IndiaFilings

Expert

Published on: Apr 22, 2026

Value of Supply - Related Party Transactions under GST

To regulate the value of supply under GST for the free market transactions, the Government of India (GoI) implemented guidelines for the valuation of goods and services. The guidelines shall regulate invoicing or distortion in the value of supply for the related party. The implementation of the guidelines shall result in a regulated and accountable

GST transaction between the buyer and the seller. This article details on determining the value of supply, related parties under GST and other details related to transactions for a value of supplyRelated Party under GST

The following

- Such persons are officers or directors of one another’s businesses;

- Persons legally recognised as partners in business;

- Such persons are employer and employee;

- Any person directly or indirectly owns, controls or holds twenty-five per cent. or more of the outstanding voting stock or shares of both of them;

- One of them directly or indirectly controls the other;

- A third person directly or indirectly controls both of them; (vii) together they directly or indirectly control a third person; or

- They are members of the same family;

Under GST, the term “related parties” also includes legal persons and persons who are associated in the business of one another in that one is the sole agent or sole distributor or sole concessionaire, of the other. Further, related parties are also referred to as related persons or distinct persons under GST.

Read about related parties transaction as per Companies Act, 2013.Related Party Transaction-Value of Supply

It is important to consider two rules defined in the rules for Determination of Value of Supply while calculating the value of supply between related parties.

Value of Supply- Transaction not Wholly in Money

In a lot of related party transaction, the consideration for the value of supply of goods and/or services might not be paid wholly in money. Hence, the related party shall ensure that all associated rules apply during the transactions if the transfer made for the supply not wholly in money. During those circumstances, the related party shall follow the following:

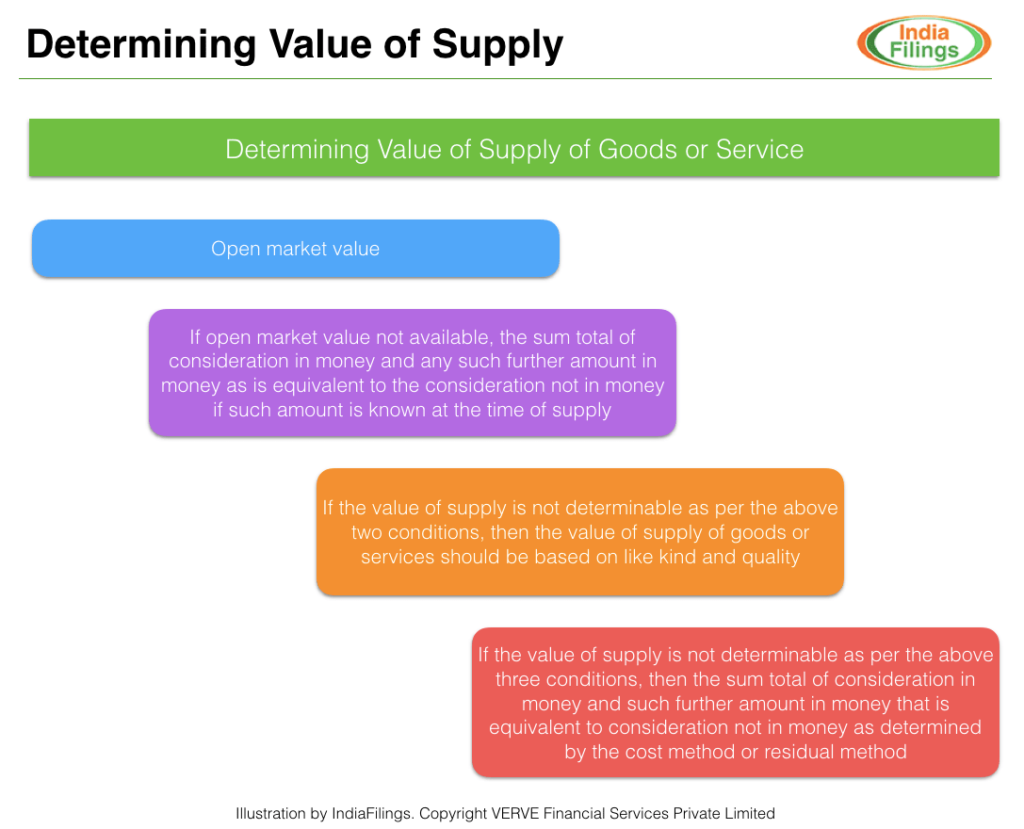

When the supply of goods or services is for a consideration not wholly in money, then the value of the supply should be calculated as:- The open market value of such supply;

- At the time of supply, any transaction of the amount in full or any further transaction equivalent to the value, but not in money, during unavailability of the open market,

- During unavailability of the open market, the total amount transferred in full for the value of the supply of goods or any transfer involved other than money equivalent to the value of the supply of goods or services,

- If the value of supply is not determinable as per the above three conditions, then the total of consideration in money and such further amount in money that is equivalent to consideration not in money as determined by the cost method or residual method.

Cost Method for Determining Value of Supply under GST

The value for the supply of goods or services or both shall apply at 110% for the cost involved for production, manufacturing, acquisition of such goods or provision of such services if the goods or services or both left unclassified in any of the rules prescribed in the procedure for determining the value of supply under GST.

Determining Value of Supply under GST

Determining Value of Supply under GST

Value of Supply - Related Party Transaction or Distinct Persons

The calculation for the value of the supply of goods or services or both made through an agent and not between distinct persons or related parties, shall apply as:

- The open market value of such supply,

- If the open market value is not available, be the value of the supply of goods or services of like kind and quality,

- If the value is not determinable under the above two methods, then the value as determined by the cost method or residual method,

- Besides, if the recipient intends to further the supply of goods to a customer (not related to the supplier) and the supplied value of the goods equals 90% of the price charged for the supply of goods, such as in variety and quality,

- The recipient shall consider the value declared in the invoice as part of the open market value of goods or service if the recipient receives full eligibility to avail input tax credit(ITC).