IndiaFilings

Expert

Published on: Apr 22, 2026

Small Company as per Companies Act, 2013

The concept of a small company was introduced in Companies Act 2013 to provide certain advantages for small businesses operating as a private limited company. Small businesses are the backbone of any economy and it the procedure for starting and managing a small business must be made simple to boost employment and the economy. Therefore, the classification of "small company" in the Companies Act, 2013 goes a long way in promoting the small business in India. In this article, we review the definition of a small company as per the Companies Act, 2013 and the advantages enjoyed.

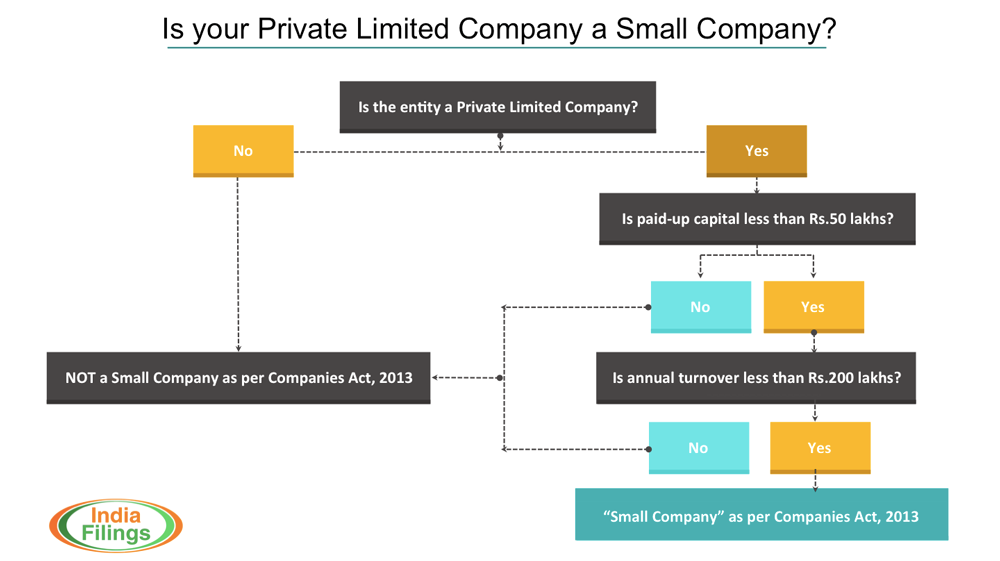

Small Company Definition as per Companies Act 2013

Updated: Section 2(85) of the Companies Act, 2013 defines "Small Company" in the following manner:

- The small company’’ means a company, other than a public company,-

- paid-up share capital of which does not exceed fifty lakh rupees or such higher amount as may be prescribed which shall not be more than five crore rupees;

- turnover of which as per its last profit and loss account does not exceed two crore rupees or such higher amount as may be prescribed which shall not be more than twenty crore rupees: Provided that nothing in this clause shall apply toA) a holding company or a subsidiary company; B) a company registered under section 8; orC) a company or body corporate governed by any special Act;

As per Companies Act, 2013 a company may be treated as a ‘small company’ if it meets either of the conditions (1) or (2) provided above. However, most companies were being classified as a small company since they meet criteria one but exceeded the monetary limit in respect of second criteria excessively. Therefore, in an effort to curb too many from being classified as a small company, the Ministry of Corporate Affairs changed "OR" at the end of condition 1 to "AND". The update to the definition was published in The Gazette of India on February 13, 2015. Updated Small Company Definition. Hence, a small company is now defined as above.

Check if your Company can be classified as a Small Company as per Companies Act, 2013

Check if your Company can be classified as a Small Company as per Companies Act, 2013

Most Startups will be Small Company

Since most of the startups will have a paid-up capital of fewer than Rs.50 lakhs and also an annual sales turnover of fewer than Rs.200 lakhs, they will be classified as a small company. The difference between authorized capital and paid-up capital can be gleaned from the article on "Authorized Capital of a Private Limited Company".

Advantages for Small Company

A private limited company that can be classified as a small company enjoys a number of benefits under the Companies Act, 2013 and lesser compliance formalities. Some of the advantages enjoyed are:

- Filing Annual Return

- The annual return of a private limited company classified as a small company can be signed by a Company Secretary or by a Director of the private limited company.

- The annual return of a private limited company NOT classified as a small company must be signed by a Director AND a Company Secretary.

- Board Meeting

- It is sufficient for a small company to conduct only two Board Meetings in a financial year.

- Private limited company NOT classified as a small company are required to conduct four Board Meetings in a financial year.

- Cash Flow Statement

- A private limited company classified as a small company need NOT prepare a cash flow statement as a part of the financial statement.

- Private limited company NOT classified as a small company MUST prepare a cash flow statement as a part of the financial statement.

- Rotation of Auditors

- The private limited company classified as a small company are NOT required to rotate Auditors.

- Private limited company NOT classified as a small company MUST rotate Auditors every 5 or 10 years as per the Act.