RENU SURESH

Expert

Published on: Aug 11, 2026

Old Regime vs New Regime 2025: Which Tax Regime is Better for You?

The Union Budget 2025 has brought significant changes to India’s personal income tax structure, raising the question: “Should you opt for the old tax regime versus the new tax regime?” Whether you’re a salaried professional or a self-employed individual, making the right choice between the old regime vs new regime can help optimise your overall tax liability. This in-depth article explores the new tax regime vs the old tax regime slabs, highlights the latest income tax slabs, and offers key insights to help you decide which tax regime is better for you.

If you need expert guidance in navigating these changes, IndiaFilings can provide personalized tax planning and hassle-free ITR filing services tailored to your requirements.

New Regime vs Old Regime: Which is Better After Budget 2025?

With Finance Minister Nirmala Sitharaman’s Union Budget 2025 offering a significant income tax relief—particularly no tax burden up to ₹12.75 lakh—a large segment of the middle class has plenty to celebrate. However, this shift has also led to a key question for salaried taxpayers: Should you move to the new regime, or do the higher deductions and exemptions available under the old regime still offer better overall savings?

All the noteworthy changes to income tax slabs and rates for FY 2025–26 have been introduced in the new tax regime. Hence, the dilemma revolves around whether the new system genuinely benefits you more than the traditional one. According to EY, the most straightforward approach is to total up the exemptions and deductions you can claim under the old regime before deciding which option yields the lowest overall tax liability.

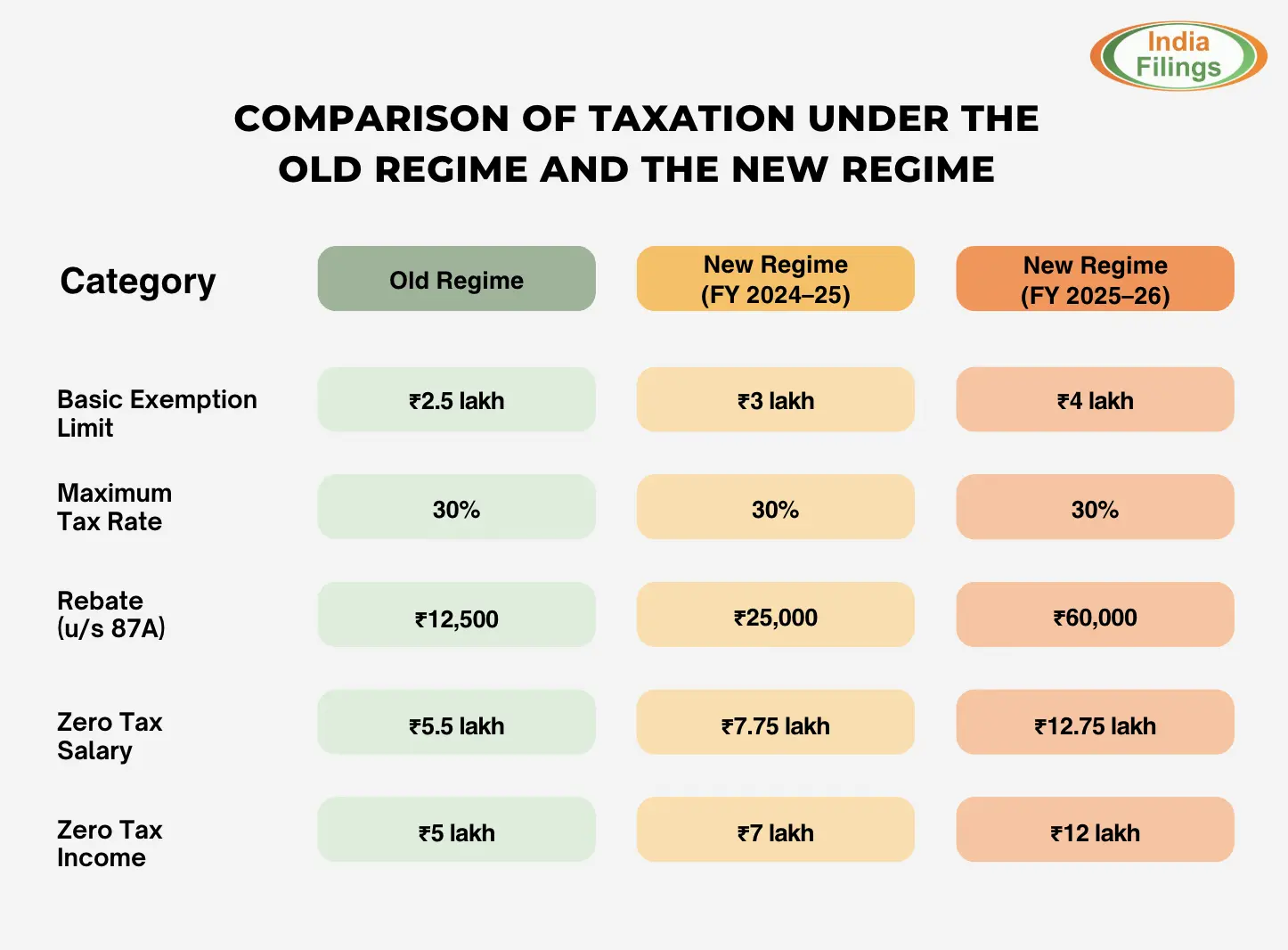

Key Highlights of the Union Budget 2025

- Zero Tax Up to ₹12.75 Lakh (Salaried Under New Regime)

- Under the new tax regime, the basic exemption limit has gone up to ₹12 lakh for all individuals.

- Salaried taxpayers get a ₹75,000 standard deduction, effectively making ₹12.75 lakh income tax-free.

- New Income Tax Slab Rates: The new tax regime now has seven slabs, starting with 0% for income up to ₹4 lakh and rising to 30% for income above ₹24 lakh.

- Old Income Tax Slabs Unchanged: The old tax regime slabs continues with its standard slabs:

- 0% up to ₹2.5 lakh

- 5% from ₹2.5 lakh to ₹5 lakh

- 20% from ₹5 lakh to ₹10 lakh

- 30% above ₹10 lakh

- Minimal Deductions in the New Regime: The new regime largely eliminates conventional tax exemptions and deductions such as HRA, LTA, Section 80C (for investments), and Section 80D (medical insurance). The primary offset is the standard deduction of ₹75,000 for salaried individuals.

Also read: Budget 2025: Rationalisation of certain provisions of Income Tax Act

New Tax Regime Slabs - Income Tax Slabs (FY 2024–25)

Under the new tax regime, the slabs are structured to offer lower rates across broader income brackets:

Income Range (₹) | Tax Rate |

0 – 4 lakh | 0% |

4 – 8 lakh | 5% |

8 – 12 lakh | 10% |

12 – 16 lakh | 15% |

16 – 20 lakh | 20% |

20 – 24 lakh | 25% |

Above 24 lakh | 30% |

Note: Salaried individuals enjoy an additional ₹75,000 standard deduction, effectively raising their zero-tax threshold to ₹12.75 lakh.

Old Tax Regime Slabs - Income Tax Slabs (FY 2024–25)

The old tax regime retains its traditional slabs:

Income Range (₹) | Tax Rate |

0 – 2.5 lakh | 0% |

2.5 – 5 lakh | 5% |

5 – 10 lakh | 20% |

Above 10 lakh | 30% |

Note: Under the old regime, taxpayers can still avail of popular deductions (like 80C, 80D, HRA, etc.), whereas the new regime permits fewer exemptions/deductions but provides broader tax slabs and higher exemption thresholds for many.

New and Old Tax Regime Slabs: A Quick Comparison

To better understand which is better—the old tax regime versus the new tax regime—let’s look at the core differences:

Criteria | Old Tax Regime | New Tax Regime (Budget 2025) |

Basic Exemption Threshold | ₹2.5 lakh | ₹12 lakh (₹12.75 lakh for salaried) |

Tax Slabs | 5%, 20%, 30% beyond their thresholds | 0%, 5%, 10%, 15%, 20%, 25%, 30% across broader slabs |

Deductions/Exemptions | HRA, LTA, 80C, 80D, interest on home loan, etc. allowed | Limited (only standard deduction of ₹75k for salaried) |

Compliance & Documentation | High (investment proofs, rent receipts, etc.) | Low (fewer claims mean simpler filing) |

Ideal For | Taxpayers with large deductions & exemptions (≥ ₹5–8 lakh) | Those with limited deductions or preferring simplified slabs |

Old Tax Regime Slabs: Structure and Benefits

Income Tax Slabs Unchanged

- Up to ₹2.5 lakh: 0%

- ₹2.5 lakh – ₹5 lakh: 5%

- ₹5 lakh – ₹10 lakh: 20%

- Above ₹10 lakh: 30%

Large Scope for Deductions

- Section 80C: Up to ₹1.5 lakh (for investments in PPF, ELSS, life insurance, etc.)

- Section 80D: Health insurance premium for self and family

- HRA: House rent allowance exemption if you live on rent

- LTA: Leave travel allowance exemption (subject to rules)

- Interest on Home Loan: Deduction up to ₹2 lakh for self-occupied property

- And more (80CCD for NPS contributions, 80G for donations, etc.)

Benefits of Old Tax Regime: Who Benefits Most from the Old Tax Regime?

Those With High Deductions

If you can claim significant deductions—for instance, ₹5–8 lakh or more—through HRA, 80C, 80D, and home loan interest, then the old regime may reduce your taxable income enough to offset the higher tax rates.

Mid-Range Income Earners (₹12L – ₹24L)

- If your total exemptions (HRA, LTA) and deductions (80C, 80D, home loan) are substantial, the old regime could still be beneficial.

- For many in the ₹12 lakh to ₹20 lakh range, the break-even heavily depends on how much they invest in tax-saving instruments.

Who Should Consider the Old Regime?

- Mid to higher earners who can exhaust multiple deductions (often ₹5 lakh or more in total) may still find the old regime cheaper.

- Salaried individuals with substantial HRA (especially in metro cities) or big home-loan interest outgo.

New Tax Regime - Budget 2025

Raised Zero-Tax Limit

- 0% tax on incomes up to ₹12 lakh.

- Salaried taxpayers enjoy an additional standard deduction of ₹75,000, effectively making incomes up to ₹12.75 lakh tax-free.

Updated Slabs

- 0%: Up to ₹4 lakh

- 5%: ₹4 – 8 lakh

- 10%: ₹8 – 12 lakh

- 15%: ₹12 – 16 lakh

- 20%: ₹16 – 20 lakh

- 25%: ₹20 – 24 lakh

- 30%: Above ₹24 lakh

Minimal Deductions

Apart from the standard deduction for salaried taxpayers, most traditional exemptions (HRA, LTA) and common deductions (80C, 80D) are not available.

Who Should Consider the New Regime?

Salaried individuals up to ₹12.75 lakh who want a zero-tax liability.

- People who cannot (or prefer not to) invest large sums in instruments like PPF, ELSS, or insurance solely to save tax.

- High-income earners whose total deductions (excluding the standard deduction) are relatively modest—especially if under ~₹8 lakh in the old regime (according to many tax experts).

Benefits of Old Tax Regime: Who Benefits Most from the New Tax Regime?

Salaried Individuals Up to ₹12.75 Lakh

- No tax for incomes up to ₹12.75 lakh.

- Ideal for those who do not or cannot utilise large deductions under the old system.

High-Income Earners with Limited Deductions

- Even above ₹24 lakhs, the new regime can be beneficial if you’re not claiming big exemptions (e.g., no major HRA, no large housing loan, or no big 80C investments).

Preference for Simplicity

- Minimal documentation; no need to submit multiple proofs of investment or rent.

- Straightforward slabs and lower rates for those with fewer financial commitments.

Income Tax Old Regime vs New Regime 2025: Example Scenarios

Income = ₹13 Lakh (Salaried)

- New Regime: Likely zero or very minimal tax after the standard deduction (₹75,000) since ₹12.75 lakh is tax-free.

- Old Regime: Could match or beat new regime only if you have large deductions (e.g., total ≥ ₹2–3 lakh in 80C, HRA, etc.).

Income = ₹20 Lakh

- New Regime: Tax rates from 16–20 lakh = 20%, and you only get ₹75,000 as a standard deduction.

- Old Regime: If you have substantial deductions (HRA, 80C, 80D, home loan), you may drive your taxable income down into a lower tax bracket.

Incomes Up to ₹12–13 Lakh

- Under the new regime, there is effectively no tax up to ₹12 lakh (₹12.75 lakh for salaried).

- In the old regime, you would need significant exemptions (like HRA or 80C + 80D) to reduce your taxable income to effectively zero—often a tough benchmark to beat.

- For most in this bracket, the new regime is simpler and often yields zero or minimal tax.

Incomes Around ₹15–20 Lakh

- If you invest heavily (HRA, 80C, 80D, interest on housing loan), the old regime might match or outperform the new regime. For instance, some mid-tier earners can reduce their taxable income drastically if they max out 80C (₹1.5 lakh), pay substantial rent (HRA exemption), and have home-loan interest deductions.

- If your total deductions are modest (say under ₹5 lakh), the new regime is typically simpler and can be cheaper.

Incomes Above ₹24–25 Lakh

- Many experts note that if your total deductions (excluding standard deduction) are under ₹8 lakh, the new regime tends to yield a lower tax liability.

- If you can stack up large deductions—HRA, 80C, home loan interest, etc.—beyond ₹8 lakh, you may still find the old regime helpful. However, it requires significant financial outflows toward rent or loan EMIs plus strategic investments.

Illustrative Example - Above ₹24 Lakh Income: Old Tax Regime versus New Tax Regime

- Gross Salary (A): ₹35,00,000 (₹3,500,000)

- Deductions and Exemptions (B): Varied scenarios (e.g., HRA, LTA, 80C, 80D, interest on housing loan)

- Standard Deduction (C):

- Old Regime: ₹50,000

- New Regime: ₹75,000

When you apply different levels of total deductions/exemptions—from ₹5.75 lakh to ₹9.5 lakh—the final tax liability changes. Once your deductions exceed ₹8 lakh, the old regime may offer more savings.

- Old Regime: Potentially lower taxable income (after subtracting HRA, LTA, 80C, interest on home loan, etc.).

- New Regime: Higher standard deduction of ₹75,000 but fewer overall deductions or exemptions allowed.

In the example calculations:

- When total deductions/exemptions are below ₹8 lakh, the new regime’s final tax tends to be lower.

- As deductions climb to or beyond ₹8 lakh, the old regime may yield a reduced tax liability.

Illustrative Examples - Below ₹24 Lakh Income: New and Old Tax Regime

The second example shows scenarios for gross salaries of:

- ₹14 lakh

- ₹18 lakh

- ₹22 lakh

In each case, various deductions (HRA, LTA, 80C, 80D) reduce the taxable income under the old regime, while the new regime allows only the standard deduction. These calculations reveal:

At ₹14 lakh:

- If you have significant exemptions (e.g., HRA of ₹2.3 lakh, LTA of ₹25,000, etc.), the old regime’s final tax might be slightly higher or lower depending on how much you deduct.

At ₹18 lakh or ₹22 lakh:

- As total exemptions/ deductions grow, the old regime can sometimes reduce taxable income enough to offset higher slab rates.

- The new regime, however, might still be simpler and cheaper if your deductions are relatively small.

In the example calculations:

A taxpayer with a gross salary of ₹14 lakh, claiming about ₹4.55 lakh in deductions/exemptions under the old regime, ends up with a taxable income of ₹8.95 lakh. Comparatively, under the new regime, the taxable income is higher (₹13.25 lakh), but the tax rates are lower.

The exact “benefit or loss” under the old regime varies with each scenario, reflecting how your personal mix of deductions influences the final result.

Click here to visit the TAX CALCULATOR – OLD REGIME VIS-À-VIS NEW REGIME

Key Takeaway: Income Tax Old Regime vs New Regime

- For salaried individuals with gross income above ₹24.75 lakhs, the new tax regime is generally more beneficial only if their total deductions and exemptions (those not permitted under the new regime) are below ₹8 lakhs (excluding the standard deduction).

- Conversely, if these deductions and exemptions exceed ₹8 lakhs, then the old tax regime might still result in a lower overall tax outgo.

- This break-even threshold of ₹8 lakhs specifically applies to incomes in the 30% tax bracket (i.e., above ₹24 lakhs or ₹24.75 lakhs when factoring in the standard deduction). For lower income levels, the corresponding break-even point will be different.

The exact break-even depends on how many deductions you can claim. It may require testing both regimes to see which yields the lower tax.

Overall, the best approach is to itemise your allowable deductions and exemptions carefully under the old regime, compare that final taxable figure and tax outgo with the new regime, and then choose the option that leads to maximum net savings.

Deciding Factors: Old Regime vs New Regime

- Magnitude of Deductions: The new and old tax regimes differ primarily in how they handle exemptions and deductions. The more you can claim, the stronger the case for the old regime.

- Record-Keeping & Compliance: The old regime requires more paperwork, while the new regime is nearly documentation-free.

- Financial Goals & Liquidity: Many old regime deductions (like 80C) lock your money into long-term investments (PPF, ELSS, etc.). If you prefer liquidity or simpler finances, the new regime may be easier.

- Annual Reevaluation: You can opt for either regime each financial year (with some constraints for business income). Always do a side-by-side calculation because your finances—and tax laws—can change over time.

Which Tax Regime is Better for You?

Choosing between the old and new tax regimes largely depends on your individual financial profile, deductions, and investment habits. Here are some key points to help you decide which tax regime is better for you:

Available Deductions and Exemptions

- Old Regime: You can claim deductions and exemptions like HRA, LTA, 80C (Investments), 80D (Health Insurance), etc.

- New Regime: Most exemptions and deductions are removed, but tax rates and income slabs may be more favourable.

Income Level and Slab Rates

- Check the tax slab rates in both regimes. The new regime may have more income slabs but lower rates.

- Compare your tax outflow by actually calculating potential savings under each regime.

Type of Income

- If your income is mainly salary and you rely heavily on exemptions (e.g., House Rent Allowance), the old regime might help minimize your tax burden.

- If you have fewer exemptions to claim—or do not want to invest in tax-saving instruments—the new regime can be simpler and may result in lower taxes.

Standard Deduction Differences

- Under the Budget 2025 proposals, the old regime provides a standard deduction of ₹50,000 (for salaried), whereas the new regime offers ₹75,000.

- This alone might make the new regime more attractive if your other exemptions aren’t as significant.

Long-Term Financial Planning

- If you already invest in 80C avenues (e.g., Provident Fund, ELSS), the old regime can reward you with deductions you’ve been using.

- If you prefer flexibility and do not want mandatory investments for tax benefits, you might find the new regime more convenient.

Calculate Both Scenarios

The best way to decide is to compute your approximate tax under both regimes using your actual income, possible deductions, and the relevant slab rates. Whichever yields a lower overall liability is generally the better choice.

Tip: Each financial year, do a quick calculation of your projected income and deductions at the start of the year (or before filing your tax return). This ensures you pick the regime that aligns with your current financial situation.

Conclusion

Ultimately, the decision between the old and new tax regimes depends on your individual circumstances—your income level, the size of your eligible deductions, and your long-term financial objectives. While the old regime can be advantageous for those who benefit substantially from exemptions like HRA, LTA, or 80C investments, the new regime’s higher exemption limits and simplified slabs may be ideal for taxpayers seeking minimal documentation and compliance. It’s wise to recalculate your liabilities at the start of each financial year, comparing both regimes with your current deductions, to ensure you consistently choose the approach that offers the maximum net savings.

Ready to simplify your Section 80C Detailsand ensure you choose the most beneficial regime? Let IndiaFilings tax experts guide you through the process with expert advice, personalised assistance, and seamless online filing.

Contact our experts today to secure the best possible tax outcome for your financial goals!