IndiaFilings

Expert

Published on: Apr 22, 2026

GST refund applies to any taxpayer upon making extra GST payment in the form of tax, interest, penalty, fees or any others. For the refund process, the taxpayer shall apply through FORM GST RFD-01, as prescribed. To file FORM GST RFD-01, the individual can log in to GST Common Portal, GST Facilitation Centre or aHow to Get GST Refund?

IndiaFilings helps you to process your GST refunds quickly and effectively!

As per Section 54 of the GST Act, any of the following situations may necessitate a GST refund application to be filed by the taxpayer: GST laws have standardised procedure for processing a GST refund claim across India. The taxpayer must file all GST refund applications online in a standardised form on the GST Common Portal. The person shall also file returns on a monthly basis for claiming refund amount in the credit balance. On filing a refund application, an acknowledgement for refund application would be provided within 14 days of the refund application is acceptable.

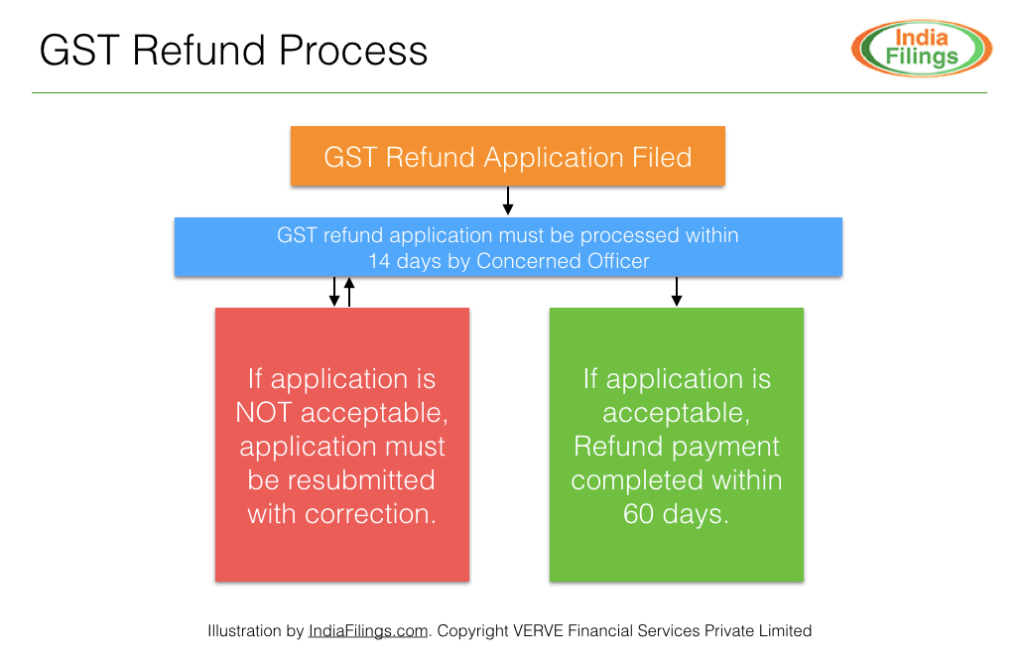

On receiving the refund request, the concerned Officer would have to convey the status of the application within 14 days. If there are any deficiencies in the application, the GST refund request would be sent back to the applicant along with the list of deficiencies and the applicant can refile the application. If there are no errors or deficiencies, the GST refund claims, if in the order must be sanctioned within a period of 60 days from the date of receipt of the claim. Officers are also not allowed to issue deficiencies memo after the 14 day period during when there are required to process the GST refund application. If the taxpayer exceeded the timelines above or mandatory period, the individual becomes liable to pay the interest along with the refund amount from the expiry of 60 days till the date of payment. The GST Council on meetings held on 18th and 19th May 2017 has recommended a 6% and 9% interest rate, respectively. On any circumstances, if the taxpayer made any pre-deposit for refund claim before any appellate authority, then the interest becomes payable from the date of making such payment. Any taxpayer can claim a refund of any tax, interest, For claiming GST refund, the applicant must maintain and file proper documentation. Along with all GST refund request, a statement of relevant invoices pertaining to the claim must be filed. As per the GST rules, the taxpayer shall maintain the invoice filed by the taxpayer for a minimum period of 7 years. In favour of refunding export of services, the taxpayer should produce the relevant bank realisation certificates evidencing the receipt of payment in foreign currency. If the supplier makes the claim for the GST refund to an SEZ unit, the concerned individual shall produce an endorsement from the Proper Officer evidencing receipt of such goods/services associated the SEZ. The process also requires a declaration from the SEZ unit stating that input tax credit of the tax paid by the supplier remains unclaimed. However, if the concerned individual applies only to claim a refund for the accumulated input tax credit, the application shall include a statement containing the invoice. In case of a claim of GST refund on account of any order or judgment of appellate authority or court, the reference number of the order giving rise to refund should be submitted along with the GST refund request. For crossing the bar of unjust enrichment and upon claiming a refund for less than Rs.2 Lakhs, the taxpayer must submit a self-declaration stating the effect that the incidence of tax remains unpassed passed to any other person. For refund claims exceeding Rs.2 Lakhs, a certificate from aClaiming GST Refund

GST Refund Process

Interest Payable

Procedure for Filing Refund Request

Documents Required

Statement of Relevant Invoices

For Export of Services

For Supplies Made to SEZ Units

Refund on Account of Judgement

Claiming Refund for Unjust Enrichment

Chartered Accountant Certificate

Streamline your GST refund process effectively with IndiaFilings experts!