IndiaFilings

Expert

Published on: Apr 22, 2026

Start Business India - How to Start a Business in India

Entrepreneurial aspirations among youngsters are rising along with the growing middle class in India. Technology has opened up numerous business opportunities and made starting and managing a business easier. Therefore, it is more rewarding than any other time to start a business in India. In this article, we look at how to start a business in India.

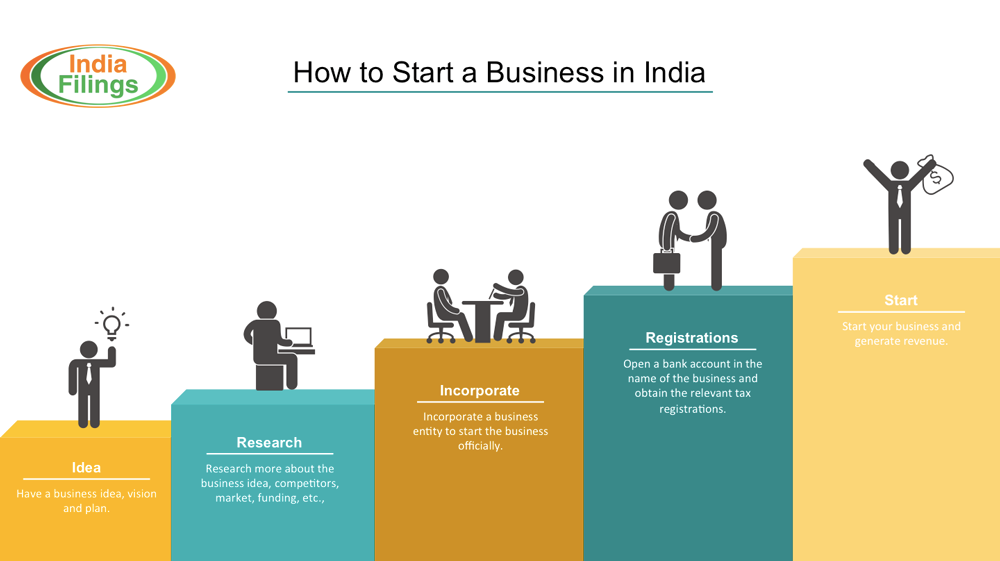

Infographic on how to start a business in India

Infographic on how to start a business in India

Choosing a Business

Prior to starting a business, the Entrepreneur must have a vision for the proposed business. A vision could be as simple as a plan of action to starting a business in the mind of the Entrepreneur or could even be a detailed business plan with market analysis, projected financial statement, etc., Detailed business plans will help the Entrepreneur avoid mistakes and increase the chances of succeeding in the business. In case the Entrepreneur doesn't have any preconceived business idea, he or she can research online for business ideas. The following are good resources for finding a business idea:

- Home-based business ideas in India

- Kickstarter

- Business Idea Center

- Big List of Business Ideas

- Small business Ideas

Business Entity Registration

The first step in starting a business in India is deciding and choosing a business entity. Choosing a business entity is akin to choosing a vehicle for a journey. If a long journey is expected, it is best to opt for a car. Similarly, if a medium to large-sized business is envisaged, it is best to incorporate a Private Limited Company. On the other hand, if the business envisioned is micro or small, it would be wise to start a Limited Liability Partnership (LLP) or Proprietorship.

If the entrepreneur decides to start an LLP or Private Limited Company, two persons would be required to act as Partners or Directors. A document like PAN Card and address proof of the promoters would also be required during incorporation of LLP or Private Limited Company. To talk to a Business Advisor about starting a business in India or choosing the right business entity, visit IndiaFilings.com or Call: +91-44-40247777.

Bank Account Opening

Opening a bank account in the name of the business is one of the first tasks to be completed after incorporation of the business entity. Corporate entities like LLP, Private Limited Company, One Person Company and Limited Company are allowed to open a bank account in India by submitting a copy of the Certificate of Incorporation and PAN Card of the entity. On the other hand, opening a bank account in the name of the business for a Proprietorship entity could be more cumbersome - as one or more tax registrations may be required to establish the identity of the proprietorship business. Refer to the article on "Opening a business bank account in India", for more information.

If a bank loan is required for working capital or purchase of equipment while starting a new business, it is best to open a bank account with a Nationalized Bank. Nationalized banks are more in favour of providing bank loans for startups when compared to privatized banks. Hence, the right banker must be selected while opening a business account.

Tax Registration

Based on the type of activity proposed by the business or vendor criterion or customer requirements, various tax registrations may be required for the business, as follows:

GST Registration: GST registration is mandatory for any person or entity if the turnover is over Rs.20 lakhs in most states.

TAN Registration: TAN Registration is mandatory for tax deduction at source (TDS). Therefore, TAN Registration may be required while hiring employees or dealing with certain customers or vendors.

ESI Registration: ESI Registration will be mandatory when the number of employees in the business crosses 20. Proof of ESI Registration is often requested by businesses that outsource manpower requirements.