and Perquisites

Section 194R of the Income Tax Act requires tax deduction at source (TDS) on benefits or perquisites provided to a resident like a business or professional relationship. The section applies when the aggregate value of such benefits or perquisites a person provides to the recipient exceeds ₹20,000 in a financial year. The TDS rate under Section 194R is 10%. This provision is applicable when benefits or perquisites, including gifts, vouchers, or free services, are provided in connection with a business or profession. The person providing the benefit is responsible for deducting the TDS and remitting it to the government.

15. Section 192A - TDS on PF Withdrawals

Section 192A of the Income Tax Act mandates tax deduction at source (TDS) on premature withdrawals from the Employees' Provident Fund (EPF). If the accumulated balance in the EPF is withdrawn before five years of continuous service, and the withdrawal amount exceeds ₹30,000, TDS is deducted at 10%. However, if the employee does not provide their Permanent Account Number (PAN), the TDS rate will be deducted at the maximum marginal rate (i.e.. 34.608%) . No TDS is deducted if the withdrawal is after five years of continuous service. The employer is responsible for deducting and remitting the TDS to the government at withdrawal time.

Learn more: Penalties for Late filing of TDS return

TDS Section List

We have given below the TDS section list in the table format,

Section | Nature of Payment | TDS Rate | Threshold Limit |

TDS on Salary | As per income tax slabs | N/A | |

TDS on Contractor Payments | 1% (individual/HUF), 2% (others) | ₹30,000 | |

TDS on Rent | 10% (land/building), 2% (machinery/equipment) | ₹2.4 lakh | |

TDS on Interest | 10% (PAN provided) / 20% (PAN not provided) | ₹40,000 (individual), ₹50,000 (senior citizens) | |

TDS on Professional Fees | 10% | ₹30,000 | |

TDS on Commission and Brokerage | 5% | ₹15,000 | |

TDS on Dividend | 10% | ₹5,000 | |

TDS on Payments to Non-Residents | As per agreement or DTAA | N/A | |

Section 194B | TDS on Lottery and Prize Winnings | 30% | ₹10,000 |

TDS on Sale of Property | 1% | ₹50 lakh | |

TDS on Insurance Commission | 5.00% | ₹15,000 | |

TDS on E-commerce Transactions | 1% | ₹5 lakh | |

TDS on Purchase of Goods | 0.10% | ₹50 lakh | |

TDS on Benefits and Perquisites | 10% | ₹20,000 | |

TDS on PF Withdrawals | 10% | Less or equal to ₹30,000 (withdrawing less than 5 years) |

Also read: TDS Certificates

Conclusion

In conclusion, understanding the various types of Tax Deducted at Source (TDS) in India is essential for individuals and businesses to ensure compliance with income tax regulations. Each type of TDS, from salary payments and contractor fees to rent, interest, and professional services, has specific rates and thresholds. Timely deduction and remittance of TDS help avoid penalties and ensure accurate tax credit claims. By staying informed about the different sections and requirements, taxpayers can effectively manage their financial obligations and maintain smooth financial operations in line with the law.

Simplify your TDS return filing process with IndiaFilings, minimizing your tax-related concerns and keeping your business compliant!