IndiaFilings

Expert

Published on: Mar 28, 2026

Is GST Applicable on Imported Goods?

Under the

GST regime, both the import of goods and or services into the territory of India would be treated as supply of goods or services in the course of inter-state trade attracting the levy of IGST. Hence, GST on imports will be treated as deemed inter-state supplies and would be subject to GST. In this article, we look at the applicability of GST on goods imported into India.GST on Import of Goods

The GST Act defines the import of goods as bringing goods into India from abroad. Accordingly, the GST Act considers all imports into India as inter-state attracting IGST. In addition to the IGST, the import would also be subject to Customs Duties. Thus, when goods are imported into India, IGST would be applied to the value of the goods and collected along with Customs Duty. The Customs Tariff Act, 1975 has already been amended to provide for levy of integrated tax and the compensation cess on imported goods, in anticipation of the GST rollout. While GST applies to imports in addition to the Basic Customs Duty, GST Compensation Cess shall levy on certain luxury and demerit goods under the Goods and Services Tax (Compensation to States) Cess Act, 2017.

Learn about the difference between IGST, CGST and SGSTAmount of GST on Imported Goods

HSN (Harmonised System of Nomenclature) code has been used for the purpose of classification of goods under the GST regime. Hence, the classification of the item for Customs Duty purpose and IGST calculation purpose would be harmonised. The amount of GST payable on imported goods would be dependent on the assessable value plus customs duty levied under the Customs Act, and any other duty chargeable on the goods. The value of the imported article for the purpose of levying GST Compensation cess would be, assessable value plus Basic Customs Duty levied under the Act, and any sum chargeable on the goods in the same manner as a duty of customs. Thus, the GST Compensation cess shall exclude the IGST paid while the calculating value.Calculating GST on Imports

- The assessable value of goods imported into India shall apply at the value for Rs.100.

- Basic Customs Duty is 10% ad-valorem.

- The integrated tax rate shall apply at the rate of 18%.

Paying GST for Imports

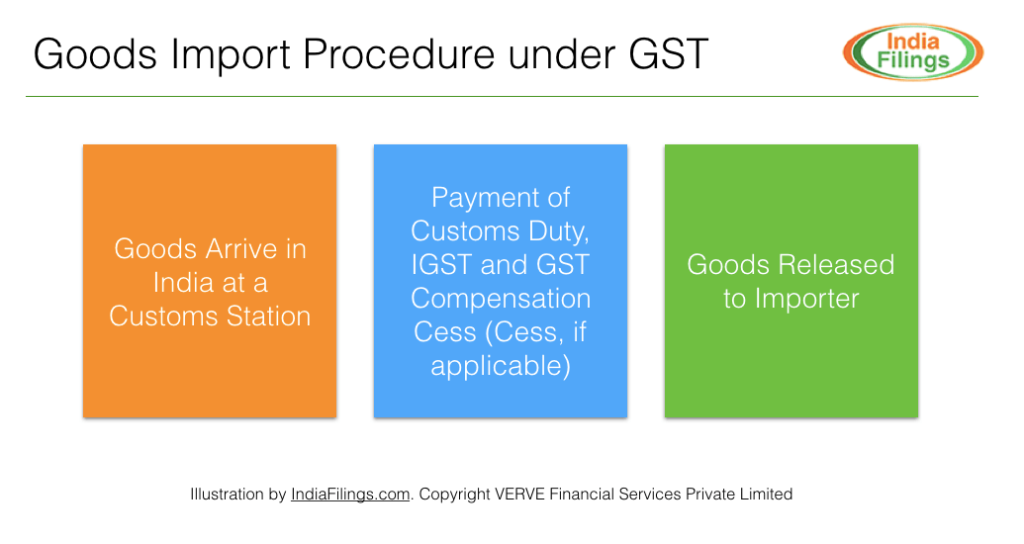

Under The Customs Act, 1962, removal of goods from a customs station can be done only after payment of Customs Duty and the Integrated GST tax payable. Thus, the importer should pay the Integrated tax at the time of removal of goods from a customs station to a warehouse.

Goods Import Procedure under GST

Goods Import Procedure under GST

Input Tax Credit for Imports

The input tax credit shall apply under the GST regime to set off the cascading effect of indirect tax and ensure that the consumer bears GST. The integrated tax also applies for the Input tax credit on import of goods. The importer shall receive the Input tax credit of the IGST paid during the time of import. Further, the taxpayer can utilize the as Input Tax Credit for payment of IGST liability on outward supplies. Though input tax credit applies for the IGST paid, the input tax credit remains unclaimable for The Basic Customs Duty (BCD) paid by the importer.

Start your Import & Export Code Registration with IndiaFilings experts!