IndiaFilings

Expert

Published on: Apr 22, 2026

GST Credit Transfer Document

The Ministry of Finance introduced the concept of Credit Transfer Document (CTD) in Goods and Services Tax (GST) to transfer CENVAT credit paid on specified goods available with a trader on the GST implementation date. The manufacturer can issue a CTD through TRANS 3 through the GST portal. In this article, let us look at the GST Credit Transfer Document in detail.

Who can issue the GST Credit Transfer Document?

A manufacturer registered under Central Excise can issue Credit Transfer Document to evidence payment of central excise duty for goods manufactured and cleared by the concerned individual before the date of GST implementation. In addition, the manufacturer shall issue CTD to an unregistered person under Central Excise with the cover of an invoice but registered under

GST.Criteria for Issuing Credit Transfer Document

Upon issuing the GST Credit Transfer Document, the issuing authority should follow the following limitations, conditions and procedures:

- For the value of such goods higher than Rs.25,000 per piece, the goods shall bear the brand name of the manufacturer or the principal manufacturer and shall identify using a distinct number such as chassis/engine number of the vehicle.

- The manufacturer should maintain the verifiable records of clearance and payments related to duty of each piece of such goods and make available for verification on demand by a Central Excise officer.

- The issuer shall use the serial number system when issuing CTD. It should contain the following details of the receiver:

- Central Excise registration number,

- Address of the concerned Central Excise Division,

- Name, address and GSTIN number of the person,

- Description,

- Classification,

- Invoice number with date of removal,

- Mode of transport and vehicle registration number,

- Rate of duty, quantity,

- Value and duty of central excise and

- The total amount paid.

Availing Credit

- A dealer availing credit using Credit Transfer Document on manufactured goods would not be eligible to avail credit under GST Transition Rules made under CGST Act, 2017 on identical goods manufactured by the same manufacturer available in the stock of the dealer.

- The dealer availing credit on the basis of CTD should, at the time of making a supply of such goods, mention the corresponding CTD number in the invoice issued by him.

Misuse of Credit Transfer Document

If a manufacturer issues a CTD and the credit of central tax is availed twice on the same goods, then the manufacturer would be jointly and severally responsible for excess credit availed by the dealer and provisions for recovery of credit, interest and penalty under the CENVAT Credit Rules would apply on the manufacturer.

Procedure for Issuing Credit Transfer Document

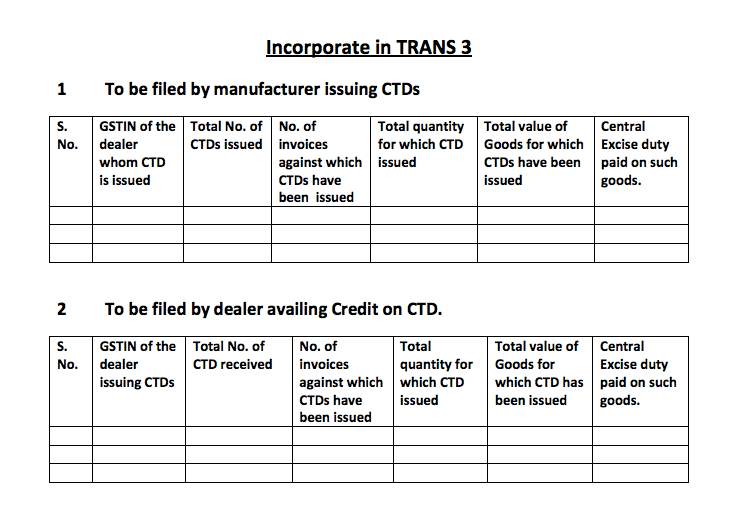

A manufacturer issuing a Credit Transfer Document should submit details in TRANS 3 on GST common portal within sixty days of the appointed date. A dealer availing credit on CTD should submit details in TRANS 3 on the common portal within sixty days of the appointed date.

GST Form TRAN 3

All manufacturers issuing CTD shall maintain the records in form TRANS 3A and the concerned authority shall produce all the records to the Central Excise officer for verification on demand.

Dealers availing credit on CTD should maintain the record in the form TRANS 3B, and the record should be made available to the Central Excise officer for verification on demand.

GST Form TRAN 3

All manufacturers issuing CTD shall maintain the records in form TRANS 3A and the concerned authority shall produce all the records to the Central Excise officer for verification on demand.

Dealers availing credit on CTD should maintain the record in the form TRANS 3B, and the record should be made available to the Central Excise officer for verification on demand.