IndiaFilings

Expert

Published on: Jul 30, 2026

GSTR-3A - Notice for Not Filing GST Return

GSTR-3A is a notice for not filing GST returns issued under the GST regulations. Taxable persons registered under GST shall file GST returns periodically. The due date and the type of return to be filed varies based on the type of

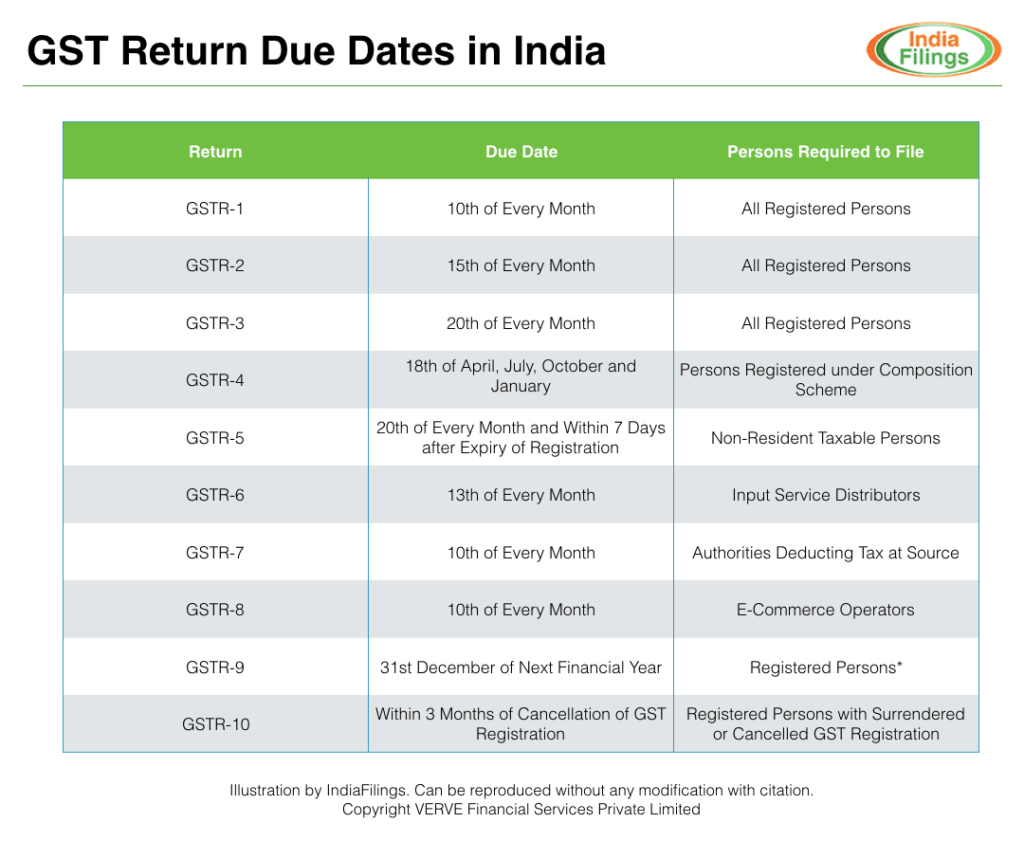

GST registration obtained by the taxpayers. Regular taxpayers registered under GST have to file 3 GST returns a month namely, GSTR-1, GSTR-2, and GSTR-3. Casual taxable persons, non-resident taxable persons, and taxpayers registered under the Composition scheme have to file different types of GST returns on due dates, as shown below. GST Return Filing Due Dates

GST Return Filing Due Dates

GSTR-3A: Notice for Not Filing GST Return

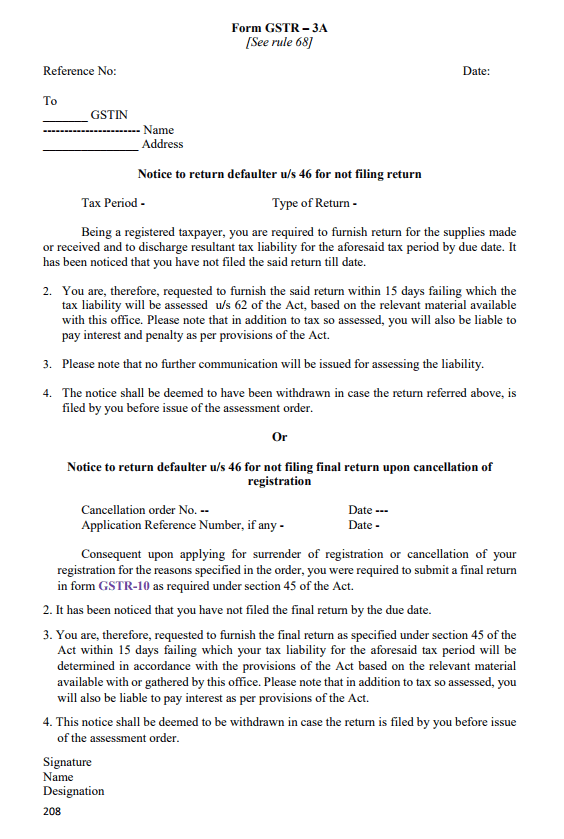

Upon failure to file the GST returns on a regular basis, the GST department issues GSTR-3A to the taxpayer. The following is a sample GSTR-3A tax notice:

Sample GSTR-3A

GSTR-3A can be classified under two categories as follows:

Sample GSTR-3A

GSTR-3A can be classified under two categories as follows:

Notice to File Pending GST Return

In the first type of GSTR-3A notice, the GST department provides an opportunity for the taxpayer to file any pending GST returns with penalty or interest and regularize the GST compliance. The following reasons shall apply for issuing the notice: Being a registered taxpayer, you are required to furnish return for the supplies made or received and to discharge resultant tax liability for the aforesaid tax period by due date. It has been noticed that you have not filed the said return till date.

-

You are, therefore, requested to furnish the said return within 15 days failing which the tax liability will be assessed u/s 62 of the Act, based on the relevant material available with this office. Please note that in addition to tax so assessed, you will also be liable to pay interest and penalty as per provisions of the Act.

-

Please note that no further communication will be issued for assessing the liability.

-

The notice shall be deemed to have been withdrawn in case the return referred above, is filed by you before issue of the assessment order.

Responding to notice to file GST return

The taxpayer should file for GST returns even if the business stops the operation or no transactions for the month. Hence, the taxpayer should always file any pending GST returns immediately after receiving the notice from the GST department. After filing the GST returns and clearing any tax liabilities, the taxpayer can apply for cancellation. In the case of nil transactions, the taxpayer shall apply to discontinue the GST compliance. In any case, if the taxpayer regularizes GST compliance within 15 days, then the GST registration would be valid. In case the taxpayer fails to respond to the above notice, the department shall cancel the GST registration and issue the following notice:

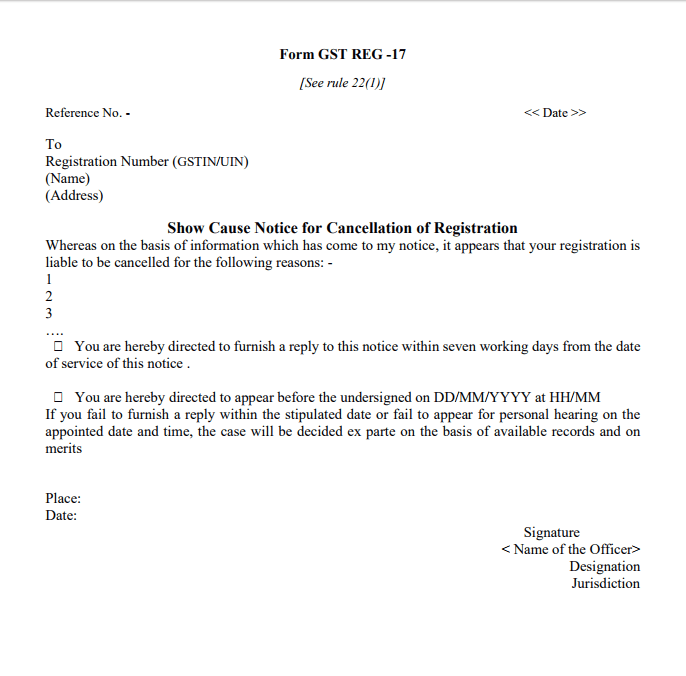

Notice of Cancellation of GST Registration

If a taxpayer after receiving a notice requesting GST return filing has not complied or filed GST returns within 15 days of notice, the following notice in Form GST REG-17 can be issued by the GST department with show-cause notice for cancellation of GST registration.

Sample GST REG-17

In such a case, the taxpayer must immediately file the overdue GST returns within 7 days, provide a written reply to the tax office about the reason for the delay in filing of GST returns and appear before the concerned officer in person on the date and time mentioned in the show-cause notice.

In case the taxpayer is not able to file GST returns, a reply citing reasons for the delay in filing GST returns along with a request for extension can be submitted in writing. The authorised person under GST will also have to appear before the tax officer for the personal hearing and decide on a course of action.

gst registration to read on GST Registration for Branches & Business Verticals

Sample GST REG-17

In such a case, the taxpayer must immediately file the overdue GST returns within 7 days, provide a written reply to the tax office about the reason for the delay in filing of GST returns and appear before the concerned officer in person on the date and time mentioned in the show-cause notice.

In case the taxpayer is not able to file GST returns, a reply citing reasons for the delay in filing GST returns along with a request for extension can be submitted in writing. The authorised person under GST will also have to appear before the tax officer for the personal hearing and decide on a course of action.

gst registration to read on GST Registration for Branches & Business Verticals

Notice to File GST Final Return - GSTR-10

After the cancellation or surrender of a GST registration, the taxpayer must file GSTR-10 return within 3 months. In case the taxpayer failed to file GSTR-10, then the following notice would be issued by the GST department.

The taxpayer should provide the final return in Form GSTR-10 as per Section 45 of the Act when surrendering or canceling the GST registration for the following reasons:

- It has been noticed that you have not filed the final return by the due date.

- You are, therefore, requested to furnish the final return as specified under section 45 of the Act within 15 days failing which your tax liability for the aforesaid tax period will be determined in accordance with the provisions of the Act based on the relevant material available with or gathered by this office. Please note that in addition to tax so assessed, you will also be liable to pay interest as per provisions of the Act. This notice shall be deemed to be withdrawn in case the return is filed by you before

- This notice shall be deemed to be withdrawn in case the return is filed by you before issue of the assessment order.