Renu Suresh

Expert

Published on: Apr 20, 2026

House Rent Allowance (HRA) Calculation

House Rent Allowance (HRA) is an amount paid by the employer to his employee as a part of the salary. The purpose of providing house rent allowance is to meet the cost of living in rented accommodation. HRA also allows employees to get tax benefits towards the payment for accommodations every year. House Rent Allowance calculation is regulated by the provisions of Section 10(13A) of the Income Tax Act. The employer decides how much HRA needs to be paid to the employee based on several different criteria, such as the salary and the city of residence. In this article, we will look at the House Rent Allowance (HRA) Calculation in detail.HRA Applicability

According to the Section 10(13A) of the Income Tax Act, the tax benefit is available only to the salaried individuals who have the House Rent Allowance component as part of the salary structure and staying in rented accommodation. Self-employed professionals cannot avail the deduction. If the individual is not living in rented accommodation, the entire HRA component of his/her salary is taxable. On the other hand, if he/she is paying rent regularly, a part of the HRA component is exempt from tax.Benefits of HRA

The main benefits of HRA are given in detail below:Reduces Taxable Income

The HRA amount is deducted from the gross salary of an employee, only after which income tax is charged on the net income. This is advantageous to the eligible employees, by lowering their taxable income, which eventually reduces the tax paid.Improves Affordability of Living Costs

HRA reduces the burden on employees, especially who have moved from their homes to a new place. With the increasing cost of living, many people are unable to manage such changes. Companies can help eligible employees by making rent costs more affordable through HRA, which reduces taxable income.Combined with Housing Loan

Income tax exemption can be claimed on both house rent allowance and home loan repayment. It is an added advantage for employees living in a rented property and repaying a house loan on another property. It is because tax exemption can be claimed by combining both HRA and housing loan. Note: In a particular situation, where a person owns a house, but choose to stay in rented accommodation because of any particular reasons, he/she can claim the HRA and exemptions on the home loan interest at the same time.Criteria for Calculation of HRA

As stated above, the House Rent Allowance is decided based on the salary. However, some other factors also affect HRA, such as the city in which the employee resides.- In case the individual lives in a metro city, then he is entitled to a House rent allowance equal to 50% of the salary.

- For cities other than a metro, the entitlement is 40% of the salary.

HRA for Central Government Employees

For the Central Government employees, the minimum and maximum house rent allowance in different cities were recently modified in 2017 as per the recommendations of the Seventh Pay Commission. For the HRA calculation purpose, cities have been divided into three parts such as X, Y and Z.|

City Category |

Population | HRA Calculation (as a percentage of salary) |

Minimum HRA (in Rs) |

|

X |

Above 50 lakh | 30% | Rs.5400 |

|

Y |

5 lakh to 50 lakh |

20% |

Rs.3600 |

| Z | Below 5 lakh | 10% |

Rs.1800 |

HRA Calculation

The House Rent Allowance serves as a vital component of an individual's salary. The calculation of house rent allowance for tax benefit is considered from any of the following three listed provisions:- The actual rent that is paid should be less than 10% of the basic salary.

- In case a person is staying in a metro, 50% of the basic salary and 40% if he lives in a non-metro city.

- The actual amount allotted by the employer as the house rent allowance (HRA).

HRA Calculation Period

The computation can be clubbed together for a period during which all the above items are the same. If any item changes during the year, then the computation is to be made for different periods. In this case, the HRA will be computed into the following parts :- Computation for April to June period.

- Computation for July to October period

- Computation for November to December period

- Computation for January to March period

HRA Claim Rules

The rules that apply to HRA claims are explained in detail below:- The allotted HRA cannot exceed more than 50% of the basic salary.

- As a salaried employee, the person cannot claim for the full rental amount he/she is paying. The exemption will be based on the least of the below-mentioned options:

- 50% of salary, when the residential house is situated at Mumbai, Kolkata, Delhi or

- Chennai and 40% of salary where residential house is situated at any other place.

- HRA received by the employee in respect of the period during which the employee and rent occupy rental accommodation is incurred by the employee during the previous year.

- Rent paid in excess of 10% of salary. The employee can also avail tax benefits of HRA along with a home loan.

- In case a person stays with his parents, he is eligible to pay rent to his parents and collect a receipt for the HRA claim. However, similar rules don't allow him to pay rent t his spouse and claim a tax exemption.

- If the annual rent of the accommodation exceeds Rs.1 lack, then the landlord's PAN card is essential. In case the landlord does not have a PAN, he/she can furnish a self-declaration.

- Another important rule is that, if your landlord is an NRI, you have to deduct 30% tax from the rent amount that requires to be declared.

Documents Required for HRA Exemption

- For HRA exemption, the applicant needs to produce the Rent Receipts.

- In case the monthly rent exceeds Rs. 3,000 monthly, then rent receipts will be required. However, if the rent paid is up to or lesser than Rs. 3000, rent receipts need not be provided.

- In case, the rent amount exceeds Rs.15,000 per month or Rs. 1 Lakh annually, then either the PAN card of the landlord or written consent (stating the PAN is not available) from the landlord is required.

Procedure to Claim HRA Exemption

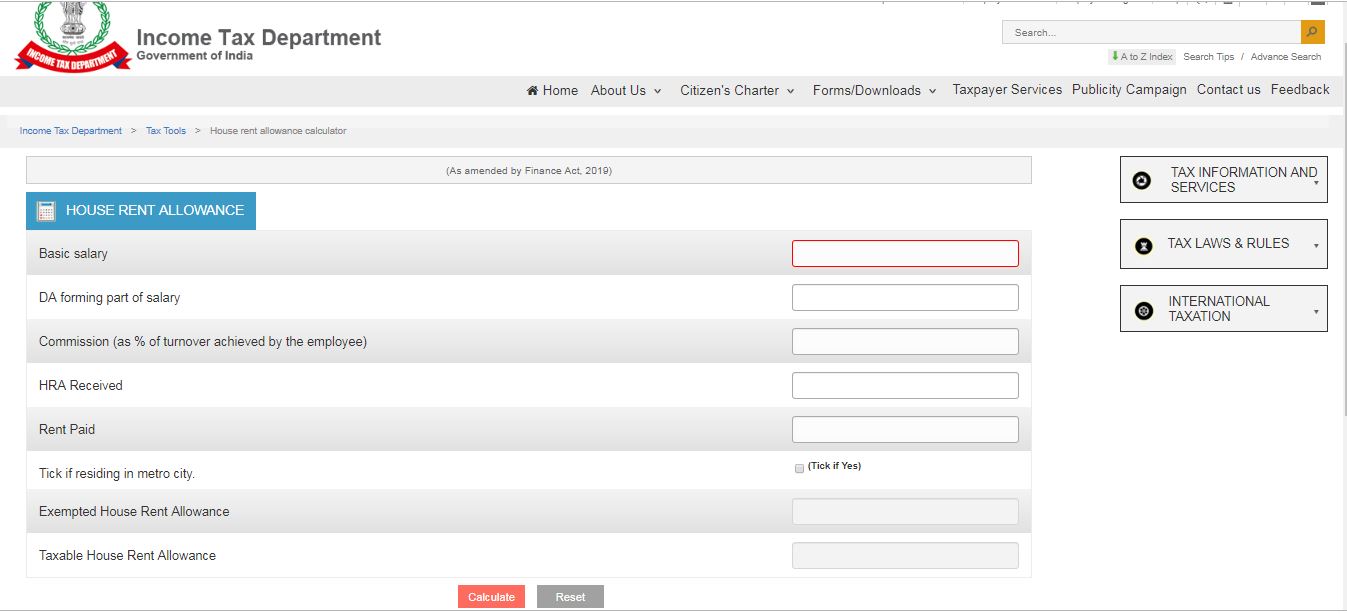

The simplest ITR form 1 requires taxpayers to provide break up of their salary details. Therefore, any portion of HRA which is taxable will be required to be reported while filing Income Tax Return. If you do not submit the documents such as rent agreement or rent receipts to your employer, then he/she deducts higher TDS from your salary. However, you can claim the tax-exemption benefit available on HRA while filing the income tax returns (ITR). If you have not submitted the HRA documents to your employer, the Form-16 will show the HRA portion of the salary as fully taxable. The payable amount of wages, as shown in the Form-16, will be higher than the calculations made. The employee is first required to calculate how much of the allowance is taxable to claim the HRA exemption. The minimum tax-exempt portion of HRA received will be calculated based on the rules mentioned above:House Rent Allowance Calculator

The Income Tax Department provides an online calculator for House Rent Allowance. By providing the details of basic salary, DA forming part of the salary, commission, HRA received, rent paid, Exempted HRA and Taxable HRA, the House Rent Allowance can be calculated. House Rent Allowance (HRA) Calculation

House Rent Allowance (HRA) Calculation