IndiaFilings

Expert

Published on: Jun 24, 2026

GST Accounts and Record Maintenance Procedure

After the implementation of Goods and Services Tax (GST), all the businesses started to follow the GST accounts and record maintenance procedure. One of the primary reasons to follow the GST accounting procedure as the process completely depends on technology. In addition, all multiple taxations shifted to a single taxation process. Under the new GST regime, businesses should maintain various accounts and records for ready verification by an authorized GST Authority. This article describes the necessary GST accounts and records to be maintained by all businesses operating in India.

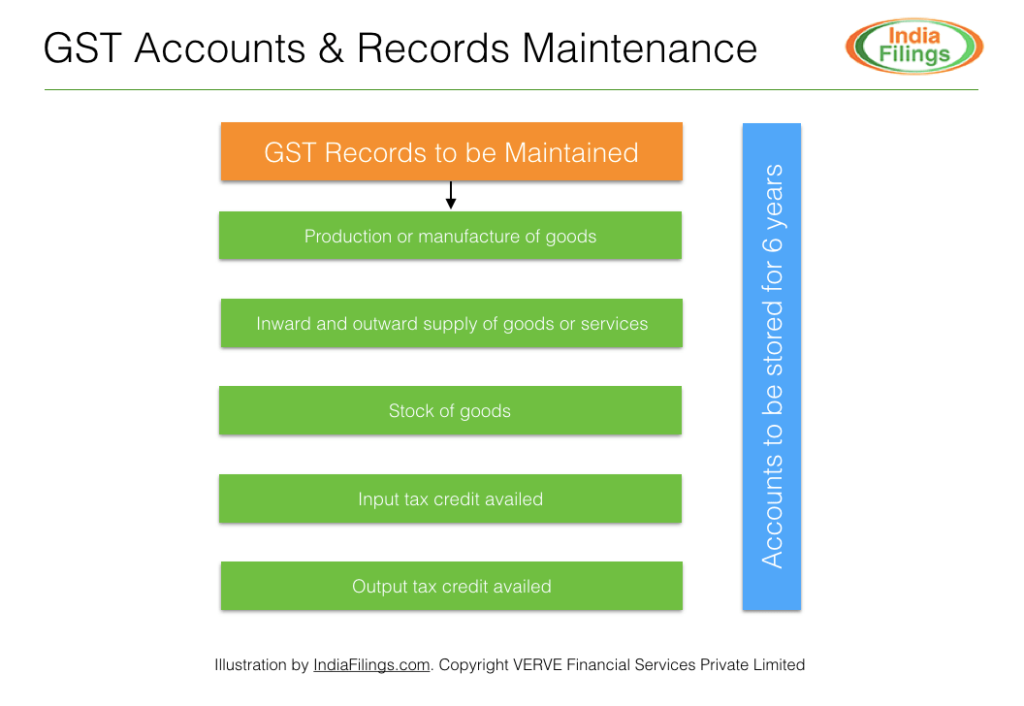

Necessary Records

According to Section 35 of the GST Act, all taxable persons under GST shall maintain the following records at their principal place of business:

- Production or manufacture of goods;

- Inward and outward supply of goods or services or both;

- The stock of goods;

- Input tax credit availed;

- Output tax payable and paid; and

- Other particulars as prescribed.

Accounts maintained by a

taxable person under GST along with all invoices, bills of supply, credit and debit notes, and delivery challans relating to stocks, deliveries, inward supply and outward supply should be maintained for a period of 6 years from the date of furnishing GST annual return. Further, the entity should keep all the related GST accounts and records at the place of business mentioned in the certificate of registration. GST Accounts & Records Maintenance

GST Accounts & Records Maintenance

Necessary GST Accounts to Maintain

In addition to the regulations mentioned in the GST Act, an additional requirement for maintaining accounts and records under GST has been provided for in the GST Accounts and Records Rules. According to the GST Accounts and Records Maintenance Rules, all taxable persons registered under GST should mandatorily maintain the following accounts in addition to the records mentioned above.

- A true and correct account of the goods or services imported, exported or supplies attracting payment of tax on reverse charge along with relevant documents, including invoices, bills of supply, delivery challans, credit notes, debit notes, receipt vouchers, payment vouchers, refund vouchers and e-way bills.

- Accounts of stock in respect of goods received and supplied by the taxpayer, and such account shall contain particulars of opening balance, receipt, supply, goods lost, stolen, destroyed, written off or disposed of by way of gift or free sample and balance of stock including raw material, finished goods, scrap and wastage thereof.

- Maintain an account, containing the details of tax payable (including tax payable, tax collected and paid, input tax, input tax credit claimed, together with a register of tax invoice, credit note, debit notes, delivery challan issued or received during any tax period.

- Maintaining details of Suppliers with information including names and complete addresses of suppliers from whom he has received the goods or services chargeable to tax under GST;

- Maintain details of Customers with information including names and complete addresses of the persons to whom he has supplied goods or services, where required under GST;

- Complete address of the premises where the taxpayer stores the goods, including goods stored during transit along with the particulars of the stock stored therein.

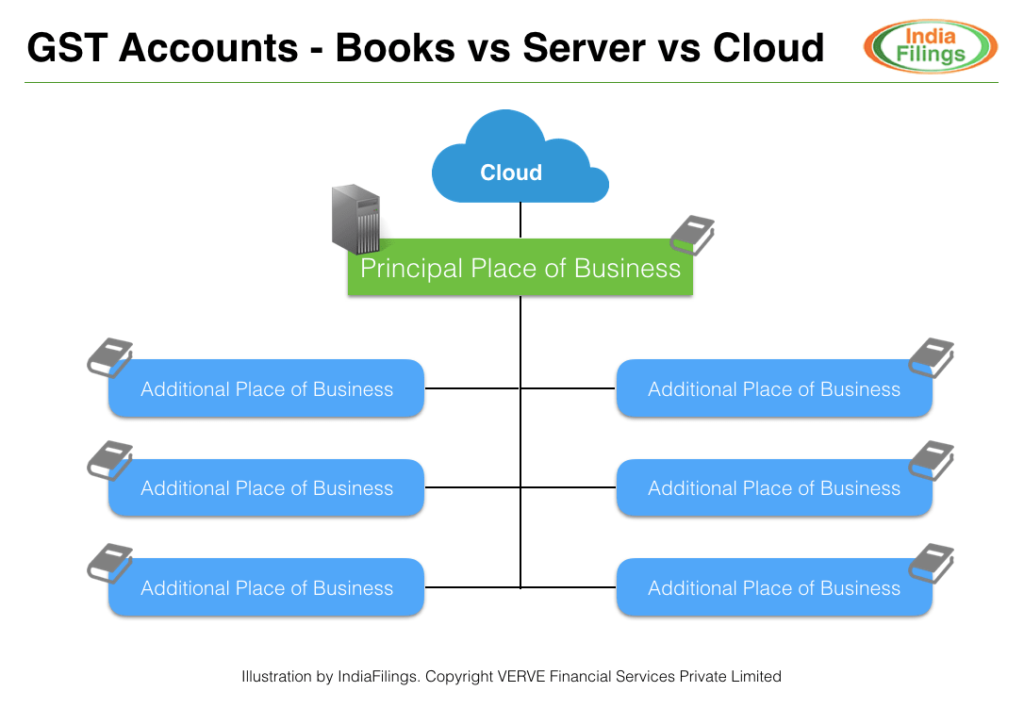

How to Maintain GST Accounts?

The taxpayer should maintain all GST accounts and records, including the books of account at the principal place of business. Further, the accounts shall also include records relating to additional place of business, if required. For all the GST records maintained manually, the accountant should include serial number system for each of the volume of books of account. While maintaining

GST account manually, if any entry in any of the registers or accounts or documents must be erased, effaced or overwritten, then it should be scored out under attestation, and thereafter correct entry should be recorded. If GST accounts are maintained electronically, then there should be a log of every entry edited or deleted. Also, if GST accounts and records are maintained electronically, then the records should be authenticated by means of a digital signature and should be accessible from every related place of business mentioned on the GST registration certificate. Finally, any documents, registers, or any books of account belonging to a registered person that are found at any premises, even will be presumed to be maintained by the taxpayer, unless proved otherwise. Hence, it is important to ensure that all accounting and financial information is maintained safely by the taxpayer. According to the GST Accounts and Records Rules, if any taxable goods stored at any place(s) other than those declared by the taxpayer in his/her accounts or records, without any other proof of valid documents; then, the Officer would levy tax. The Officer shall apply the tax as it applies to supplied goods by the registered person. Hence, the taxpayer must maintain all the record of inventory and goods-in-transit under GST as prescribed.

Necessary GST Accounts required to maintain by Agents, Brokers, Real Estate Brokers and Stock Brokers

Under GST, the word Agent means a person, including a factor, broker, commission agent, arhatia, del credere agent, an auctioneer or any other mercantile agent, by whatever name called, who carries on the business of supply or receipt of goods or services or both on behalf of another. All agents or brokers, including real estate agents and brokers, should mandatorily maintain the following additional records:

- Particulars of authorization received by him from each principal to receive or supply goods or services on behalf of such principal separately;

- Details including description, value and quantity (wherever applicable) of goods or services received on behalf of every principal;

- Particulars including description, value and quantity (wherever applicable) of goods or services supplied on behalf of every principal;

- Details of accounts furnished to every principal; and

- Tax paid on receipts or on the supply of goods or services effected on behalf of every principal.

Necessary GST Accounts required to maintain by Manufacturers

All persons involved in the manufacturing of Goods under GST should mandatorily maintain monthly production accounts, showing quantitative details of raw materials or services used in the manufacture and quantitative details of the goods so manufactured including the waste and by-products.

Necessary GST Accounts required to maintain by Service Providers

All taxable persons providing services taxable under GST should maintain accounts showing quantitative details of goods used in the provision of services, details of input services utilized and the services supplied.

Necessary GST Accounts required to maintain for Works Contract

Person registration with GST and involved in executing works contract should keep a separate account for works contract with details including:

- The names and addresses of the persons on whose behalf the works contract is executed;

- Description, value and quantity (wherever applicable) of goods or services received for the execution of works contract;

- Description, value and quantity (wherever applicable) of goods or services utilized in the execution of works contract;

- Details of payment received in respect of each work contract; and

- The names and addresses of suppliers from whom he received goods or services.

Know more about LEDGERS, an online GST Accounting Software for maintaining GST accounts.