IndiaFilings

Expert

Published on: Apr 22, 2026

Job Work under GST - Comprehensive Guide

A significant group of

MSME businesses in India are involved in the job work sector, providing outsourced manufacturing services. Job work is a type of outsourced service, wherein goods are manufactured or processed using goods supplied by the principal. Thus, under a job work, the principal manufacturer sends inputs or semifinished goods to a job worker for further processing. In this article, we look at the treatment and definition of job work under GST.GST Definition for Job Work

Section 2(68) of the CGST Act, 2017 defines job work as ‘any treatment or process undertaken by a person on goods belonging to another registered person’. The one who does the said job would be termed as ‘job worker’. The ownership of the goods does not transfer to the job-worker but it rests with the principal. The job worker is required to carry out the process specified by the principal on the goods.

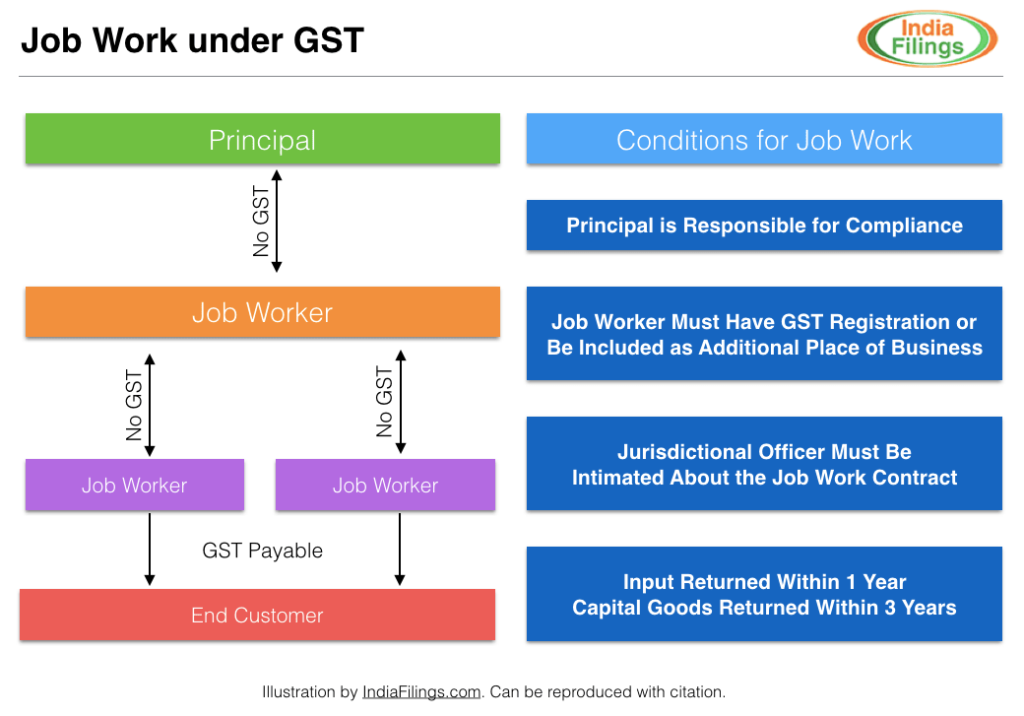

GST on Job Work

Job work provisions already existed under Central Excise, VAT and Service Tax regulations. Under these regulations, concession was given to the job workers (often times a micro, small or medium business) and the principal was made responsible for tax compliance on behalf of the job worker. Under GST as well, special provisions have been provided for removal of goods for job-work and receiving back the goods after processing from the job-worker without the payment of GST. The benefit of these provisions shall be available both to the principal and the job worker.

GST Registration for Job Work

Job contract can be initiated by a principal with a third-party job work service provider by declaring the premises of the job worker as additional place of business in the

GST registration. In case the job worker is already registered under GST, then declaring the premises of the job worker under additional place of business is not required.Conditions for Job Worker under GST

Once the GST registration aspect is complete, the principal must submit to the Jurisdictional Officer, details of the description of inputs intended to be sent by the principal and the nature of processing to be carried out by the job-worker. Then, the principal can send goods for further processing or capital goods to the job worker under the cover of challan issued by the principal. Challan must be issued by the principal even for inputs and capital goods directly send to the job-worker. Job work challan must conform to the

GST invoice rules and the responsibility for keeping proper accounts as per GST requirements would lie with the principal. All inputs must be returned to the principal within one year and capital goods must be returned with three years after processing by the job worker. However, the condition of return of goods for job work is not applicable in case of moulds and dies, jigs and fixtures or tools supplied by the principal to job worker.GST on Job Work

Illustration for Job Work under GST

Job work contract satisfying the above conditions enjoy special concessions as under:

Illustration for Job Work under GST

Job work contract satisfying the above conditions enjoy special concessions as under:

- Principal can send inputs/ capital goods without payment of tax to a job worker.

- The job worker after completing the job work can send the principal's goods from there to another job worker for additional processing and after completion of job work bring back such goods without payment of tax.

- Principal is not required to reverse the input tax credit availed on inputs or capital goods dispatched to job-worker.

- Principal can send inputs or capital goods directly to the job worker without bringing them to his premises and can still avail the credit of tax paid on such inputs or capital goods.

If the job work does not satisfy the conditions and intimation requirement for job work, then

GST rate as applicable for job work must be paid by the job worker.Input Tax Credit for Job Work

Under GST, the principal is allowed to take

input tax credit on goods supplied to the job worker. Also, the principal can take input tax credit on inputs / capital goods directly supplied to the job worker even without the goods being brought into the premise of the principal.GST Transition for Job Work Contract

On 1st July, 2017, GST was implemented in India. Transitional provision has been provided for input or goods transferred under job work contract prior to the implementation of GST in India. All principal who have sent goods to job worker before 1st July, 2017 are required to file GST TRAN-1 within 90 days of 1st July 2017 with details of such goods sent/received for job-work. Under the GST transitional provision for job work, inputs which are sent to a job-worker prior to introduction of GST would not attract GST, if the goods are returned to the principal by the job worker before 31st, December 2017. If goods sent to a job worker are not returned to the principal before 31st December 2017, then input tax credit availed on the goods will be liable to be recovered.

Read more about GST in India at the GST Portal. You can file your GST returns using LEDGERS GST Accounting Software.