IndiaFilings

Expert

Published on: Apr 22, 2026

How to Generate GST E-Way Bill

GST Way bill or E-Way bill must be generated for any transport of goods within India wherein the value of the consignment is over Rs.50,000. GST E-Way bill needs to be generated not only for the transport of goods on account of sales but also for any other reason like inter-branch transfer, purchase from an unregistered person, and transfer on account of job work. In this article, we look at the procedure for generating the GST Way Bill in India.

Step 1: Generate Form GST EWB-01

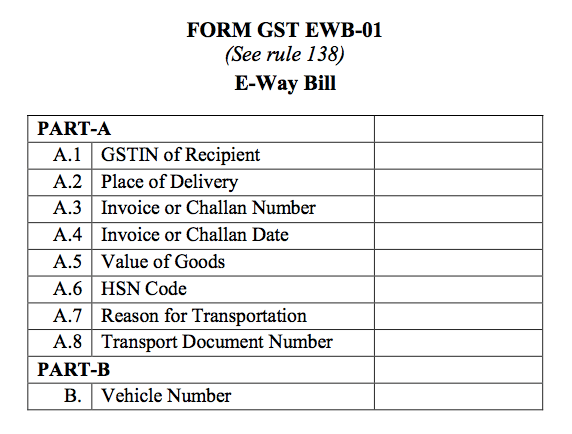

To generate a GST E-way bill, the person initiating the transport must provide details of the goods being transported on the GST Common Portal. The registered taxpayer can generate the GST E-way bill from the GST portal by logging into their GST account. While generating for the E-way bill, the taxpayer must provide the following details in GST EWB-01 on the GST Portal:

- GSTIN of Recipient

- Place of Delivery

- Invoice or Challan Number

- Invoice or Challan Date

- Value of Goods

- HSN Code

- Reason for Transportation

- Transport Document Number

For the place of delivery, the pin code of place of delivery must be provided. For Transport Document number, the Goods Receipt Number or Railway Receipt Number or Airway Bill Number or Bill of Lading Number must be provided. Reason for transportation can be any of the following:

- Supply

- Export or Import

- Job Work

- SKD or CKD

- Recipient not known

- Line Sales

- Sales Return

- Exhibition or fairs

- For own use

- Others

Form GST EWB-01

Form GST EWB-01

Step 2: Provide Details of Transport

The second step after completing Form EWB-01 Part-A is updating of the information about the transport vehicle in Part-B of GST EWB-01.

If the supplier or customer transports the goods through own vehicle or a hired vehicle or by railways or air or ship, the concerned individual can update the Part-B or information about the transport vehicle by the supplier itself.

If the supplier hands over the goods by a supplier to a transporter for transportation by road, the supplier must provide details in Part-A required for the generation of the e-way bill to the transporter. The transporter would then generate an e-way bill based on the information provided by the supplier by completing Part-B. In the following scenarios, the details of transport need not be provided. Goods can be transported by providing information required under EWB Part-A only:

- If goods are transported for a distance of less than ten kilometres within the State or Union territory from suppliers place of business to a transporter for transportation, the supplier need not furnish details of the transport on the GST common portal.

- If goods are transported for a distance of less than 10 kilometres from a supplier to a recipient, then details of transport need not be provided on the GST portal for generation of E-way bill.

After a generation of the e-way bill by providing information about the transport or vehicle, a unique e-way bill number of EBN will be provided. In case the vehicle is changed during the transit, the transporter would have to update details of conveyance in the e-way bill on the GST portal.

Also read on

Bond for Release of Seized Goods under GSTValidity of GST E-way Bill

E-way bill generated on the GST common portal will be valid across all States and Union Territories. An e-way bill generated for a distance of upto 100 kilometres will be valid for one day. For every 100 additional kilometres, the e-way bill would be valid for an additional day. Hence, an e-way bill for a distance of 500 kilometres would be valid for 5 days.

In case the transport cannot be completed within the validity period due to circumstances of an exceptional nature, the transporter can generate a new e-way bill after updating details of the transport. Also, a Commissioner through notification can extend the validity period of the e-way bill for certain categories of goods.

Get expert help from IndiaFilings to register for a Private Limited Company, Public Limited Company or One Person Company!