IndiaFilings

Published on: Apr 22, 2026

GST Registration for Importers

GST registration is mandatory for taxable persons under GST. In most states, businesses having an annual aggregate turnover of more than Rs.40 lakh (In some states, Rs.20 lakh) should mandatorily obtain GST registration. In addition to the turnover criteria's other conditions have also been specified by the GST Council. However, all importers should mandatorily obtain GST registration, the individual requires GSTIN for clearing goods from the Customs Department. In this article, let us look GST registration for importers in detail.

GST Registration Required for Import of Goods

After the implementation of GST on 1st July 2017, the procedure and documents required for import of goods into India have changed. From 1st of July, 2017, quoting of GSTIN is mandatory for filing Bill of Entry as IGST is to be paid on imports and input tax credit can be availed for IGST paid. In addition to GSTIN, the requirement for PAN of the importer and IE Code for the importer would continue. Hence, all importers would be required to obtain

GST registration, PAN and IE Code for their business or complete

GST migration- if they had an existing tax registration.

IE Code Required for Import of Goods

Even after the implementation of GST, IE Code and PAN will be required for import. Import Export Code or IE Code is a registration under the Directorate General of Foreign Trade (DGFT) mandatorily required for import of goods into India. To obtain IE Code, a business would have to apply with the following documents to DGFT:

- Digital Photograph (3x3cms) of the Managing Partner.

- Copy of PAN card of the applicant entity.

- Copy of Passport (first & last page)/Voter’s I-Card /UID (Aadhar Card) /Driving License/PAN (any one of these) of the Managing Partner signing the application.

- Copy of Partnership Deed.

- Sale deed for self-owned business premises; or Rental/Lease Agreement, for rented/ leased office; or latest electricity /telephone bill.

- Bank Certificate as per ANF 2A (I)/Cancelled Cheque bearing preprinted name of the applicant entity and A/C No.

Import Procedure under GST

Integrated Goods and Services Tax and GST Compensation Cess would be applicable for cargo that arrives on or after 1st July 2017. Further, IGST shall apply on cargo that arrived prior to GST implementation for which Bill of Entry filed on or after 1st July 2017. In addition, if cargo arrived after 1st July 2017 but the individual filed the Bill of Entry in advance, then the Officer shall recall the Bill of Entry and assess the levy of IGST and GST Compensation Cess through the authority as provided.

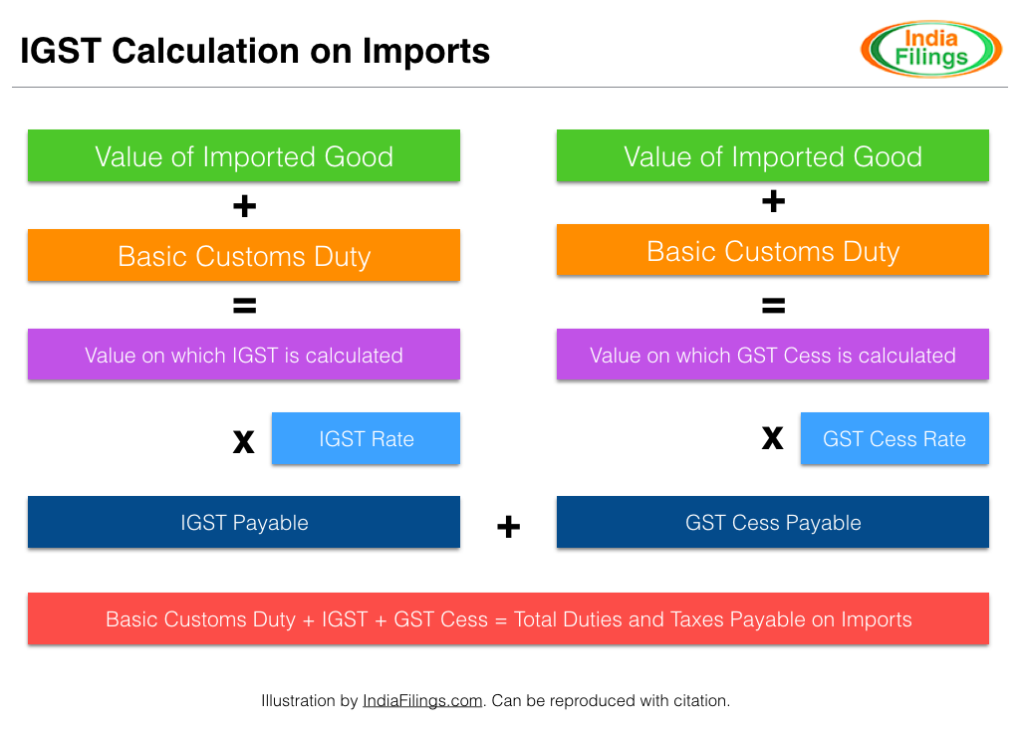

The procedure for calculating IGST on Imports is illustrated below:

IGST on Imports - Calculation Methodology

Input Tax Credit for IGST Paid on Imports

Under GST,

input tax creditis provided for the IGST and

GST Compensation Cesspaid on imports. However, the input tax credit cannot be availed for Basic Customs Duty or other types of customs duty paid during import. The GSTIN mentioned in the Bill of Entry shall apply to track the flow of input tax credit from import to consumption. Hence, in order to avail input tax credit, importers would have to mandatorily declare their GSTIN and

file GSTR-2showing details of inward supply.