IndiaFilings

Expert

Published on: Jul 30, 2026

Gst Unique Identification Number (UIN)

Regular taxpayers, casual taxable persons and a

non-resident taxable person who apply for GST registration are provided with Gst Unique Identification Number (UIN) or Goods and Services Tax Identification Number. In addition to the GSTIN, GST Unique ID can be allotted by the GST Authorities. In this article, we look at GST Unique Id in detail.GSTIN vs GST Unique ID

All the regular taxpayers should acquire the Goods and Services Tax Identification Number or the GSTIN to collect and file GST returns. However, the GST department allots Unique Identification Number (UIN) only for a particular set of people as notified under the GST Act. Hence, GSTIN and GST Unique ID are different forms of identification under GST.

Who can get GST Unique ID?

The GST Act states that any specialised agency of the United Nations Organisation or any Multilateral Financial Institution and Organisation notified under the United Nations (Privileges and Immunities) Act, 1947, Consulate or Embassy of foreign countries and any other persons notified by the Commissioner can be granted a GST Unique Identity Number. GST Unique Identity Number can be used for the purposes of claiming GST refund on notified supplies of goods or services and other purposes as notified by the GST authorities.

How to apply for GST UIN?

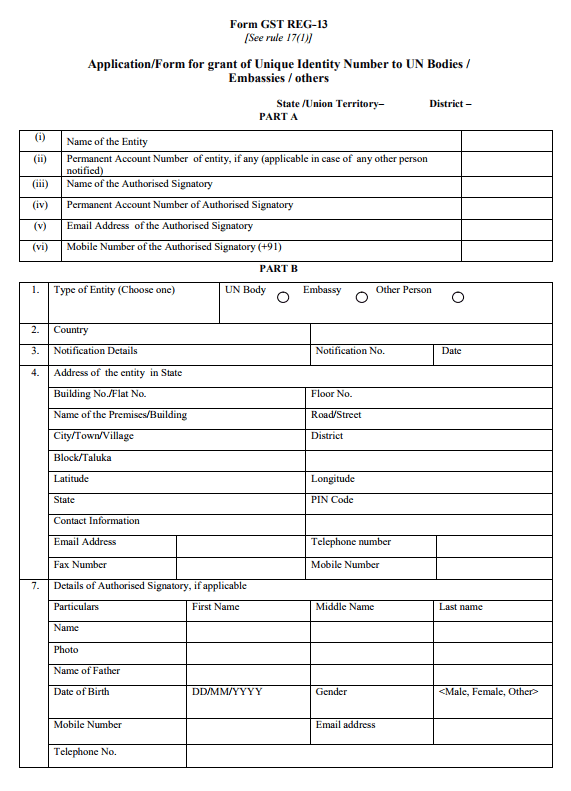

As mentioned above, Consulates, Embassies and other specialized agencies can opt to receive GST UIN. The Ministry of Finance grants GST UIN to the above-mentioned institutions. The institutions can opt to apply GSTIN through the Form GST REG-13. The below image displays a sample of Form GST REG-13, for reference:

GST REG-13 - Page 1

GST REG-13 - Page 1

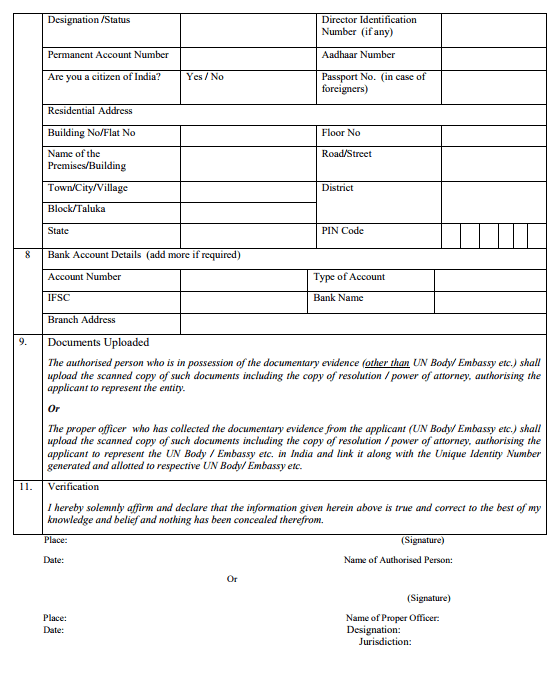

GST REG-13 - Page 2

In addition to applying for GST UIN using FORM REG-13 on the GST Common Portal, consulates and embassies can also be granted suo-moto registration by a GST officer.

GST REG-13 - Page 2

In addition to applying for GST UIN using FORM REG-13 on the GST Common Portal, consulates and embassies can also be granted suo-moto registration by a GST officer.

How long does it take to obtain GST UIN?

After filing FORM GST REG-13, the GST office processing the application should issue a GST certificate in FORM GST REG-06 within a period of three working days from the date of the submission of the application.

GSTR-11 Filing

All persons registered with UIN should file GSTR-11 returns on a quarterly basis. Based on the GSTR-11 return filing, GST refunds will be processed by the Government. Further, UIN holders will not be allowed to add or modify any details in GSTR-11, only the auto-populated information from GSTR-1 filing can be verified and filed by the GST UIN holder. Know more about

GST return filing.