Marlin Priya

Expert

Published on: Apr 21, 2026

Madhya Pradesh Property Tax

Property tax is a levy imposed by the Government that the property owner is liable to pay on his/her real or personal property. The concerned governing authority of the jurisdiction where the property is located will assess the value of the property and levy the tax. The types of properties taxed and the property tax rates differ by jurisdiction. The Revenue section of the Municipal body is responsible for the administration of the property taxation for the respective urban local bodies. It is important to pay the property tax on time to avail tax benefits and avoid legal hassles. In this article, we look at the various aspects of Madhya Pradesh property tax in detail.

Purpose

Property Tax is one of the main sources of revenue for the Urban Local Bodies (ULB) in Madhya Pradesh. The local governing body will assess the property and collects the property tax. The collected taxes are used for the jurisdiction in which the property is situated. The services for which the collected money are used include education, library construction, sewer improvements, road and highway constructions, repairing roads, fire service and other services that highly benefit the concerned jurisdiction.

The Madhya Pradesh Municipal Corporation Act, 1956

Section 135 under the Madhya Pradesh Municipal Corporation Act, 1956 deals with the imposition of property tax and includes the provisions for the assessment method of lands and buildings and the collection for property tax. The act incorporates the properties liable for property tax, the tax rates, properties exempted from the levy of the property tax etc.

Properties Liable for Madhya Pradesh Property Tax

All residential and commercial (non-residential) properties located within the limits of urban local bodies in Madhya Pradesh are assessed for tax. Based on such assessments, taxes are levied on the property owners. However, the residential buildings for which the Annual Rental Value of the property tax is below Rs.6000 for the Municipal having a population less than one lakh are exempted from property tax. The information about all the new constructions, existing construction and improvements to the property must be provided to the Town Planning Department to make necessary changes to tax assessment.

Property Tax Components

As per section 135 of the Madhya Pradesh Municipal Corporation Act, the council determines the tax be levied on all buildings and lands within the limits of the Municipal that includes the following components.

- water and drainage tax

- scavenging tax.

- lighting tax

- tax for the general purpose

Responsible Persons

As per the Act, the following personnel will be responsible for paying the Madhya Pradesh Property Tax.

- The owner or joint owners

- The lessor - if the land or building is let for lease

- The superior lessor - if the land or building is sub-let

- If the property is not let out, the person who has the right to let is responsible for paying the tax.

If the above-mentioned person fails to pay the tax, the occupier of the building will be charged.

Properties Exempted from Tax

Under section 135, the Madhya Pradesh property tax is not leviable for the following properties. a) Buildings and lands owned by the following but not leased or rented out.

- The Union Government

- The State Government

- The Corporation

b) Agricultural land and building other than the residing house. c) Buildings and lands or a part of it used solely for educational purposes that include schools, boarding houses, hostels and libraries without payment of any rent d) Vacant land and building occupied exclusively for public worship, for charity purposes with the approval of corporation, for public burial or as a cremation ground. Inherited land or buildings that are used for the above-mentioned premises are also notified for tax exemption. e) Land or building owned by the widows, abandoned, minor, physically or mentally disabled. Such exemptions are subjected to twelve thousand rupees or the annual value of such buildings and lands. f) Buildings or lands where any business or trade is carried on will be tax-exempted if the rent derived from such property is exclusively utilized for public charitable institutions or religious purposes. g) One personal residential property owned by the employees or the officers of Municipal Corporation of Madhya Pradesh who are completely handicapped during duty hours is tax-exempted. h) Property owned by a political party in the State that the Election Commission of India has recognized. i) One residential property owned by the following are also exempted from property tax.

- Gallantry award winners in Police, Defense Forces, and Paramilitary Forces

- Civilians who have received the highest order of bravery awards from the Government

- Armed force personnel who have sustained disability between 76 to 100 percent in war or war-like operations.

Discount of Property Tax

As per section 135 of the Madhya Pradesh Municipal Corporation Act, 1956, a rebate of 6.25 per cent is allowed for the taxpayers who make the property tax payment on time before the due date.

Payment of Madhya Pradesh Property Tax

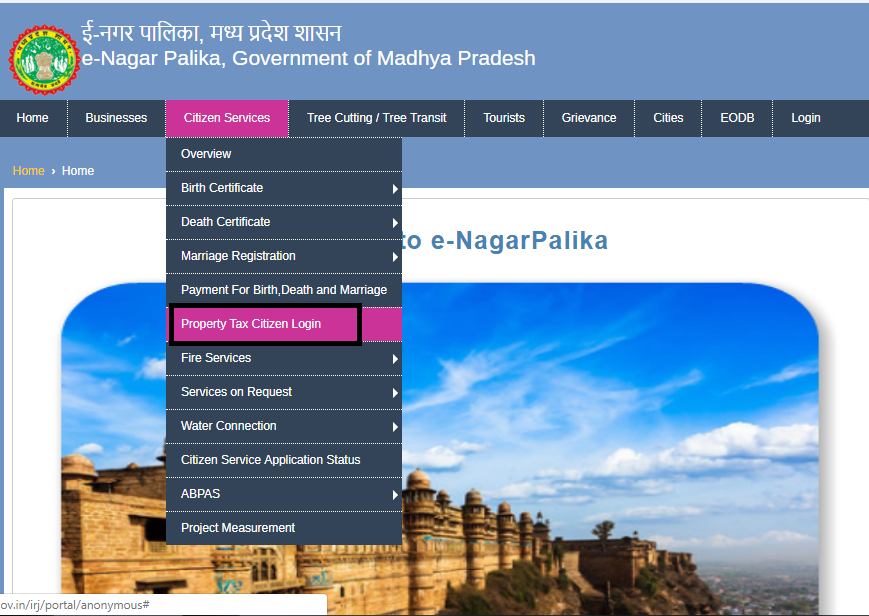

Step 1: The taxpayer can make the property tax payment online by visiting the official website of e-Nagar Palika of Madhya Pradesh. Step 2: Under the tab citizen services, select ‘Property Tax Citizen Login’. Madhya Pradesh Property Tax - Citizen services

Clicking it will redirect to the property tax payment login.

Madhya Pradesh Property Tax - Citizen services

Clicking it will redirect to the property tax payment login.

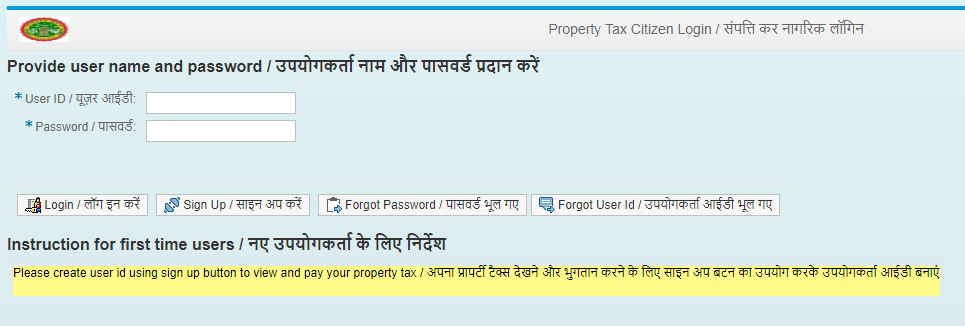

Madhya Pradesh Property Tax - Login

Step 3: Online tax calculation can be done by providing the details such as the name of the owner, ownership category, use of the property, address etc.

Step 4: Enter the other required details and make the necessary payment.

To check the payment status before payment, click on ‘View Demand/Payment Status’ under property tax services. Fill all the details and click on the “Search” button. In the screen that appears, check the assessment Details, Demand Details and Payment Details.

Step 5: Print the receipt after making the required payment.

Madhya Pradesh Property Tax - Login

Step 3: Online tax calculation can be done by providing the details such as the name of the owner, ownership category, use of the property, address etc.

Step 4: Enter the other required details and make the necessary payment.

To check the payment status before payment, click on ‘View Demand/Payment Status’ under property tax services. Fill all the details and click on the “Search” button. In the screen that appears, check the assessment Details, Demand Details and Payment Details.

Step 5: Print the receipt after making the required payment.