IndiaFilings

Expert

Published on: Jun 24, 2026

Gst Electronic Credit Ledger

GST utilizes three ledgers, namely

electronic cash ledger, electronic liability register and electronic credit ledger for levying, calculating and tracking GST payments, liability and credits. All the three ledgers for maintained for each of the taxpayers in the GST Common Portal and is accessible to the taxpayer. In this article, we look at the electronic credit ledger in detail.Credit for Input Tax Credit

All persons registered under GST, not being a person registered under composition scheme are entitled to take the

input tax credit on any goods or services used as input by the taxpayer for the furtherance of business. The credit for the input tax credit is credited to the electronic credit ledger of the taxpayer.Conditions for Electronic Credit Ledger

- The electronic credit ledger should be maintained in Form GST PMT-02 by the registered taxpayer are those eligible for claiming the input tax credit. Further, this electronic credit ledger reflects the amount credited against every claim of an input tax credit.

- The registered taxpayers can claim a refund of any unutilized amount from the electronic cash ledger. However, the portal debits the refund claimed in the electronic credit ledger.

- The concerned authority may reject the refund claimed either fully or partly. In such instances, the debited amount re-credits to the electronic credit ledger. To claim the debited amount, the individual shall apply through Form GST PMT-03 to the proper officer.

- Apart from the above mentioned rules, the taxpayer should avoid making any direct entries in the electronic credit ledger under any circumstance.

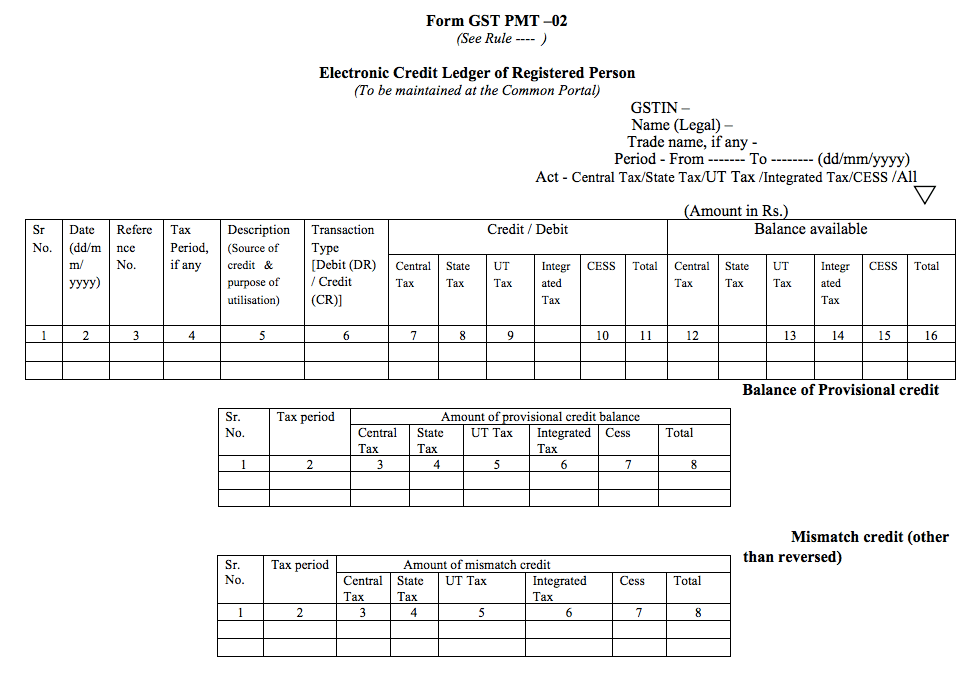

Electronic Credit Ledger Format

Electronic Credit Ledger Format

The GST Portal maintains the Electronic credit ledger in the above format. All the approved claims for input tax credit are credited to the electronic credit ledger under the appropriate head of CGST, SGST or IGST, UTGST and GST Cess. Further, after any debits for liability, the available balance credit for CGST, SGST, UTGST, IGST and GST Cess is also provided in the electronic credit ledger.

Also, for reference, the unique identification number is generated at the Common Portal for each credit in the electronic liability register for reasons other than those cov.

Electronic Credit Ledger Format

The GST Portal maintains the Electronic credit ledger in the above format. All the approved claims for input tax credit are credited to the electronic credit ledger under the appropriate head of CGST, SGST or IGST, UTGST and GST Cess. Further, after any debits for liability, the available balance credit for CGST, SGST, UTGST, IGST and GST Cess is also provided in the electronic credit ledger.

Also, for reference, the unique identification number is generated at the Common Portal for each credit in the electronic liability register for reasons other than those cov.

Incorrect Information in Gst Electronic Credit Ledger

In case any incorrect information is noticed in the electronic credit ledger, the taxpayer can raise a request in the GST Common Portal using FORM GST PMT-04. Details to be provided in GST PMT-04 include,

- GSTIN

- Legal Name

- Ledger where the discrepancy is noted

- Type of tax in which discrepancy is noticed

- Type of discrepancy

- Amount of discrepancy

- Reasons, if any for the discrepancy

Electronic Credit Ledger on GST Portal

Here are the steps to view an Electronic Credit Ledger in the GST Portal.

Step 1: Log in to the Portal The taxpayer has to login to the official GST Portal. Step 2: Enter the Details The taxpayer has to enter the username and password. Step 3: Click Electronic Credit Ledger From the ‘Services’ tab, click ‘Ledgers’ and then select ‘Electronic Credit Ledger’ command. Step 3-Gst Electronic Credit Ledger

The page is displayed along with the credit balance as per the present date.

Step 3-Gst Electronic Credit Ledger

The page is displayed along with the credit balance as per the present date.

Step 3-Gst Electronic Credit Ledger

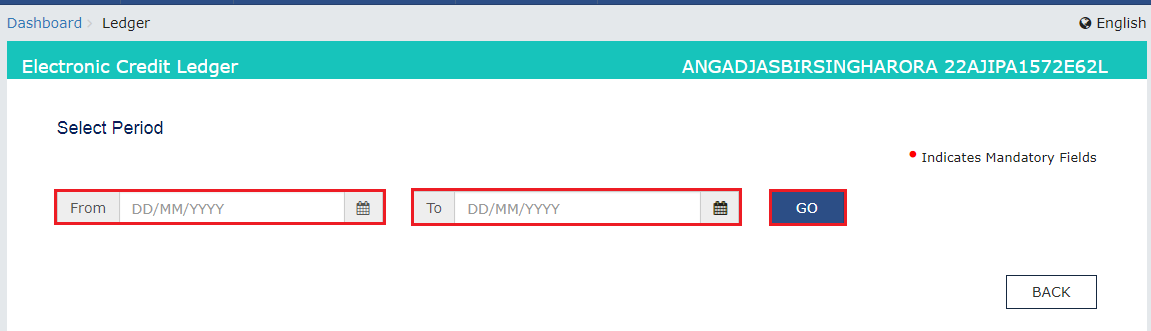

Step 4: Select the Time Period

The taxpayer using the calendar has to select the ‘From’ and ‘To’ date for which the taxpayer desires to view the transactions of the Electronic Credit Ledger.

Step 5: Click GO

Once this is completed, the taxpayer has to click the ‘Go’ button. The Electronic Credit Ledger details are displayed.

Step 3-Gst Electronic Credit Ledger

Step 4: Select the Time Period

The taxpayer using the calendar has to select the ‘From’ and ‘To’ date for which the taxpayer desires to view the transactions of the Electronic Credit Ledger.

Step 5: Click GO

Once this is completed, the taxpayer has to click the ‘Go’ button. The Electronic Credit Ledger details are displayed.

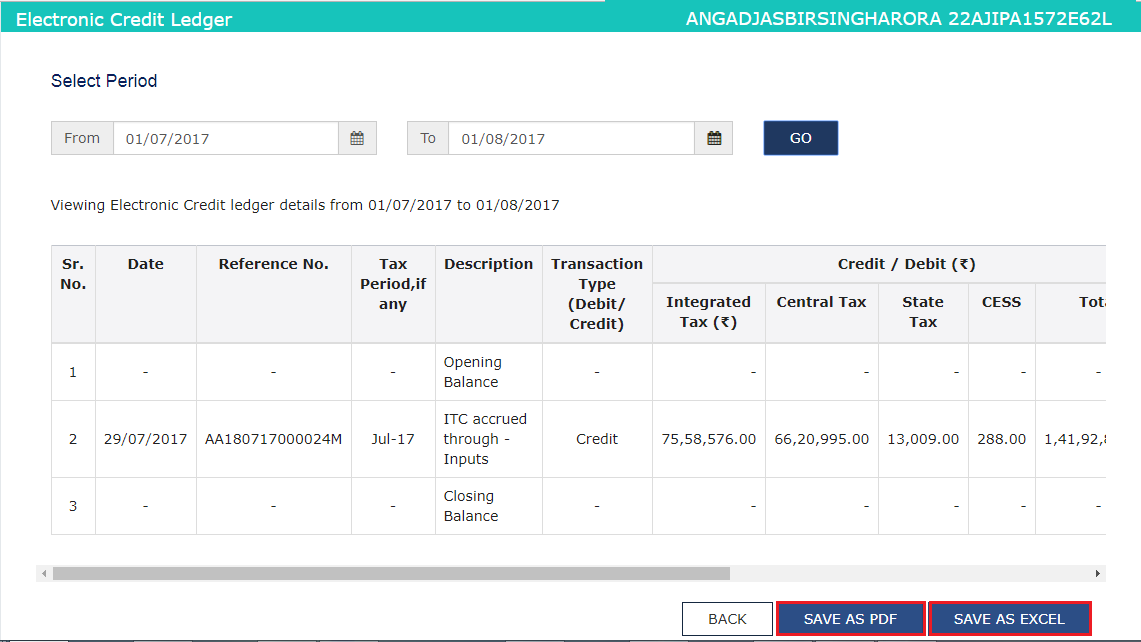

Step 6-Gst Electronic Credit Ledger

Step 6: Click Save

The taxpayer has to either click on ‘Save as PDF’ or ‘Save as Excel’ button to save the Electronic Credit Ledger.

Step 6-Gst Electronic Credit Ledger

Step 6: Click Save

The taxpayer has to either click on ‘Save as PDF’ or ‘Save as Excel’ button to save the Electronic Credit Ledger.

- By clicking the ‘Save as PDF’ button, the Portal saves the Electronic Credit Ledger file in the PDF format.

- By clicking the ‘Save as Excel’ button, the Portal saves the Electronic Credit Ledger file in the excel format

Step 6-Gst Electronic Credit Ledger

Step 6-Gst Electronic Credit Ledger

Utilization of the Cash

The cash available in the Electronic Credit Ledger can be utilized for paying off tax liabilities as per the below rules. However, the following describes making the first payment:

- ITC of IGST: Used for payment of IGST output tax liability, The taxpayer may utilize the balance for making CGST and SGST payments.

- ITC of CGST: Used for payment of CGST output tax liability. Then the taxpayer may utilize the balance for making IGST payment.

- The ITC of SGST: Used for payment of SGST output tax liability and then the balance can be used for payment of IGST.

- ITC of CESS: Used only against CESS tax liability. CESS credit is not available for cross-utilization with other tax liabilities.

Balance Check

A taxpayer can check the balance on the landing page of the Electronic Credit Ledger by clicking on the ‘Service’ tab, the ‘Ledgers’ option and then click on the ‘Electronic Credit Ledger’.

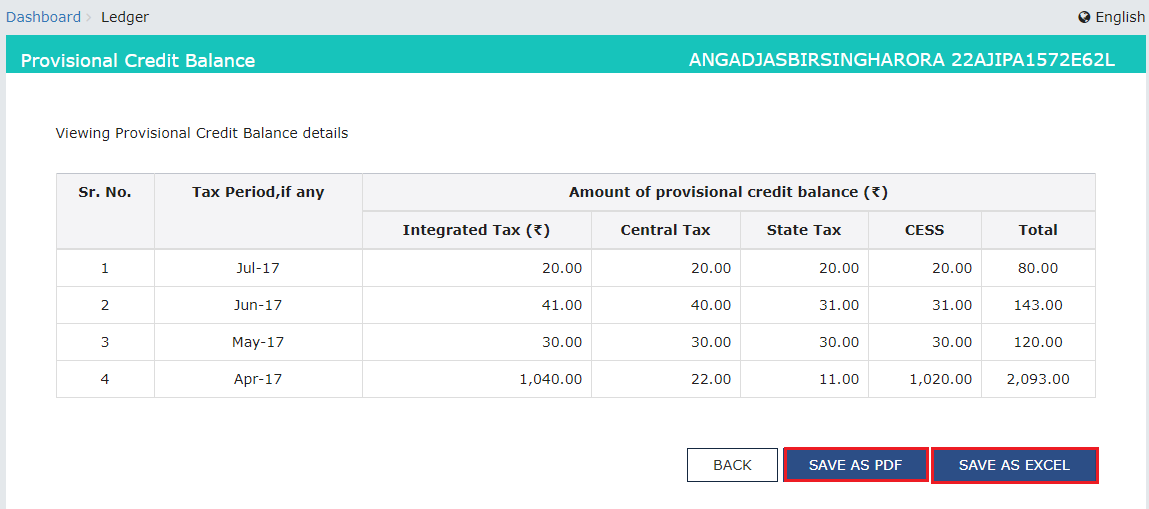

Provisional Credit Balance

The provisional credit tables display the balance of provisional and mismatch credit, tax period wise. To access this, the taxpayer has to click on the ‘Servies’ tab, ‘Ledgers’ option, ‘Electronic Credit Ledger’ and then the ‘Provisional Credit Balance’ link to view it.

Viewing Procedure

The taxpayer shall use the following procedure for viewing Provisional Credit Balance:

Step 1: Log in to the Portal The taxpayer has to login to the official GST Portal. Step 2: Enter the Details The taxpayer has to enter the username and password. Step 3: Click Electronic Credit Ledger From the ‘Services’ tab, click ‘Ledgers’ and then select ‘Electronic Credit Ledger’ command. Step 4: Click Provisional Credit Balance The taxpayer has to click the ‘Provisional Credit Balance’ link. The Portal displays the provisional Credit Balance on the screen. Step 5: Click Save The taxpayer has to either click on ‘Save as PDF’ or ‘Save as Excel’ button to save the Provisional Credit Balance.- By clicking the ‘Save as PDF’ button, the Portal saves the Provisional Credit Balance file in the PDF format.

- By clicking the ‘Save as Excel’ button, the Portal saves the Provisional Credit Balance file in the excel format.

Step 5- Gst Electronic Credit Ledger

Step 5- Gst Electronic Credit Ledger

Blocked Credit Balance

For authentication purposes, a Jurisdiction Officer can examine the ITC's amount claimed by the taxpayer through GST TRAN-1, GST TRAN-2 and other related forms. The concerned Jurisdiction Officer decides to temporarily block the ITC that is available to a taxpayer when there is a requirement of further investigation in the revenue. The officer may completely or partly block CGST, SGST, IGST and Cess balance. After the investigation, the concerned officer unblocks the ITC that was previously blocked. The taxpayer will be notified through an email and SMS while blocking and unblocking of ITC.

Viewing Blocked Credit Balance

The taxpayer shall use the following procedure to view Blocked Credit Balance:

Step 1: Log in to the Portal The taxpayer has to login to the official GST Portal. Step 2: Enter the Details The taxpayer has to enter the username and password. Step 3: Click Electronic Credit Ledger From the ‘Services’ tab, click ‘Ledgers’ and then select ‘Electronic Credit Ledger’ command. Step 4: Click Blocked Credit Balance The taxpayer has to click the ‘Blocked Credit Balance’ link. The Portal displays the Blocked Credit Balance on the screen. Step 5: Click Save The taxpayer has to either click on ‘Save as PDF’ or ‘Save as Excel’ button to save the Blocked Credit Balance.- By clicking the ‘Save as PDF’ button, the Portal saves the Blocked Credit Balance file in the PDF format.

- By clicking the ‘Save as Excel’ button, the Portal saves the Blocked Credit Balance file in the excel format.

Step 5- Gst Electronic Credit Ledger

Step 5- Gst Electronic Credit Ledger