IndiaFilings.com

Expert

Published on: Jul 30, 2026

Section 80G Deduction - Income Tax Act

Section 80G Deduction is a facility available in the Income Tax Act which allows taxpayers to claim deductions for various contributions made as donations. The deduction under the Act is available for contributions to the specified relief funds and charitable institutions. Not all charitable donations are eligible for deduction under Section 80G of Income tax act. Only donations made to the prescribed funds can qualify as a deduction. The Government of India introduced Section 80G deduction to encourage people to donate. By providing income tax relief, the government intends to motivate people to donate more to worthy causes.Under Section 80G deduction, the amount donated can be claimed as a deduction when filing the assessee's income tax return. Section 80G Deduction can be claimed by individuals, partnership firms, HUF, companies and other types of taxpayers, irrespective of the type of income earned. Trusts and institutions registered under Section 80G of Income tax act are provided with a registration number by the Income Tax Department, and donors should ensure their receipt contains this number. This registration number needs to be valid on the date of a particular donation. If the donation is made while the Section 80G Income tax registration is not valid, then the donation would not be eligible for deduction.

Claim your 80G deductions with ease—file your income tax return online with IndiaFilings!

What is a Section 80G Tax Exemption?

Section 80G tax exemption is a provision in the Indian Income Tax Act that encourages charitable giving by offering tax deductions for donations made to specified institutions. This means you can reduce your taxable income by the amount you donate, potentially lowering your overall tax liability. However, there are limitations and specific criteria for eligible donations and institutions.

Amount of Deduction under Section 80G Income tax

Donations paid towards eligible trusts and charities which qualify for tax deductions are subject to certain conditions. Donations under Section 80G Income tax can be broadly classified into four categories. The categories are mentioned below:Donations with 100% deduction (Available without any qualifying limit)

Donations made under this category can obtain a 100% tax deduction and are not subject to the requirement to achieve any qualification criterion. Donations to the National Defence Fund, the Prime Minister’s National Relief Fund, The National Foundation for Communal Harmony, the National/State Blood Transfusion Council, etc., qualify for such deductions.- National Defence Fund set up by the Central Government.

- Prime Minister's National Relief Fund.

- Prime Minister's Armenia Earthquake Relief Fund.

- Africa (Public Contributions - India) Fund.

- National Children's Fund.

- National Foundation for Communal Harmony.

- A University or any educational institution of national eminence approved by the prescribed authority in this behalf.

- Chief Minister's Earthquake Relief Fund, Maharashtra.

- Fund set up by the State Government of Gujarat exclusively for providing relief to the victims of earthquake in Gujarat.

- Zila Saksharta Samiti constituted in any district under the chairmanship of the Collector of that district for the purposes of improvement of primary education in villages and towns in such district and for literacy and post-literacy activities. Town means a town with a population not exceeding one lakh as per last census.

- National Blood Transfusion Council or any State Blood Transfusion Council which has its sole object the control, supervision, regulation or encouragement in India of the services related to operation and requirements of blood banks.

- Fund set up by a State Government to provide medical relief to the poor.

- Army Central Welfare Fund or the Indian Naval Benevolent Fund or the Air Force Central Welfare Fund established by the armed forces of the Union for the welfare of the past and present members of such forces or their dependants.

- The Andhra Pradesh Chief Minister's Cyclone Relief Fund, 1996.

- National Illness Assistance Fund.

- The Chief Minister's Relief Fund or the Lieutenant Governor's Relief Fund in respect of any State or Union territory, as the case may be.

- National Sports Fund set up by the Central Government.

- National Cultural Fund set up by the Central Government.

- Fund for Technology Development and Application set up by the Central Government.

- National Trust for Welfare of Persons with Autism, Cerebral Palsy, Mental Retardation and Multiple Disabilities.

- Swachh Bharat Kosh, set up by the Central Government.

- Clean Ganga Fund, set up by the Central Government.

- The National Fund for Control of Drug Abuse constituted under section 7A of the Narcotic Drugs and Psychotropic Substances Act, 1985.

Donations with 50% Deduction (Available without any qualifying limit)

Donations made towards trusts like the Prime Minister’s Drought Relief Fund, National Children’s Fund, Indira Gandhi Memorial Fund, etc., qualify for a 50% tax deduction on the donated amount.

- Jawaharlal Nehru Memorial Fund.

- Prime Minister's Drought Relief Fund.

- Indira Gandhi Memorial Trust.

- Rajiv Gandhi Foundation.

Donations with 100% deduction (Available up to 10% of adjusted gross total income)

Donations made to local authorities or the government to promote family planning and donations to the Indian Olympic Association qualify for deductions under this category. In such cases, only 10% of the donor’s Adjusted Gross Total Income is eligible for deductions, and donations exceeding this amount are restricted to 10%.Donations with 50% deduction (Available up to 10% of adjusted gross total income)

Donations made to any local authority or the government that would then use the money for any charitable purpose qualify for deductions under this category. In such cases, only 10% of the donor’s Adjusted Gross Total Income is eligible for deductions, and donations exceeding this amount are capped at 10%.- Any fund or any institution established for charitable purposes and approved by the Commissioner of Income-Tax, which is constituted as a

- Public charitable trust; or

- Registered under the Societies Registration Act, 1860; or

- Registered under section 8 of the Companies Act, 2013; or

- University established by law, or is any other educational institution recognised by the Government or by a University established by law, or affiliated to any University established by law; or

- Is an institution financed wholly or in part by the Government or a local authority.

- Government or any local authority, to be utilised for any charitable purpose other than the purpose of promoting family planning.

- An authority constituted in India by or under any law enacted either for the purpose of dealing with and satisfying the need for housing accommodation or for the purpose of planning, development or improvement of cities, towns and villages, or for both.

- Any corporation for promoting interest of minority community.

- Donations for the renovation or repair of any such temple, mosque, gurdwara, church or other place as is notified by the Central Government in the Official Gazette to be of historic, archaeological or artistic importance or to be a place of public worship of renown throughout any State or States.

Adjusted Gross Total Income

The term 'adjusted gross total income' refers to the

gross total income (which is the summation of income under various heads prior to providing relief under the provisions of Chapter VI-A) as reduced by the following:- Amount deductible under Sections 80CCC to 80U (without including Section 80G of Income tax act)

- Exempt income as per Section 10 of the Act

- Long-term capital gains

- Short-term capital gains are taxable at @15 per cent under section 111A.

- Income referred to in Sections 115A, 115AB, 115AC, 115AD, pertaining to non-residents and foreign companies.

Know more about

donations qualifying for Section 80G deduction.Documents Required for Claiming a Deduction

Taxpayers claiming Section 80G deduction must have the following documents to support the claim.Donation Receipt

It is mandatory to have a donation receipt issued by the Trust or Charity which received the donation. This receipt should include the following details mandatorily to be valid:- Name and address of the Trust or NGO

- Name of the Donor

- Amount donated (mentioned in words and figures)

- Registration number of the Trust, as given by the Income Tax Department under Section 80G tax exemption along with the period of validity.

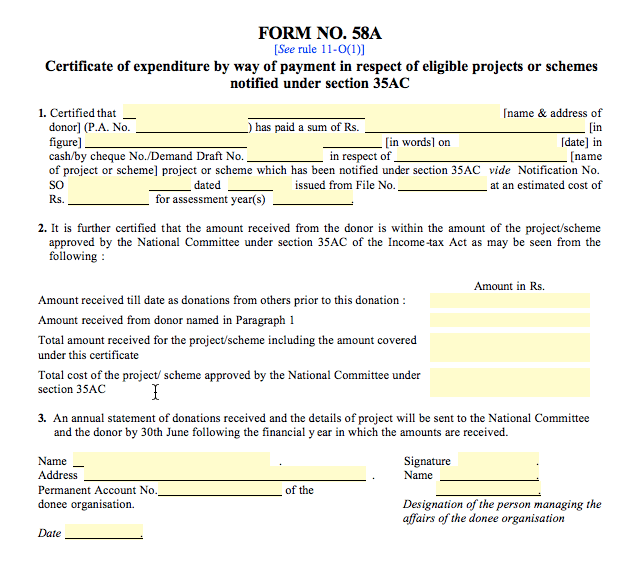

Form 58A

Form 58A is required if the taxpayers claims 100% deduction on a donation, without which their donation will not be eligible for 100% deduction. Form58A will be provided only for certain types of eligible deductions. Form 58A Format

Form 58A Format

Download Form 58A format for Section 80G Deduction

Section 80G Validity & Renewal

Under Section 80G, organizations initially receive a provisional registration valid for three years. Upon successful renewal, the registration extends for another five years, after which it must be renewed every five years to maintain tax exemption benefits.

Important Note: For Section 8 companies, the 80G registration remains valid until March 2025, requiring renewal in the same month to continue availing benefits for Assessment Year (AY) 2025-26. Timely renewal is essential to ensure uninterrupted eligibility for tax deductions and compliance with regulatory requirements.

Maximize your tax savings on donations—start your income tax return e-filing with IndiaFilings now!