GST Form ITC-01 is a declaration form that is used to claim the

input tax credit. An input tax credit means that a taxpayer can claim the amount that has been already paid as GST while making GST payment to the Government which was collected from the customers.

Entitlement of the Form

According to Section 18(1) of the CGST Act 2017, the registered person can claim an input tax credit by filing declaration form

GST ITC-01. For inputs in stock as finished, semi-finished or capital goods, the credits can be availed as given below.

For once in a lifetime of the taxpayer, the day before the date of registration, it can be claimed according to Clause (a) or clause(b) of sub-section(1) of Section 18.

During a financial year, the day before the day from when the taxpayer is liable to pay tax under Section 9, to claim according to Clause(c) of sub-section (1) of Section 18.

Claims made according to Clause (d) of sub-section (1) of Section 18, all supplies claimed by a registered taxpayer from a day before the date is taxable.

Application Procedure

Given below are the steps to declare and file a claim of ITC under Section 18(1)(a) in Form ITC-01.

Step 1: Login to the Portal

The taxpayer has to login to the official GST Portal.

Step 2: Enter the Details

The taxpayer has to enter the username and password.

Step 3: Click ITC Forms

From the ‘Services’ tab, the taxpayer has to select ‘Returns’ and then click on ‘ITC Forms’. The GST ITC Forms page is displayed on the screen.

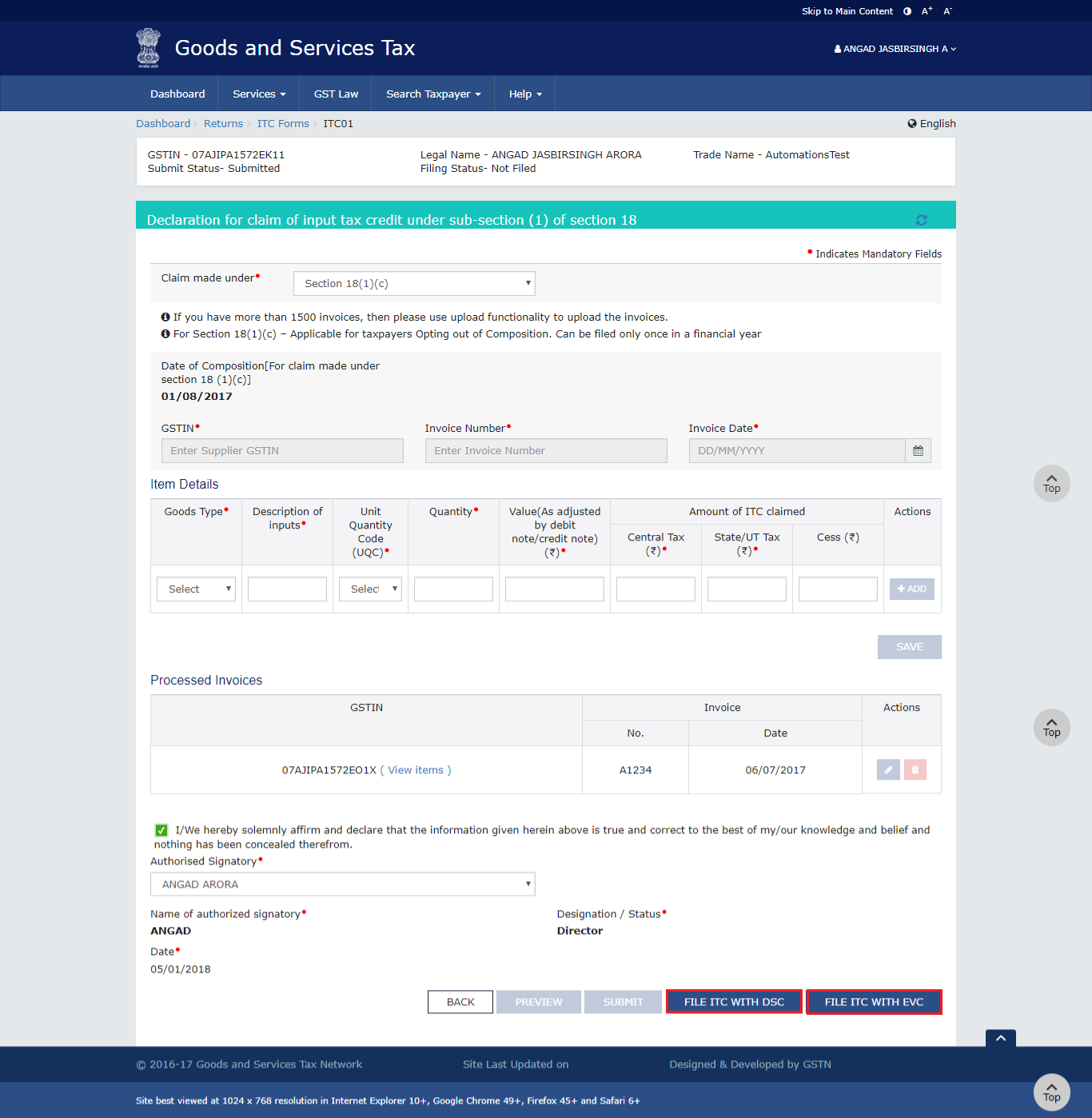

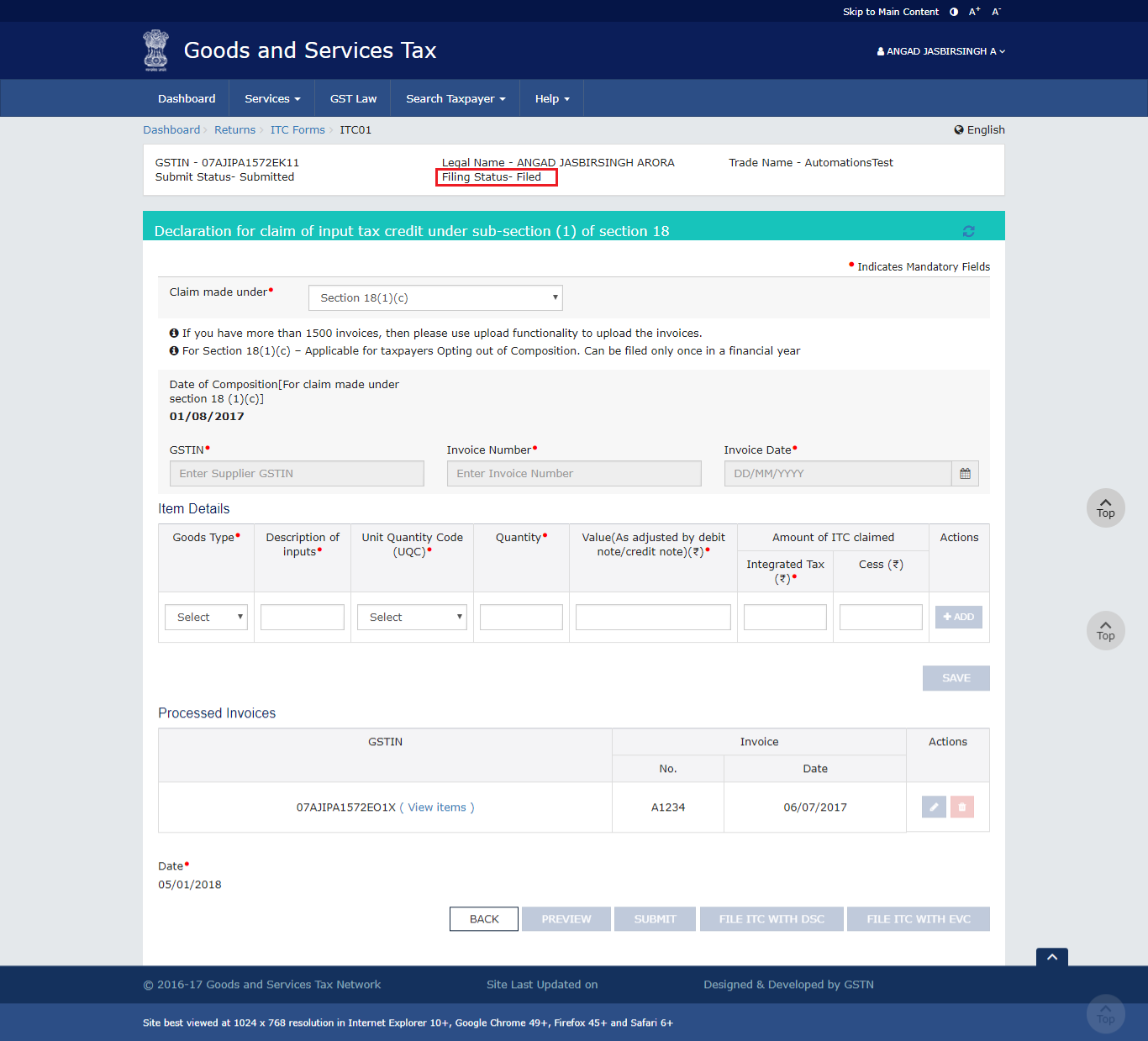

Step 3-GST Form ITC-01Step 4: Click Prepare Online

Under GST ITC – 01, click ‘Prepare Online’ button if the taxpayer desires to provide a statement by making entries on the GST Portal.

Step 4-GST Form ITC-01Click here to proceed with Offline Procedure

Step 5: Select the Section

The taxpayer has to select the appropriate section from the ‘Claim Made Under’ drop-down list.

Step 5-GST Form ITC-01

Section 18(1)(a) is applicable for those taxpayers who have applied for registration within 30 days of becoming liable and this can be filed only once.

Step 6: Enter the GSTIN

In the GSTIN field, the taxpayer has to enter the GSTIN of the supplier who has supplied the goods or services.

Step 7: Enter the Invoice Number

In the ‘Invoice Number’ field, the taxpayer has to enter the invoice number.

Step 8: Enter Invoice Date

In the ‘Invoice Date’ field, the taxpayer has to select the date when the invoice was generated using the calendar.

The Invoice date should be prior to the grant of approval.Step 9: Select Goods Type

The taxpayer has to select the ‘Goods Type’ from the drop-down list.

Step 10: Enter the Description of Inputs

In the ‘Description of Inputs’, the taxpayer has to enter the description of inputs that are in stock, the inputs contained in semi-furnished or finished goods that are in stock.

Step 11: Select Unit Quantity Code

The taxpayer has to select the ‘Unit Quantity Code (UQC) from the drop-down list.

Step 12: Enter the Quantity

In the ‘Quantity’ field, the taxpayer has to enter the number of inputs.

Step 13: Enter the Invoice Value

In the ‘Value’ (as adjusted by debit note/ credit note) field, the taxpayer has to enter the invoice value.

Step 14: Enter ITC Amount

The taxpayer has to enter the amount of ITC claimed as the Central Tax, State/UT Tax, Integrated Tax and Cess.

CGST and SGST amount should be the same and the total sum of CGST and SGST should not exceed the invoice value (IGST). In the case of an Inter-State purchase, IGST amount should not exceed the Invoice Value.Step 15: Click Add

The taxpayer has to click the ‘Add’ button.

Step 15-GST Form ITC-01Step 16: Click Save

Once all the details are entered, the taxpayer has to click the ‘Save’ button.

Step 16-GST Form ITC-01

The taxpayer can click the Edit/ Delete icon to edit or delete the Invoice.

Step 16-GST Form ITC-01Step 17: Previewing the Form

The taxpayer has to click the ‘Preview’ button to preview the draft for GST ITC-01.

Step 17-GST Form ITC-01

The draft is displayed in the PDF Format.

Step 17-GST Form ITC-01Step 18: Click Submit

The taxpayer has to click the ‘Submit’ button to submit the form.

Step 18-GST Form ITC-01Step 19: Click Proceed

The taxpayer has to click the ‘Proceed’ button. After submitting the data, the page is frozen and no changes can be made.

Step 19-GST Form ITC-01Step 20: Refresh the Page

The taxpayer has to refresh the page and the status of GST ITC-01 changes to Submitted.

Step 20-GST Form ITC-01

Updating Certifying Chartered Accountant’s or Cost Accountant’s Details

Once the form is submitted, and if the ITC claimed is more than Rs.2 Lakh, then the taxpayer has to update the Chartered Accountant/ Cost Accountant details.

Application Procedure

Given below are the steps to upload the Chartered Accountant/ Cost Accountant certificate on the GST Portal.

Step 1: Enter the Name

The taxpayer has to enter the name of the firm that issued the certificate in the ‘Name of the Firm Issuing Certificate’ field.

Step 2: Enter the Chartered Accountant or Cost Accountant

The taxpayer has to enter the name of the Chartered Accountant or Cost Accountant in the ‘Name of the Certifying Chartered Accountant/ Cost Accountant’ field.

Step 3: Enter the Membership Number

The taxpayer has to enter the membership number of the Chartered Accountant or Cost Accountant in the ‘Membership Number’ field.

Step 4: Date of Issuance of Certificate

The taxpayer has to select the ‘Date of Issuance of Certificate’ using the calendar.

Step 5: Upload the Certificate

The taxpayer has to upload the ‘Chartered Accountant or Cost Accountant’ certificate in the JPEG format. The file should not be more than 500 KB.

Step 6: Save CA Details

The taxpayer has to click ‘Save CS Details’ to save all the details.

Step 6-GST Form ITC-01Step 7: Select the Checkbox

The taxpayer has to select the checkbox for declaration.

Step 8: Select the Authorized Signatory

In the ‘Authorized Signatory’ drop-down list, the taxpayer has to select the authorized signatory. This option enables two buttons ‘File ITC with DSC’ or ‘File ITC with DVC’.

Step 8-GST Form ITC-01File With DSC

The taxpayer has to click the ‘Proceed’ button and then has to select the certificate and click the ‘Sign’ button.

Step 8-GST Form ITC-01File with EVC

The taxpayer has to enter the OTP that is sent on Email and to the registered mobile number of the Authorized Signatory and then click ‘Verify’ button.

Step 8-GST Form ITC-01Step 9: ARN Generation

The success message is displayed on the screen. ARN is generated and it is sent to the taxpayer via SMS and email. When the page is refreshed, the status of GST ITC – 01 is changed to ‘Filed’.

Step 9-GST Form ITC-01

Benefits of Filing GST ITC-01

A taxpayer can avail the following benefits by filing GST ITC-01.

The form enables a newly registered taxpayer to take credit of input tax for inputs that are held in stock and inputs that are contained in a semi-finished or finished good that is in stock on the day immediately after the date from which he/she becomes liable to pay tax under GST provisions.

The form benefits the taxpayers who have been taken registration in a voluntary basis, to take credit of input for inputs that are held in stock and inputs maintained as semi-finished or finished goods that are held in stock on the day immediately after the date of grant of registration.

The form enables those taxpayers opting out of composition scheme and opting to pay tax as a normal taxpayer and to take credit of input tax for inputs that are held in stock, inputs maintained in semi-finished or finished goods that are held in stock or on capital goods on the day immediately after the date on which he becomes liable to pay tax under Section 9.

The form entitles such registered people whose supply of goods and services to become taxable from exempt to take credit of input tax for inputs held in stock and inputs maintained in semi-finished or finished goods that are held in stock relatable to such exempt supply and on capital goods that are exclusively used for such exempted supply on the day immediately preceding the date from which such supply become taxable.

Restriction on claiming ITC

As per the CGST Rules, Rule 36 provides the conditions for claiming of Input Tax Credit (ITC). Now, a new sub-rule 36(4) has been inserted under Rule 36 for the registered taxpayers to provide ITC in respect of Invoices or debit notes are not uploaded in Form GSTR-1 by suppliers cannot exceed 20% of the eligible ITC pertaining to invoices or debit notes uploaded by the suppliers.

Applicability of Rule 36(4)

The restriction on claiming ITC under Rule 36(4) is not applicable for Input Tax Credit on import of goods and services, ITC on which GST paid under Reserve Charge Mechanism, ITC on Input service distributor (ISD) invoices.

The restriction would apply on debit notes or invoices on which Input Tax Credit availed after 9th October 2019.

Basis of Calculation

The calculation for restriction would be calculated on a consolidated basis but not on the supplier basis.

The calculation for restriction would be calculated on total eligible credit from all suppliers against all supplies details have been uploaded by the suppliers.

The calculation for restriction would be calculated on those invoices uploaded, by the suppliers, as on the due date of Form GSTR-1 return filing for the said tax period.

The calculation for restriction would not consider those invoices on which Input Tax Credit is ineligible as per Section 17(5).

Note: Input Tax Credit (ITC) would be calculated upon on the entries in GSTR-2A on the due date of filing of Form GSTR-1 by the supplier. Input Tax Credit applies only for those suppliers who have filed their Form GSTR-1 on 11th of every month should be taken into consideration for the calculation of 20% restriction.

Example

The eligible ITC that can be availed as explained in a tabulated form:If a taxpayer receives 100 invoices for inward supply of goods or services involving Input Tax Credit of Rs.10 lakhs from several suppliers during the month of October 2019 and has to claim ITC in GSTR-3B of October, to be filed by 20th November 2019.

S.No

Details of suppliers invoices in which recipient eligible for ITC

20% of eligible credit where invoices uploaded

Eligible ITC has taken in GSTR-3B to be filed on or before 20th November 2019

1.

Suppliers furnished 80 invoices in GSTR-1 involving ITC of Rs.6 lakhs on the 11th November 2019

Rs.1,20,000/-

Rs.7,20,000/-(Rs.6,00,000/- of eligible ITC applicable as per GSTR-2A + Rs.1,20,000/- (for 20% of eligible ITC as per GSTR-2A))

2.

Suppliers furnished 80 invoices in GSTR-1 involving ITC of Rs.7 lakhs on the 11th November 2019

Rs.1,40,000/-

Rs.8,40,000/-(Rs.7,00,000/- of eligible ITC available as per GSTR-2A + Rs.1,40,000/- (for 20% of eligible ITC as per GSTR-2A))

3.

Suppliers furnished 80 invoices in GSTR-1 involving ITC of Rs.8.5 lakhs on the 11th November 2019

Rs.1,70,000/-

Rs.10,00,000/-(Rs.8,50,000/- of eligible ITC available as per GSTR-2A + Rs.1,50,000/- (for 20% of eligible ITC as per GSTR-2A))

Note: The additional amount of ITC availed shall be limited to ensure that the total ITC availed not exceeding the total eligible Input Tax Credit.