RENU SURESH

Expert

Published on: Jun 24, 2026

Tax Audit Report: Form 3CA, 3CB, 3CD, Due Date, Documents, Penalty & Procedure

Once your Tax Audit is completed, the next crucial step is filing the Tax Audit Report with the Income Tax Department. This report, prepared by a Chartered Accountant (CA), ensures that your financial statements are accurate, all deductions are correctly claimed, and your business or professional income complies with Section 44AB of the Income Tax Act, 1961. In this article, we will look into the step-by-step process for filing a Tax Audit Report, its key components, the forms involved, due dates, and the benefits of timely filing.

Tax Audit under Section 44AB

Section 44AB mandates that certain taxpayers must get their accounts audited by a Chartered Accountant (CA) and submit the Tax Audit Report to the Income Tax Department before the due date. Tax Audit applies to the following categories:

- Business: If total sales, turnover, or gross receipts exceed ₹1 crore in a financial year. The turnover limit is ₹10 crore if cash transactions are limited to 5% of total transactions (both receipts and payments).

- Profession: If gross receipts exceed ₹50 lakh in a financial year.

- Presumptive Taxation Scheme: If a taxpayer is eligible for presumptive taxation under Section 44AD, 44ADA, or 44AE, but claims income lower than the presumptive rate and the income exceeds the basic exemption limit.

What is a Tax Audit Report

A Tax Audit Report is a formal Report prepared by a Chartered Accountant (CA) after examining the books of accounts of a business or profession, as required under Section 44AB of the Income Tax Act, 1961. Tax audit applies in specific situations where a business or professional’s turnover or receipts exceed prescribed limits. The purpose of the audit is to verify whether the accounts have been maintained accurately and whether the taxable income has been computed correctly in line with the provisions of the Income Tax Act.

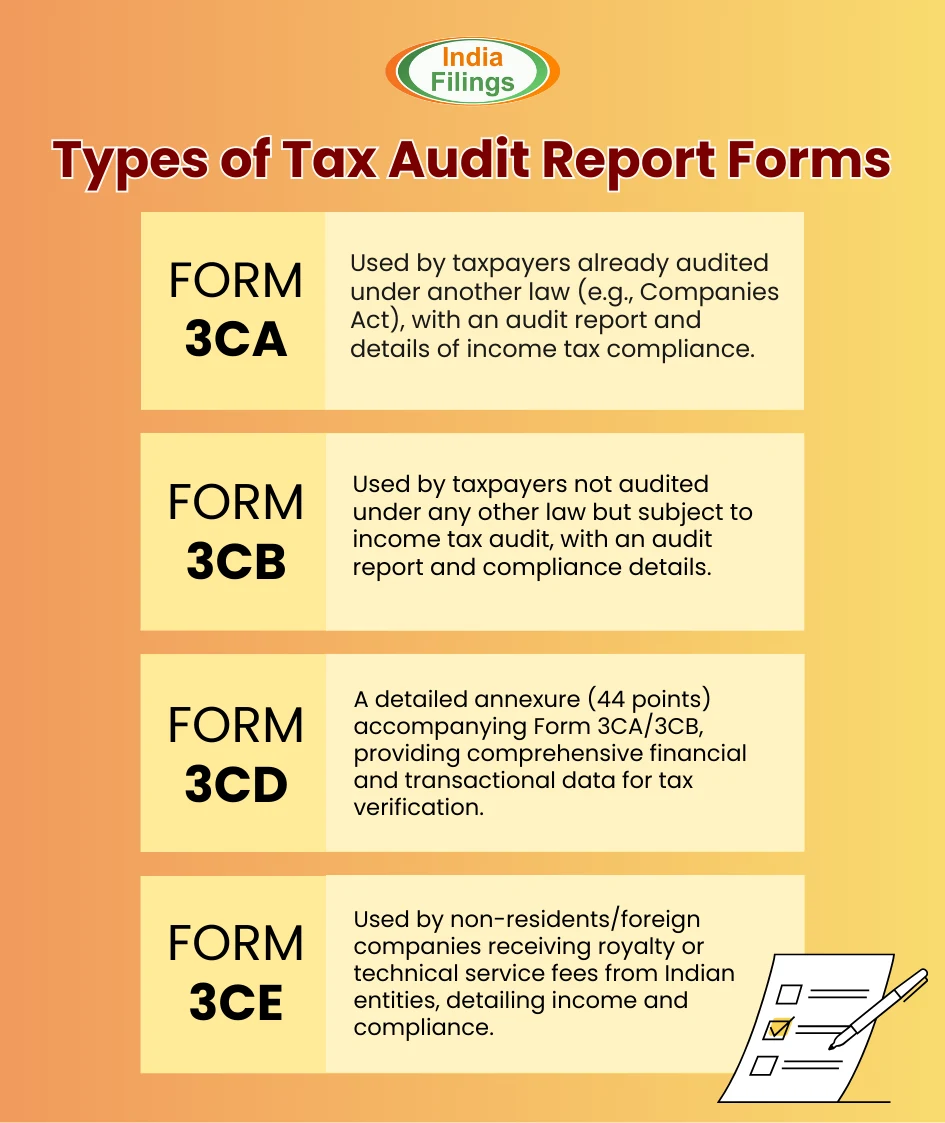

Tax Audit Report – Forms 3CA, 3CB, 3CD, and 3CE

The Income Tax Department has prescribed specific formats for filing the Tax Audit Report, each serving a distinct purpose.

- Form 3CA and Form 3CB: These contain the auditor’s Report and general audit information.

- Form 3CD: This is a detailed statement of particulars relating to the tax audit, including turnover, deductions, disallowances, and compliance details.

- Form 3CE: Applicable in the case of non-residents or foreign companies receiving royalties or fees for technical services from India.

Summary of Forms:

Form Name | Description |

Form 3CA-3CD | Tax Audit Report for taxpayers carrying on business or profession whose accounts are already required to be audited under any other law (e.g., Companies Act) in addition to the Income Tax Act. |

Form 3CB-3CD | Tax Audit Report for taxpayers carrying on business or profession whose accounts are not required to be audited under any other law except the Income Tax Act. |

Form 3CE | Tax Audit Report for non-resident taxpayers or foreign companies receiving royalty income or fees for technical services from India. |

Method to Upload and File a Tax Audit Report

The process of filing a Tax Audit Report has changed over the years. Below is the step-by-step method for both the earlier system (up to FY 2019-20) and the current system (FY 2020-21 onwards).

Up to FY 2019-20

- Add Chartered Accountant – The taxpayer logs in to the Income Tax e-filing portal and adds their Chartered Accountant (CA) using the “My Chartered Accountant” option.

- Upload by CA – The CA logs in to their own account on the portal and uploads the Profit & Loss Account, Balance Sheet, and Tax Audit Report in the prescribed forms.

- Approval by Taxpayer – The taxpayer reviews and approves the uploaded Tax Audit Report.

- File ITR – The taxpayer then files the Income Tax Return (ITR) using a Digital Signature Certificate (DSC).

FY 2020-21 Onwards

- Add Chartered Accountant – The taxpayer adds their CA in the e-filing portal.

- Upload by Taxpayer – The taxpayer uploads the Profit & Loss Account and Balance Sheet from their own login.

- Approval by CA – The CA verifies and approves the uploaded P&L and Balance Sheet.

- Filing by CA – The CA files the Tax Audit Report in the applicable forms.

- Approval by Taxpayer – The taxpayer reviews and approves the Tax Audit Report filed by the CA.

File ITR – The taxpayer files the ITR using DSC

Due Date to File Tax Audit Report

The Tax Audit Report (Forms 3CA/3CB with 3CD) for FY 2024–25, as required under Section 44AB, must now be submitted on or before 31st October 2025.

Due Date to File Income Tax Return (ITR): For taxpayers subject to tax audit under Section 44AB, the due date to file the ITR is 31 October 2025.

Action | Due Date |

Submit Tax Audit Report (Forms 3CA/3CB & 3CD)31 | 31 October 2025 (Extended from 30 September) |

File Income Tax Return (ITR) | 31 October 2025 |

Tax Audit Due DateAudit Due Date FY 2024-25

Tax Audit Report – Structure and Forms

Under Section 44AB of the Income Tax Act, 1961, the Tax Audit Report is divided into two main components – Form 3CA/3CB and Form 3CD – along with Form 3CE in specific non-resident cases. Each form serves a distinct purpose and contains specific details that must be furnished by the Chartered Accountant (CA) conducting the audit.

1. Form 3CA

Applicable when the taxpayer’s accounts are already audited under another law (e.g., Companies Act, LLP Act). This form contains basic details of the taxpayer, auditor, and audit scope.

- Name, Address, and PAN of the taxpayer.

- Name of the auditor.

- Law under which the accounts are audited (e.g., Companies Act, LLP Act).

- Date of the audit Report.

- Period covered by the Profit & Loss Account.

- Date of the Balance Sheet.

- Contains a declaration that Form 3CD is attached.

- Mentions any audit observations or qualifications based on Form 3CD.

- Includes auditor details: Name, Address, Membership Number, Place & Date of signing, Stamp, and Seal.

Download Form 3CA

2. Form 3CB

Applicable when the taxpayer’s accounts are not audited under any other law. This form contains a more detailed declaration by the auditor about the audit process.

- Date of Balance Sheet and P&L Statement; Name, Address, and PAN of the taxpayer

- Address where books of accounts are maintained; Address of branches if applicable

- Auditor’s remarks on observations, comments, discrepancies, and inconsistencies; Declaration that:

- All required information was obtained

- Proper books of accounts were maintained

- The Balance Sheet and P&L Account present a true and fair view

- A declaration that Form 3CD is attached to this Report

- Auditor’s details: Name, Address, Membership Number, Firm Registration Number, Date & Place of Signing.

Download Form 3CB

3. Form 3CD

This is a detailed statement of particulars containing 44 clauses covering financial and compliance information of the taxpayer. Some examples of disclosures include:

- Nature of business/profession

- Books of accounts are maintained

- Method of accounting and stock valuation

- Depreciation details

- Payments disallowed under Sections 40A(3) and 40(a)

- Compliance with TDS/TCS provisions

- GST turnover reconciliation

The Income Tax Department provides a prescribed format and online utility for CAs to upload Form 3CD along with Form 3CA/3CB.

Download Form 3CD

Form 3CE

Applicable for non-resident taxpayers or foreign companies earning royalty or fees for technical services from India, and covered under Section 44DA.

- Name, Address, and PAN of the non-resident; Financial year

- Declaration that all necessary information and explanations were obtained

- Certification on whether the non-resident has a Permanent Establishment or fixed place of profession in India

- Declaration of income from royalty or fees for technical services under Section 44DA

- Auditor’s signature, name, stamp, and seal

- Note: An annexure must be attached showing detailed computation of income from royalty or technical fees.

Download Form 3CE

Penalty for Not Filing Form 3CD

If a taxpayer who is required to have their books of accounts audited under Section 44AB of the Income Tax Act fails to do so, the Assessing Officer (A.O.) may levy a penalty under Section 271B.

Amount of Penalty – The lower of:

- 0.5% of total sales or turnover (for business) or 0.5% of gross receipts (for profession), OR

- ₹1,50,000.

Relief Provision – If the taxpayer can prove there was a reasonable cause for not getting the tax audit done (as per Section 273B), the penalty may be waived by the A.O.

Common reasonable causes accepted in the past include natural calamities, loss of accounts due to fire or theft, serious illness of key persons, and technical glitches on the e-filing portal

Step-by-Step Process for Filing a Tax Audit Report

Here’s a clear process flow to file a Tax Audit Report under Section 44AB:

1. Determine Applicability of Tax Audit

Check if your business or profession crosses the turnover/gross receipts limits prescribed under Section 44AB or falls under presumptive taxation rules with conditions requiring an audit.

2. Appoint a Chartered Accountant (CA)

Engage a practicing CA to conduct the audit of your books of accounts.

Add the CA to your profile on the Income Tax e-Filing Portal under the “My Chartered Accountant” section.

3. Prepare and Finalise Books of Accounts

Complete the Profit & Loss Account, Balance Sheet, and all necessary ledgers.

Ensure GST returns, TDS data, and bank statements are reconciled with the accounts.

4. Upload Financial Statements

Taxpayer should upload P&L and Balance Sheet; CA verifies them.

5. CA Prepares and Uploads the Tax Audit Report

- The CA fills in Form 3CA/3CB (auditor’s Report) and Form 3CD (statement of particulars).

- The Report is uploaded electronically using the CA’s e-filing login.

6. Taxpayer Approval

The taxpayer logs in to the Income Tax Portal, reviews the uploaded Report, and approves it digitally.

7. File the Income Tax Return (ITR)

Once the Tax Audit Report is approved, file the applicable ITR (usually ITR-3 for business/professional income) using a Digital Signature Certificate (DSC) before the due date.

Benefits of Timely Filing a Tax Audit Report

Filing your Tax Audit Report on time offers several legal, financial, and operational advantages:

- Avoidance of Penalties – Timely filing helps you steer clear of hefty penalties under Section 271B, which can be as high as ₹1,50,000 or 0.5% of turnover/gross receipts.

- Smooth ITR Filing – Having the audit Report approved well before the ITR deadline ensures a hassle-free return filing process without last-minute portal issues.

- Enhanced Business Credibility – Audited and timely filed accounts improve trust with banks, investors, suppliers, and government agencies.

- Reduced Risk of Scrutiny – Complete and accurate Reporting reduces the chances of assessment notices or tax scrutiny from the Income Tax Department.

- Better Financial Insights – The audit process highlights accounting errors, tax-saving opportunities, and compliance gaps, enabling better decision-making.

- Compliance History for Future Benefits – A consistent record of timely compliance can be beneficial for government tenders, loan applications, and registrations.

Key Components of a Tax Audit Report

A Tax Audit Report contains several important sections, each serving a specific compliance and verification purpose:

- General Information – Includes the taxpayer’s name, address, PAN, and other identification details. It also specifies the financial year covered by the audit.

- Financial Statements – Provides audited financial statements such as the Balance Sheet, Profit & Loss Account, and, if applicable, the Cash Flow Statement, detailing the business’s financial performance during the year.

- Audit Findings – Lists any discrepancies, non-compliance issues, or irregularities observed by the auditor in the books of accounts or related records.

- Supporting Documents – References key documents like bank statements, invoices, receipts, and contracts used to verify the accuracy of Reported figures.

- Auditor’s Opinion – Contains the Chartered Accountant’s professional assessment of whether the financial statements give a true and fair view and comply with the Income Tax Act. The opinion may be unqualified (clean) or qualified (with observations).

- Recommendations for Improvement – In some cases, auditors may provide suggestions to enhance accounting practices, improve compliance, and maintain better records for future audits.

Significance of a Tax Audit Report

The Tax Audit Report plays a vital role in ensuring transparency, accuracy, and compliance in financial Reporting:

- For Taxpayers – It verifies that income is correctly Reported, deductions are valid, and taxes are calculated as per law, reducing the risk of penalties or scrutiny.

- For Authorities – It enables the Income Tax Department to assess whether the taxpayer has complied with tax provisions and helps in identifying possible areas of non-compliance.

- For Policy Makers – Aggregated audit data helps evaluate the effectiveness of tax policies and ensures fairness in the tax system.

- For Businesses – A clean, timely tax audit Report enhances credibility with banks, investors, and government bodies, aiding in loans, tenders, and partnerships.

By understanding these elements and their significance, taxpayers can better prepare their records, respond to auditor queries, and maintain a strong compliance track record year after year.

Need expert assistance with your Tax Audit Report?

At IndiaFilings, our team of experienced Chartered Accountants and tax professionals can help you prepare and file your Tax Audit Report accurately and on time. From ensuring compliance with Section 44AB to guiding you through Forms 3CA, 3CB, and 3CD, we handle the entire process seamlessly.

Related Articles:

Key Amendments in Tax Audit Report (Form 3CD)

Section 44AB of Income Tax Act