IndiaFilings

Expert

Published on: Apr 22, 2026

What is Minimum Alternate Tax (MAT)?

Minimum alternate tax or MAT is applicable for Companies and Limited Liability Partnerships (LLPs) wherein the company or LLP is required to pay a minimum tax based on the book profit of the company. Without the concept of MAT, a large number of companies and LLPs were having book profit as per their profit and loss accounts but were not paying any tax since their income computed as per the Income-tax act was either, nil or negative or insignificant. Thus, to regularize such taxpayers, the concept of MAT was introduced in India.

Difference Between Book Profit and Income Tax Profit

There is a difference between book profit of a company and income tax profit of a company:

Book Profit of a company is calculated on the basis of Companies Act, 2013 taking into account the depreciation rates and deduction allowed as per the Companies Act. Income Tax Profit of a company is calculated on the basis of Income Tax Act, which allows for various incentives and deductions (Eg: Accelerated depreciation for Windmills) from the profit of the company. Hence, there is usually a difference between the book profit and income tax profit of the company. Further, many corporates do prior tax planning like investing in windmills, etc., and try to minimize their income tax payments by reducing their income tax profit.

Minimum Alternate Tax (MAT) for Companies

MAT for companies was introduced due to a rise in the number of zero-tax companies, wherein a company was declaring a book profit and declaring dividends to shareholders, while not paying any income tax since the income computer as per income tax act was negative or negligible. In 1983, the government introduces MAT in order to bring such companies into the income tax net and make them pay income tax.

For companies, the Minimum Alternate Tax (MAT) rate applicable is 18.5% of the book profit for the assessment year 2015-16. Therefore, a company has to pay taxes based on the higher income tax profit of the company or the MAT at 18.5% of the book profit.

If the company pays an excessive amount of MAT than a regular tax, then it classifies the excess amount as MAT Credit and the company carry forward to setoff future tax liability. To know more about

MAT vs AMTAlternate Minimum Tax for LLPs

Alternate Minimum Tax (AMT) similar to MAT is applicable for Limited Liability Partnership (LLP). The provisions of AMT will not be applicable to an individual or Hindu Undivided Family (HUF) or a Partnership if the total adjusted income of the person or entity is less than 20 lakh rupees.

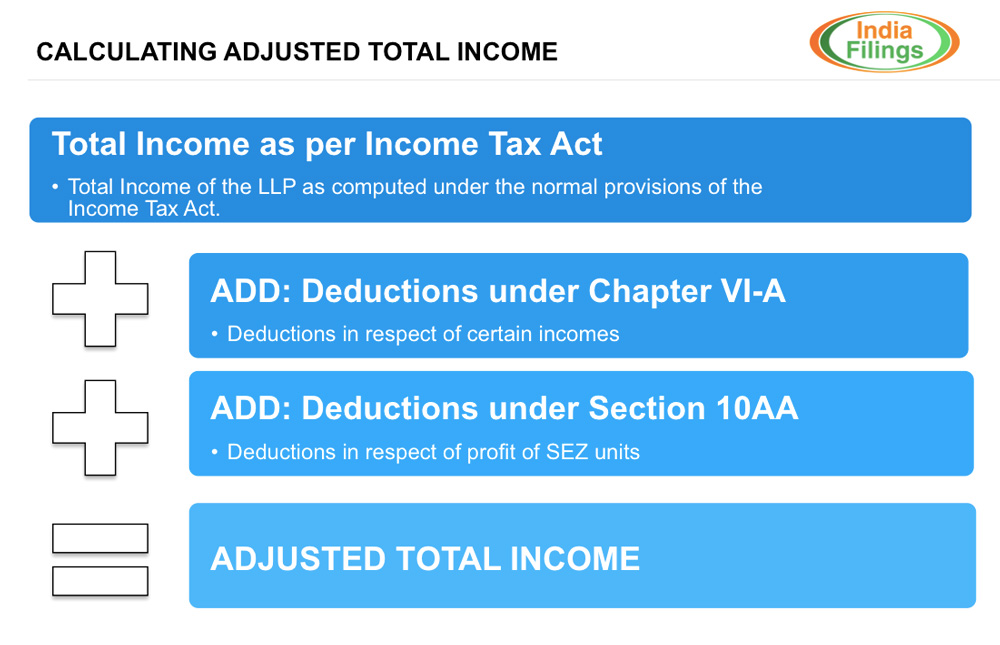

The current AMT rate is 18.5% plus education cess of adjusted total income, making the effective rate 19.055%. Adjusted total income can be calculated by using the following methodology:

Calculating Adjusted Total Income

The AMT Credit is available for the person who pays the AMT in excess of the regular tax. AMT credits are against the future tax liability of the LLP for upto 10 succeeding years.

Calculating Adjusted Total Income

The AMT Credit is available for the person who pays the AMT in excess of the regular tax. AMT credits are against the future tax liability of the LLP for upto 10 succeeding years.