Sreeram Viswanath

Published on: Jul 8, 2026

GST Appellate Tribunal (GSTAT): Rules, Members, Procedures, Fees & Appeal Process

Since the implementation of GST, numerous disputes have arisen concerning its rates, refunds, and overall application. Previously, due to the absence of specialized forums, all GST-related matters were directed to the High Courts, creating significant challenges for taxpayers. To streamline the resolution of these issues, the GST Council approved the establishment of the GST Appellate Tribunal (GSTAT). This tribunal provides a dedicated platform to handle GST disputes efficiently and effectively. In this article, we explore the GST Appellate Tribunal in detail.

Latest Updates

GST Portal Now Enabled to File Appeals Against Rejection Orders (SPL-07) Under GST Amnesty Scheme

56th GST Council Meeting 2025

The upcoming 56th GST Council meeting in 2025 is expected to clarify whether the National Anti-Profiteering Authority (NAA) will be revived or whether the GST Appellate Tribunal (GSTAT) will be empowered to accept new anti-profiteering complaints. This comes amid expectations of potential GST rate and slab revisions.

22nd June 2024 – 53rd GST Council Meeting

During the 53rd GST Council meeting held on 22nd June 2024 in New Delhi, several key recommendations were made regarding appeals under GST:

Monetary limits for filing appeals:

- GSTATs: Rs. 20 lakhs

- High Courts: Rs. 1 crore

- Supreme Court: Rs. 2 crores

Reduction in pre-deposit amounts:

- Maximum filing amount with the Appellate Authority reduced from Rs. 25 crore (each of CGST and SGST) to Rs. 20 crore.

- Pre-deposit for appeals with the Appellate Tribunal reduced from 20% (capped at Rs. 50 crore each of CGST and SGST) to 10% (capped at Rs. 20 crore each of CGST and SGST).

Amendment to Section 112 of the CGST Act, 2017:

The Council recommended allowing the three-month period for filing appeals before the Appellate Tribunal to start from a government-notified date for appeal/revision orders issued prior to that notification. This ensures taxpayers have adequate time to file appeals in pending cases.

What is the GST Appellate Tribunal?

Before exploring further details, it is essential to understand the GST Appellate Tribunal (GSTAT). The Tribunal is a specialised authority established to resolve GST-related disputes at the appellate level. It serves as the forum for second appeals under GST laws and acts as the first common platform for dispute resolution between the Centre and the states.

The GST Appellate Tribunal aims to ensure uniformity in dispute resolution and facilitate the faster settlement of cases. Its principal bench is located in New Delhi, providing a central hub for hearing and deciding appeals across the country.

GST Appellate Tribunal Composition

The GST Appellate Tribunal (GSTAT) is structured to include both a National Bench and State Benches:

National Bench (New Delhi):

- President (Head)

- Judicial Member

- Technical Members: one representing the Centre and one representing the state

State Benches:

- Two Judicial Members

- Technical Member (Centre)

- Technical Member (State)

This composition ensures a balanced representation of judicial and technical expertise from both the Centre and the states, facilitating fair and uniform resolution of GST disputes.

Click here to know more about the GST Appellate Tribunal Principal and State Benches & Jurisdiction

GST Appellate Tribunal Members

Members of the GST Appellate Tribunal (GSTAT) are appointed by the government and include:

- Judicial Member

- Two Technical Members: one representing the Centre and one representing the state

The National Bench, headed by the President, primarily addresses matters related to the place of supply, while regional and state benches handle appeals within their respective jurisdictions. The distribution of responsibilities among members is determined by the President and, for state benches, the State President.

In cases where a member is unavailable, an appeal may be heard by two members or, in certain circumstances, a single member. The government also has the authority to transfer members for administrative convenience, recognizing the distinct roles and requirements of Centre and state representatives.

GST Appellate Tribunal (GSTAT) Members’ Eligibility and Age

Membership in the GST Appellate Tribunal (GSTAT) is subject to specific eligibility and age criteria:

- President: Must be a Supreme Court judge or have served as Chief Justice of a High Court. Maximum age: 70 years.

- Judicial Member: Must be a High Court judge or have served as an Additional District Judge or District Judge for at least 10 years. Maximum age: 65 years.

- Technical Member (Centre): Must be an Indian Revenue Service (IRS) officer, Group A, or a member of the All India Service with at least 3 years of experience in administering GST at the Central Government. Additionally, the member should have completed 25 years in Group A service. Maximum age: 65 years.

- Technical Member (State): Must be a State Government officer or All India Service officer with a rank above Additional Commissioner of VAT and higher than the First Appellate Authority. The member should have completed 25 years in Group A services or equivalent and at least 3 years in GST, finance, or taxation administration in the State Government. Maximum age: 65 years.

These criteria ensure that members possess significant judicial or technical experience, maintaining the Tribunal’s ability to deliver expert.

GST Appellate Tribunal: Rules, Powers, and Duties

Rules

The GST Appellate Tribunal (GSTAT) operates under rules prescribed by GST laws, which govern its procedures, functioning, and conduct of hearings. These rules are periodically updated to reflect changes in GST regulations and best practices. Key provisions include:

- Filing of appeals and timelines for submissions

- Documentation and evidence requirements

- Procedures for conducting hearings, both physical and virtual

Powers

The Tribunal is vested with broad powers to ensure effective adjudication of disputes:

- Hear appeals against orders of the First Appellate Authority

- Decide on disputes involving GST assessments, penalties, interest, and refunds

- Confirm, modify, annul, or remand decisions of lower authorities

- Rectify errors in its own orders and grant interim relief when appropriate

The Tribunal is not bound by the Code of Civil Procedure, 1908, but it adheres to the principles of natural justice and has the authority to regulate its own procedures. It possesses powers similar to a civil court under the Code of Civil Procedure, including:

- Summoning individuals

- Requiring the production of documents

- Accepting evidence on affidavits

The Tribunal can requisition public records, issue commissions for witness examination, and dismiss or decide representations for default. Orders issued by the Tribunal are enforceable as if they were court decrees, with the Tribunal empowered to seek execution within its local jurisdiction.

All proceedings before the Tribunal are considered judicial proceedings, and it is deemed a civil court for specific legal purposes, in line with relevant provisions such as Sections 193, 228, and 196.

Duties

The primary duties of GSTAT focus on fair, transparent, and timely resolution of GST disputes:

- Deliver impartial judgments consistent with the legislative intent of GST laws

- Ensure uniform interpretation and application of tax provisions across the country

- Maintain records of proceedings and judgments, which serve as precedents for future cases

- Facilitate accurate filings and appeals, ensuring correct attribution of cases, including proper use of GST State Codes

GST Appellate Tribunal Website

The GST Appellate Tribunal (GSTAT) website serves as a valuable resource for taxpayers seeking information or guidance on GST-related disputes. The website provides comprehensive details on:

- The constitution and jurisdiction of the Tribunal

- Procedures for filing and tracking appeals

- Orders and judgments issued by the Tribunal

In addition, the website offers several resources for taxpayers, including:

- User guides

- Frequently asked questions (FAQs)

- Contact information for further assistance

This online portal ensures easy access to information and helps taxpayers navigate the appellate process efficiently.

Who Can Appeal to the GST Appellate Tribunal?

Any taxpayer or revenue department dissatisfied with the decision of the First Appellate Authority under GST laws can file an appeal with the GST Appellate Tribunal (GSTAT). This includes disputes related to:

- Tax assessments and demands

- Refund claims

- Input Tax Credit (ITC)

- Penalties and fines

Appeals can be filed by individuals, businesses, or tax officials seeking a review of the First Appellate Authority’s order. The Tribunal provides a fair and impartial forum for the resolution of GST disputes in accordance with the law.

Before filing an appeal, it is essential to ensure that your GST registration is valid and up to date, as only registered taxpayers are generally eligible to initiate appeals.

Also read: Major GST Refund and Appeal Rules Announced by CBIC

How to File an Appeal with GSTAT: Step-by-Step Guide

Filing an appeal with the GST Appellate Tribunal (GSTAT) involves a structured process to ensure proper submission and consideration of the case:

Step 1: Obtain Certified Copy

Secure a certified copy of the order against which the appeal is being filed. This serves as the basis for your appeal.

Step 2: Prepare the Appeal

Draft the appeal petition, clearly stating the grounds of appeal. Include all supporting documents and evidence to substantiate your claims.

Step 3: File the Appeal

Submit the appeal within the prescribed time frame. Pay the prescribed fees at the time of filing.

Step 4: Attend the Hearing

Participate in the hearing as notified by the Tribunal. Both parties—appellant and respondent—present their arguments and evidence.

Step 5: Tribunal Judgement

After considering all submissions, the Tribunal delivers its judgement. The decision may confirm, modify, annul, or remand the original order.

Following this step-by-step procedure ensures that the appeal is processed efficiently and in compliance with GST rules, giving the taxpayer a fair opportunity for resolution.

Click here to know more about the How to File GST Appeals Online Step-by-Step

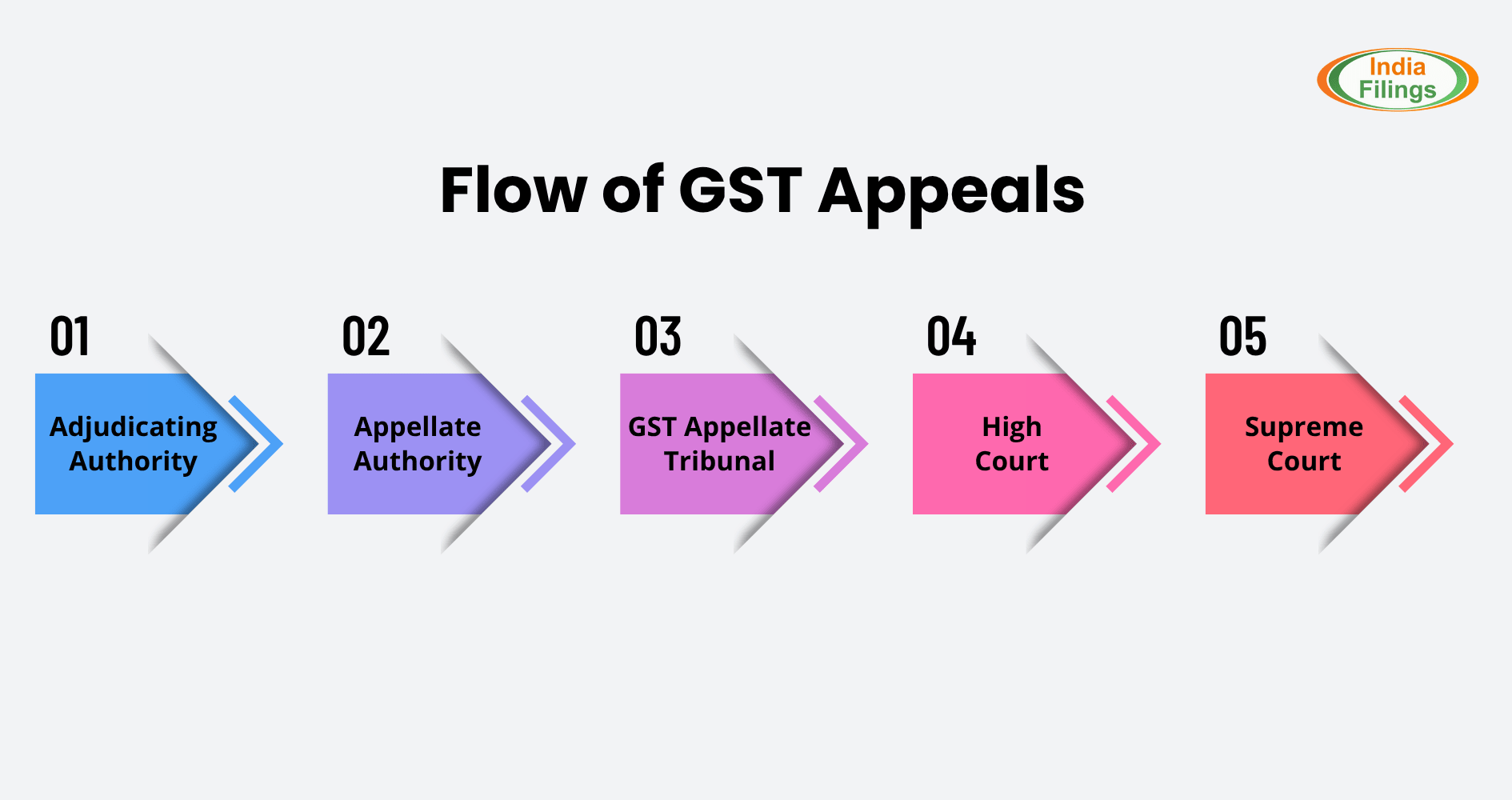

Flow of GST Appeals: From Appellate Authority to the Supreme Court

The GST appeal process follows a structured, multi-tiered system to ensure fair, timely, and legally sound resolution of disputes. The flow is designed to address issues at the appropriate level while allowing escalation for significant legal questions.

1. Appellate Authority (First Level of Appeal)

The Appellate Authority (AA) is the first forum for appeal for taxpayers aggrieved by orders of the adjudicating authority. Key features include:

- Who can appeal: Any taxpayer dissatisfied with the initial adjudication.

- Time limit: Appeals must be filed within three months of receiving the order; delays up to one month may be condoned for sufficient cause.

- Procedure: The AA follows principles of natural justice, allowing the applicant to be heard, permitting up to three adjournments, and accepting additional grounds if reasonable.

- Decision timeframe: Typically within one year of filing the appeal.

- Powers: Can confirm, modify, or annul the original order; impose fines or penalties in cases of confiscation or errors; and allow the applicant to correct mistakes, make payments, or adjust wrongly claimed input tax credit.

2. GST Appellate Tribunal (Second Level of Appeal)

If the taxpayer or department is dissatisfied with the AA or Revisional Authority, an appeal may be filed with the GST Appellate Tribunal (GSTAT).

- Structure:

- National/Regional Bench: Handles disputes involving place of supply.

- State/Area Bench: Handles other regional disputes.

- Time limit: Appeals must be filed within three months from the communication of the order; an additional three-month condonation is allowed for sufficient cause.

- Powers: The Tribunal may confirm, modify, annul, or remit the case back to the AA/Revisional Authority with directions. It can grant three adjournments to either party and may reject appeals involving amounts of ₹50,000 or less.

- Cross-objections: Taxpayers may include additional grounds not raised in previous appeals.

3. Reviews by the Commissioner (Revisional Authority)

If the department is aggrieved, the Commissioner may act as a Revisional, Appellate, or Adjudicating Authority.

- Can direct subordinate officers not involved in the original decision to act.

- Has the authority to stay, modify, or correct orders deemed improper or illegal after giving an opportunity for the concerned parties to be heard.

4. High Court

Not every appeal proceeds to the High Court; it is limited to cases presenting a substantial question of law.

- Who can appeal: Either the taxpayer or the department, against orders of the State/Area Bench of GSTAT.

- Time limit: Appeals must be filed within 180 days of the order; delays may be condoned for valid reasons.

- Scope: Primarily focuses on legal issues, though factual review may be considered in exceptional cases.

5. Supreme Court

The Supreme Court is the final appellate forum.

- Appeals can be filed against High Court decisions if certified fit by the High Court.

- In certain cases, appeals may also be filed directly from the National/Regional Bench of GSTAT.

- The Court handles matters of significant legal importance, ensuring consistency in the interpretation of GST laws.

Summary Flow

The GST appeal process can be summarized as follows:

Will Every Appeal Be Accepted by GSTAT?

Not every appeal filed with the GST Appellate Tribunal (GSTAT) is automatically accepted. The Tribunal exercises discretion in admitting or rejecting appeals based on the merits and compliance of each case.

Grounds for Rejection Include:

- Appeals deemed frivolous or vexatious

- Appeals filed beyond the prescribed time limit without sufficient cause

- Appeals that do not meet statutory requirements under GST laws

- Failure to comply with procedural rules, such as non-payment of the required filing fee

This ensures that the Tribunal focuses on genuine disputes and maintains an efficient and fair appellate process.

GST Appeal Fees

The fees for filing an appeal with the GST Appellate Tribunal (GSTAT) depend on the nature of the appeal and the monetary value involved.

Appeals concerning tax, interest, or penalties require payment of a specified fee, usually calculated as a percentage of the disputed amount.

For departmental appeals, the monetary limit is ₹20 lakhs, while for taxpayers, the pre-deposit is 20% of the disputed amount, capped at ₹20 crore each for CGST and SGST.

Interest Payable on Refund of Fees

If an appellant succeeds in their case before the GST Appellate Tribunal (GSTAT), they are generally entitled to a refund of the fees paid at the time of filing the appeal.

In addition, if there is an unreasonable delay in processing the refund, the appellant may also be eligible to receive interest on the refunded amount. This interest serves to compensate the appellant for the period during which their funds were held by the tax authorities, ensuring fairness and equity in the appellate process.

The rate and conditions for such interest are governed by GST laws and may vary depending on the specifics of the case.

Conclusion

The GST Appellate Tribunal (GSTAT) provides a specialised and streamlined forum for resolving disputes under the GST regime, ensuring uniformity, transparency, and timely justice. With a clear structure, defined powers, and well-established procedures, GSTAT enables both taxpayers and authorities to address disputes efficiently.

Understanding the appeal process, fees, timelines, and eligibility criteria is crucial for filing successful appeals. As GST laws continue to evolve, staying informed about recent council updates, digital filing options, and procedural requirements will help taxpayers navigate the system effectively and safeguard their rights.

Confused in complicated laws? Take our GST consultation services to get your issues solved from GST experts.