Dinesh P

Expert

Published on: Mar 28, 2026

Section 194J: TDS on Professional and Technical Fees

Under Section 194J of the Income Tax Act, a TDS of 10% or 2% must be deducted on payments made to residents for professional, technical, or specified services. This deduction is mandatory for all entities except individuals and Hindu Undivided Families (HUFs), ensuring tax collection at source on fees such as professional charges, royalty, and technical services.This section plays a significant role for freelancers, consultants, and business owners by outlining how TDS should be applied to payments made for legal, medical, engineering, and managerial services. Section 194J, part of the Income Tax Act of 1961, was amended by the Finance Bill 2020 with changes effective from April 1, 2020. This article covers the applicability, TDS rates, threshold limits, and consequences of non-compliance under Section 194J.

IndiaFilings helps you to file TDS returns on time with expert assistance!!

What is Section 194J TDS?

Section 194J of the Income Tax Act 1961 outlines the Tax Deducted at Source (TDS) provisions on payments made for professional and technical services. This section mandates that any payer, except individuals and Hindu Undivided Families (HUFs), must deduct TDS at rates of 10% or 2%, depending on the nature and amount of the payment when paying a resident. If the payee does not provide a Permanent Account Number (PAN), the TDS rate increases to 20%. For non-resident Indians, technical service fees are subject to TDS at 20% under Section 195. Section 194J applies to a wide range of professional fees, including those paid to lawyers, doctors, engineers, architects, chartered accountants, and interior decorators. It also covers management, technical, and consulting services.What is Section 194J TDS Threshold Limit?

Under Section 194J of the Income Tax Act, the threshold limit for deducting tax is ₹30,000. This means that TDS must be deducted if the professional or technical services payment exceeds ₹30,000 in a financial year. It is important to note that this limit applies to each payment individually. For example, suppose a company pays ₹25,000 to a lawyer in January and ₹35,000 in June for different legal services. In that case, TDS will only apply to the ₹35,000 payment since it exceeds the ₹30,000 threshold. Each payment is considered separately, so even if the total costs to a single professional or service provider exceed ₹30,000, TDS is only required if an individual payment surpasses this limit.Types of Payments Covered Under Section 194J

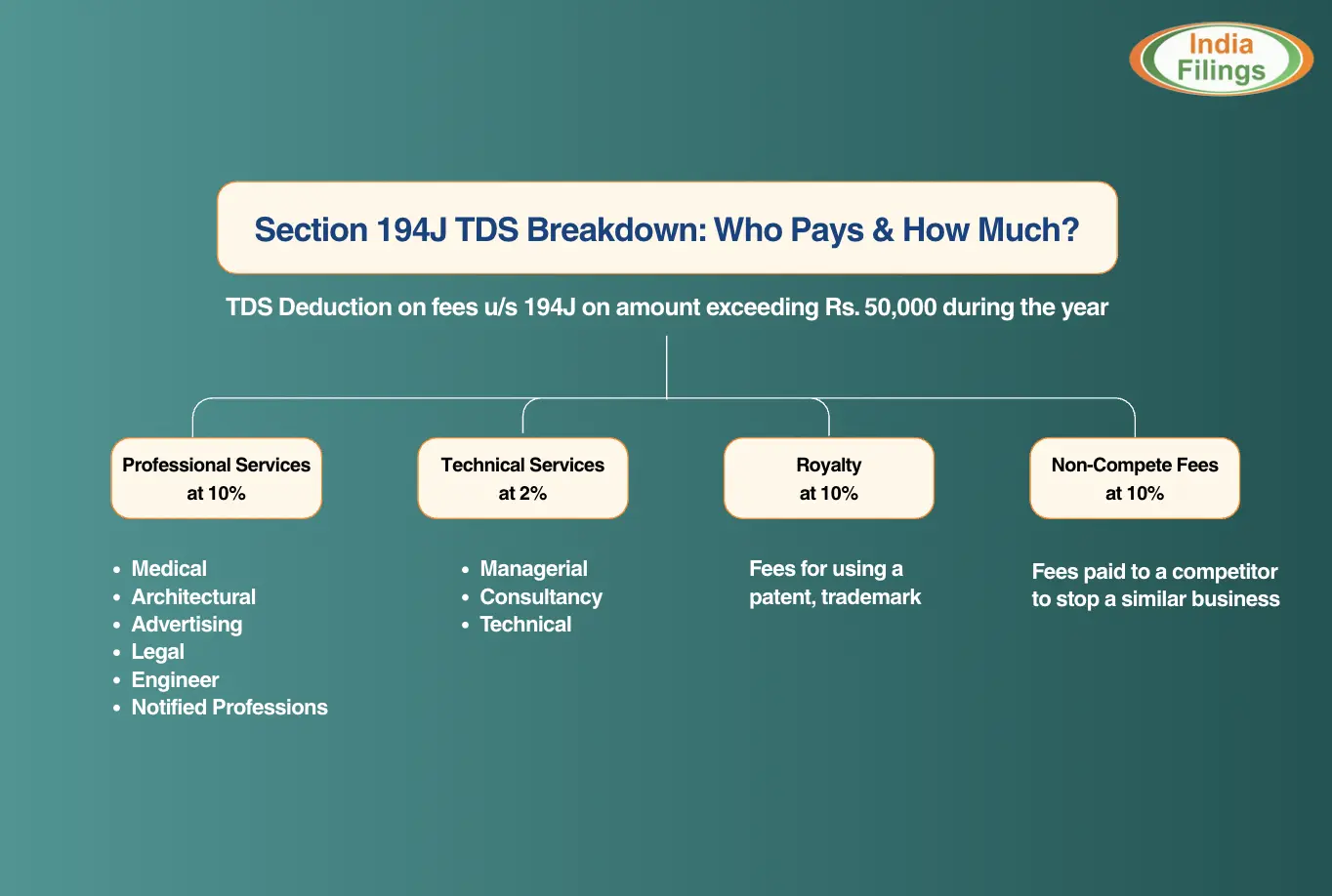

Section 194J of the Income Tax Act mandates that certain payments made to residents or non-residents must be subject to Tax Deducted at Source (TDS). This section aims to ensure that the government receives the necessary tax revenue.

Let's delve into the specific types of payments covered under this section:

Professional Fees:

Professional fees refer to payments made to individuals for their expertise in various fields, including:

Under Section 44AA, the CBDT has notified additional professions that are liable to TDS on professional fees, such as:

Technical Service Fees:

Technical service fees encompass payments made for:

However, it's important to note that this does not include payments that the recipient considers as compensation.

Technical services involve providing expertise or knowledge in a specific field, while managerial services often pertain to the operation and management of a client's business. Consultancy services involve offering advice and guidance to clients.

The Supreme Court has ruled that human services generally fall under the category of technical services, excluding those rendered by robots or machines.

Royalty:

Royalty payments are made to individuals for the transfer or use of their intellectual property rights, such as:

These payments can include license fees for using a brand name or other intellectual property.

Royalty payments are typically made for:

Non-Compete Fees:

Non-compete fees are payments made to individuals to prevent them from disclosing or using certain information, such as:

These payments can be made in cash or in kind.

By understanding these types of payments, individuals and businesses can ensure compliance with Section 194J and avoid penalties.

Who is Liable to Deduct TDS under Section 194J?

Section 194J mandates that certain individuals or entities withhold TDS when paying for professional or technical services. However, there are specific exemptions for certain individuals and Hindu Undivided Families (HUFs).

Individuals and HUFs are exempt from TDS under Section 194J if:

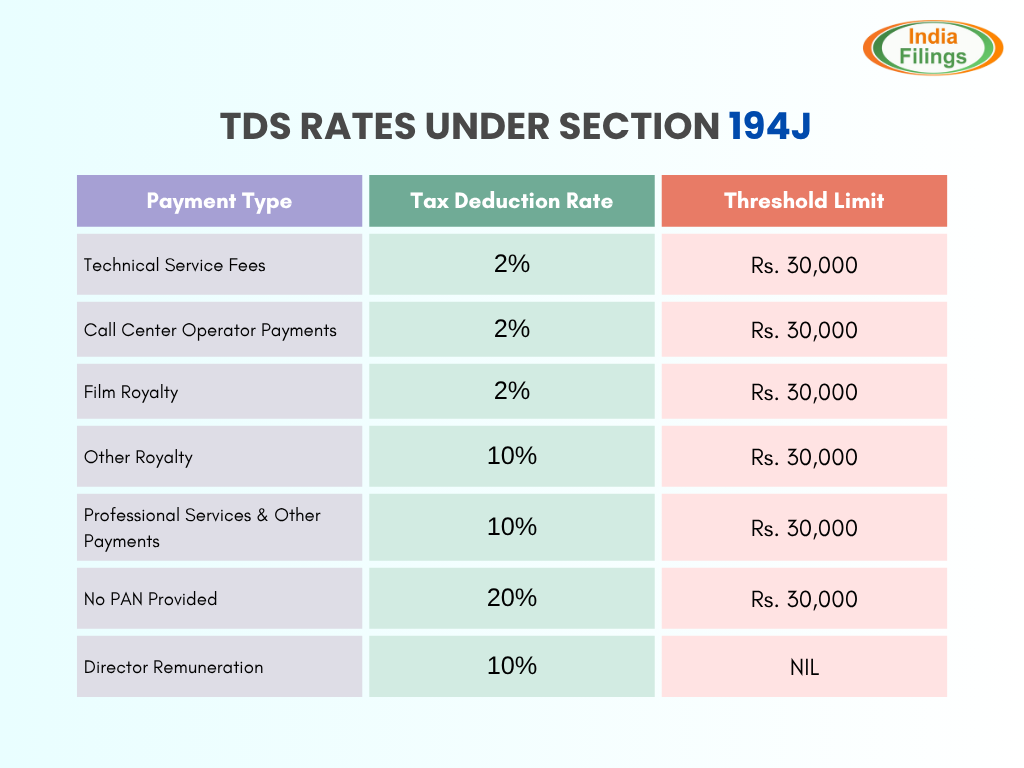

Section 194J TDS Rates

The rate of Tax Deducted at Source (TDS) under Section 194J varies depending on the nature of the payment. Here's a breakdown of the applicable TDS rates and threshold limits:

| Payment Type | Tax Deduction Rate | Threshold Limit |

| Technical Service Fees | 2% | Rs. 30,000 |

| Call Center Operator Payments | 2% | Rs. 30,000 |

| Film Royalty | 2% | Rs. 30,000 |

| Other Royalty | 10% | Rs. 30,000 |

| Professional Services & Other Payments | 10% | Rs. 30,000 |

| No PAN Provided | 20% | Rs. 30,000 |

| Director Remuneration | 10% | Nil |

What is the Time Limit for the Deposit of 194J TDS?

The time limit for depositing TDS under Section 194J varies depending on the payment type and whether the deductor is a government or non-government entity.Non-Government Deductors:

- Payments made before March 1st: The TDS must be deposited within 7 days from the end of the month the payment was made.

- Payments made in March: The TDS must be deposited by April 30th.

Government Deductors:

- Payments made before March 1st: The TDS must be deposited within 7 days from the end of the month the payment was made.

- Payments made in March: The TDS must be deposited by April 30th.

Penalties for Non-Deducting or Late Deduction of TDS under Section 194J

Failing to deduct or remit TDS under Section 194J can result in significant penalties and consequences. These include:Disallowance of Expenditure:

- Non-resident payments: Any payments made to non-residents without withholding TDS or timely remittance can be disallowed as expenses under Section 40(a)(ia) of the Income Tax Act. However, this disallowance can be reversed if the TDS is subsequently withheld or remitted.

- Resident payments: Payments made to residents without withholding TDS or timely remittance can result in a 30% disallowance under Section 40(a)(ia).

Levy of Interest:

- Non-deduction or late deduction: If TDS is not deducted or is deducted late, interest will be charged on the TDS amount from the date it was due to the payment date. The interest rate is 1% per month or part thereof.

- Late payment: If the TDS is deducted but not paid to the government on time, interest will be charged on the total TDS amount from the date of deduction to the date of payment. The interest rate is 1.5% per month or part thereof.

Levy of Penalty:

- Non-deduction or late deduction: A penalty equal to the amount of the non-deducted or late-deducted TDS can be imposed under Section 271C of the Income Tax Act.

- Non-payment of tax demand: If the assessee fails to pay the tax demand made by the assessing officer, additional penalties can be imposed under Section 221 of the Income Tax Act. The penalty amount is based on the duration of the payment delay and cannot exceed the tax demand.

Prosecution:

- Non-remittance of TDS: In severe cases of non-remittance of TDS, the offender may face prosecution with a minimum imprisonment of three months and a maximum of seven years.

Example 1: TDS on Professional Services Rendered

Scenario:

Ms. Kavya has availed professional consultancy services from Ms. Neha during the Financial Year (F.Y.) 2025–26.

- First payment: Rs. 60,000 in May 2025

- Second payment: Rs. 30,000 in January 2026

Let’s evaluate the TDS applicability in the following three situations:

Situation 1: Ms. Kavya is not liable for audit under Section 44AB

Since Ms. Kavya is not liable for tax audit, she is not required to deduct TDS under section 194J when making payments to Ms. Neha, regardless of the amount paid.

Situation 2: Ms. Kavya is liable for audit u/s 44AB but services were for personal purposes

Even though Ms. Kavya is liable to tax audit, no TDS needs to be deducted since the professional services from Ms. Neha were used for personal purposes, and not in connection with her business or profession.

Situation 3: Ms. Kavya is liable to audit, and the services were for business purposes

In this case, TDS @10% under section 194J must be deducted.

Since the first payment of Rs. 60,000 exceeds the threshold limit of Rs. 50,000, TDS of Rs. 6,000 must be deducted at the time of credit or payment, whichever is earlier.

Additionally, because the annual limit has been crossed, TDS should also be deducted on subsequent payments, including the Rs. 30,000 paid in January. Therefore, another Rs. 3,000 should be deducted on the second payment.

Example 2: TDS on Technical/Professional Services – Sports Coaching

Scenario:

A Tennis Academy in India has engaged Mr. Arjun, a resident coach, for training services. The annual remuneration paid to Mr. Arjun is Rs. 8,00,000.

Analysis:

As per Section 194J of the Income Tax Act, coaching services for sports fall under the category of professional services. Since the payment made to Mr. Arjun exceeds Rs. 50,000 in a financial year, the Tennis Academy is required to deduct TDS at the applicable rate of 10%.

Hence, TDS of Rs. 80,000 must be deducted from Mr. Arjun’s total remuneration and deposited with the government.

Conclusion

Section 194J of the Income Tax Act is a crucial provision for individuals and businesses involved in professional and technical services in India. Understanding the TDS requirements outlined in this section is essential for ensuring compliance with tax laws and avoiding penalties. Taxpayers can contribute to efficient tax collection and avoid legal repercussions by accurately deducting and remitting TDS on applicable payments. We hope you got a lot of information, including the comprehensive overview of Section 194J, the types of payments covered, the applicable TDS rates, threshold limits, time limits for deposit, and potential penalties for non-compliance.Streamline your TDS return filing with IndiaFilings experts!!

Frequently Asked Questions – TDS under Section 194J

1. How can I verify the tax deducted under Section 194J?

You can verify your TDS deductions by:

- Reviewing Form 16/16A issued by the deductor.

- Accessing your Form 26AS via the TRACES portal or the Income Tax e-filing website.

2. Does remuneration paid to a company director attract Section 194J?

Yes. Remuneration or fees paid to a director for managerial services, other than salary, fall under technical services and are liable for TDS at 2% under Section 194J.

3. If a professional is paid Rs. 10,000 initially and Rs. 50,000 later in the same financial year, how is TDS applied?

- No TDS on the first payment (Rs. 10,000), as the threshold was not crossed.

- Once the second payment (Rs. 50,000) is made, the cumulative total becomes Rs. 60,000, exceeding the Rs. 50,000 limit.

- TDS at 10% must be deducted on the entire Rs. 60,000.

4. What is Section 194J under the Income Tax Act?

Section 194J deals with TDS on fees for professional or technical services. Any person making such payments to a resident is required to deduct tax at source as per the specified rate.

5. Who is liable to deduct TDS under Section 194J?

Any individual, HUF, firm, company, or other entity, except individuals and HUFs not liable for tax audit, must deduct TDS under Section 194J.

Individuals and HUFs are liable only if their accounts are subject to audit under Section 44AB.

6. What is the threshold limit for deduction of TDS under Section 194J?

TDS is applicable only if the total payments to a professional or technical service provider exceed Rs. 50,000 in a financial year.

7. What services are covered under Section 194J?

The following payments attract TDS under Section 194J:

- Professional services (e.g., legal, medical, consultancy)

- Technical services

- Royalty payments

- Director’s remuneration (excluding salary)

- Non-compete fees

8. Is TDS applicable on payments made to models under Section 194J?

No, modelling is not a notified profession under Section 194J. TDS under this section is not applicable unless the services relate to films or entertainment, in which cas,e different provisions may apply.

9. Is TDS required if professional consultancy is used for personal purposes?

No. If an individual or HUF avails professional or technical services strictly for personal use, TDS under Section 194J is not required, even if tax audit provisions apply.

10. When is TDS not required under Section 194J?

TDS is not applicable under Section 194J in the following cases:

- The payer is an individual or HUF not liable for audit under Section 44AB.

- The services availed are for personal purposes.

- The payment does not exceed Rs. 50,000 in a financial year.