IndiaFilings

Expert

Published on: Apr 22, 2026

Guide to Annual General Meeting

Annual General Meeting (AGM) is a meeting conducted by every Private Limited Company or Limited Company that provides an opportunity to the shareholders to meet every year and discuss matters relating to the Company. The AGM ensures the interest of the shareholders are protected. In this article, we look at the procedure for conducting an AGM and recording the same.

For more details on AGM, refer to our article: 1Purpose for Annual General Meeting

Annual General Meeting is a statutory requirement for Private Limited Company and Limited Company in India. Every Company whether, public or private, limited by shares or guarantee, with or without share capital or unlimited company is required to hold an AGM every year. Annual General Meeting is an annual meeting conducted by the shareholders and Directors of the Company. In the Annual General Meeting, the audited accounts of the Company are approved, appointment of auditors and Directors are finalized. Other items that can be decided in an AGM include compensation of officers, confirmation of proposed dividends and any other issue raised by shareholder.

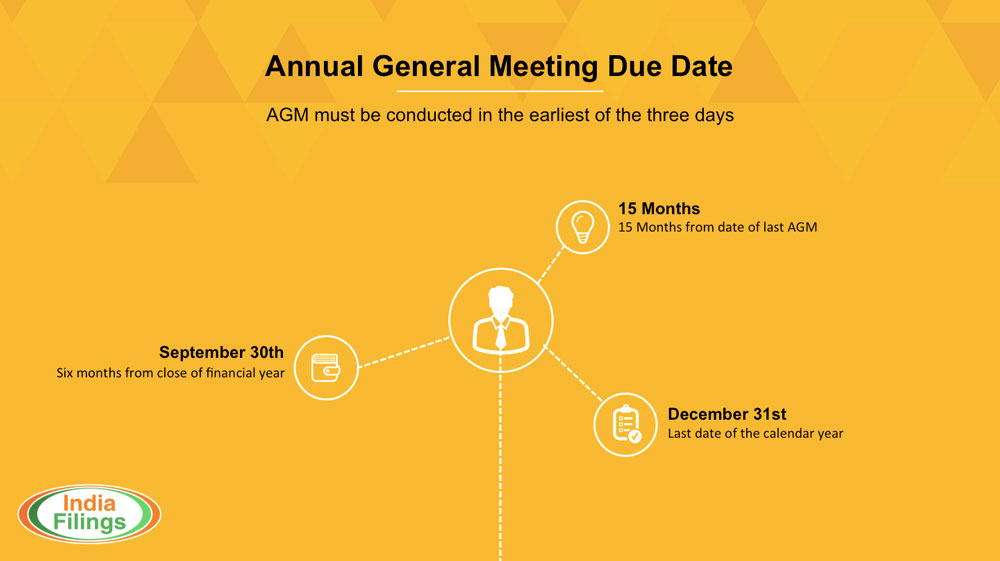

First Annual General Meeting

Annual General Meeting Infographic

Annual General Meeting Infographic

- 15 months from the date of last annual general meeting.

- the last day of the calendar year (December 31st).

- 6 months from close of the financial year (September 30th).

All company must hold an annual general meeting in every calendar year. However, if the first annual general meeting is held within 18 months from the date of its incorporation, it is not necessary to hold any annual general meeting in the year of incorporation or in the following year.

Notice for Annual General Meeting

The notice for annual general meeting must be sent to all the member, auditors and debenture trustees atleast 21 days before the meeting along with the annual report of the Company. Shorter notice may be provided with the consent of all the members entitled to vote at the meeting.

Quorum for Annual General Meeting

For a Quorum, 5 members personally present in the case of

public limited company and 2 members personally present in the case of Private Limited Company shall be the quorum for the meeting, unless the 1 provides for a larger quorum. The proxies cannot be counted for the purpose of quorum. If within half an hour from the time appointed for holding a meeting, the quorum is not present, the meeting, shall stand adjourned to the same day in the next week at the same time and place, or to such other day, time and place as the Board of Directors may determine. If at the adjourned meeting also, a quorum is not present within half an hour from the appointed time, then the members present shall be the quorum.Notice for Annual General Meeting as Per Companies Act, 2013

You can download the Notice for Annual General Meeting as per Companies Act, 2013 from the following:

- Download Notice of Annual General Meeting Format as per Companies Act, 2013 in PDF Format.

- Download Notice of Annual General Meeting Forma as per Companeis Act, 2013 in Word Format.

Procedure for Conducting Annual General Meeting

The procedure for conducting the annual general meeting is explained in detail below:

Before the Meeting

- Convene a board meeting after giving notice as soon as the financial statements are ready.

- Discuss the report of the audit committee on the annual accounts.

- Validate the draft of the board's report in compliance with the provisions of Section 134 of the Companies Act, and authorise the chairman to sign the report on behalf of the board.

- Consider the payment of dividend if it is to be declared in the annual general meeting.

- Fix place, date and time for the annual general meeting and approve the draft notice. Also, authorise the secretary to issue the notice for the meeting.

- To consider the closure of the members in the register and share transfer books of the company.

- In the case of listed companies, a notice should be sent to the stock exchange within seven working days about the dates proposed for such closure.

- If the directors decide for the publication in a newspaper should be arranged seven days before from the notice of closure of the register of members and the share transfer books.

- To arrange for the printing of a notice of the general meeting, ensure the notice containing the following contents:

-

- Time, date and place of the meeting

- Matters to be transacted in the meeting

- Procedure of e-voting, if any

- Proxy form

- Explanatory statement

- Route Map

At the Meeting

- As per the secretarial standard, arrange for the sitting arrangement to enable the directors and the company secretary to be seated by the chairman.

- Arrange for the collection of admission slip to get the attendance register signed by the shareholders and make them comfortable in their seating.

Appointment of the Chairman

- Ensure the chairman should be present within 15 minutes from the beginning of the meeting at the venue.

- In case of absence of the chairman, ensure the directors present at the meeting elect among themselves as the chairman of the meeting.

- Read the notice of the meeting and auditor report, if advised by the chairman.

- Produce a copy of Memorandum and Articles of Association (AOA) of the company.

- Supply to the chairman if any information required by the shareholders relating to accounts and other connected matters.

- Ensure the chairman of the audit committee is present at the annual general meeting to give any clarifications related to audit and shareholders queries.

After the Meeting

- Prepare minutes of the proceedings and record the minutes of the meeting and the same has to be signed by the chairman within 30 days from the meeting.

- Send an intimation of appointment of directors by filing form DIR-12 with the registrar of companies within 30 days from the appointment along with the applicable fee.

- File copies of special and other resolution along with the form MGT-14 within 30 days of the meeting to the registrar of companies.

- File profit and loss account and balance sheet reports of the directors and the auditors and notice of the meeting in form AOC-4 with 30 days from the meeting.

- To deposit the dividend distribution tax at the applicable rate within the specified time limit under the income tax act.

- The copy of the balance sheet to be forwarded to the RBI, where the company has invited public deposits.

- Open a separate bank account as "Dividend Account" and deposit the total amount of dividend within five days from the authorised persons.

- Dividend warrants and a notice of dividend to be signed by the authorised persons.

- File annual return in form MGT-7 with the registrar of companies within 60 days of the meeting and the certificate of the company secretary should be in Form MGT-8 and ensure that the annual return is also signed by the company secretary.

- In the case of listed companies, a report of the annual general meeting in form MGT-15 should be submitted to ROC within 30 days of the meeting.