DINESH P

Published on: Jun 24, 2026

GST Amnesty Scheme: Benefits, Eligibility, & Forms

The GST Amnesty Scheme, introduced under Section 128A of CGST Act, aims to ease the compliance burden on taxpayers by waiving interest and penalties on tax demands raised under Section 73. Effective from November 1, 2024, this amnesty scheme GST 2025 encourages businesses to settle outstanding dues and regularise compliance without heavy penalties. Rule 164 of CGST Rules outlines the procedure and conditions for the closure of proceedings. To avail of its benefits, taxpayers must clear payment dues before the specified deadline and submit relevant forms. This article provides a detailed outlook on the Amnesty Scheme GST 2025, including its benefits, eligibility and applicable forms.Hurry up!! Let IndiaFilings experts help clear your GST dues and file the required forms to avail the scheme benefits - fast & accurate!

What is GST Amnesty Scheme?

The GST Amnesty Scheme is a government initiative designed to help taxpayers who missed the deadline for filing their Goods and Services Tax (GST) appeals. Under this scheme, eligible taxpayers were given an opportunity to regularize pending or delayed appeals by paying a reduced penalty or facing waived interest/penalties, making it easier to comply with GST regulations.

The most recent version, GST Amnesty Scheme 2024, was introduced by the Central Board of Indirect Taxes and Customs (CBIC) and was available until January 31, 2024. According to the Ministry of Finance, it provided a valuable chance for taxpayers to resolve their past compliance issues without incurring the full penalty.

Key Highlights on Section 128A - GST Amnesty Scheme

- The GST Amnesty Scheme applies for the financial years 2017-18 to 2019-20. It applies to non-fraudulent cases assessed under Section 73.

- It waives interest under Section 50, penalty or both.

- To qualify for the amnesty, the tax amount due must be paid by the specified deadline - March 31, 2025.

- Applications for waivers must be submitted before June 30, 2025.

- No refunds will be provided if interest or penalties have already been paid.

- A separate application must be filed for multiple notices, statements or orders.

- The waiver is not applicable if an appeal or writ petition is pending and not withdrawn.

- It is not applicable if any amount is payable due to an erroneous refund.

Further appeal is not allowed against the concluded order.

- Proper and timely filing of forms is essential to avoid rejections and ensure waiver approval.

Eligibility Criteria for the GST Amnesty Scheme

To qualify for the amnesty scheme GST 2025 , taxpayers must have been assessed under Section 73 (non-fraudulent cases) and received GST demand notices/orders for the financial years 2017-18 to 2019-20. It applies to interest and penalties arising between July 1, 2017, and March 31, 2020, but excludes taxpayers involved in fraudulent cases under Section 74.Meet the criteria? Start clearing your GST dues and file the necessary forms effortlessly with IndiaFilings experts by your side!!

Deadlines for the GST Amnesty Scheme

As mentioned above, the amnesty scheme GST 2025 allows taxpayers to clear their outstanding dues by March 31, 2025. Additionally, the corresponding forms must be submitted by June 30, 2025.

Below, we have attached an advisory regarding clarifications on the due dates for availing of the GST amnesty scheme. Please note that you must pay your dues by March 31st, 2025, and file the waiver applications (SPL 01/02) by June 30th, 2025.

Types of Forms Related to the GST Amnesty Scheme

The different types of forms involved in the Amnesty Scheme GST 2025 outlined in Section 128A of the CGST Act are given below:- GST SPL 01: Used for applying for a waiver related to notices or statements. Ensure to submit the documents mentioned in Table 7 of the form.

- GST SPL 02: Used for waiver applications when a demand order or order in appeal has been issued.

- GST SPL 03: Used for issuing a Show Cause Notice to the Applicant. It provides reasons forissue of Notice, mentions short tax payments if applicable, and includes the date and time for a personal hearing.

- GST SPL 04: Used for replying to the Show Cause Notice. Applicants must submit their reply within one month, along with supporting documents like tax payment proof.

- GST SPL 05: Issued to conclude proceedings if the application or reply is admitted or allowed. Specific timelines are provided for issuing the order based on whether a reply is submitted.

- GST SPL 07: Issued for rejection of an application. It includes reasons like incomplete payments, late payments, or incorrect declarations. The order is appealable, and previous appeals withdrawn for the application can be restored if no new appeal is filed.

- GST SPL 06: Issued when an appellate authority allows an appeal after rejecting the initial application.

- GST SPL 08: Issued when an appellate authority rejects an appeal.

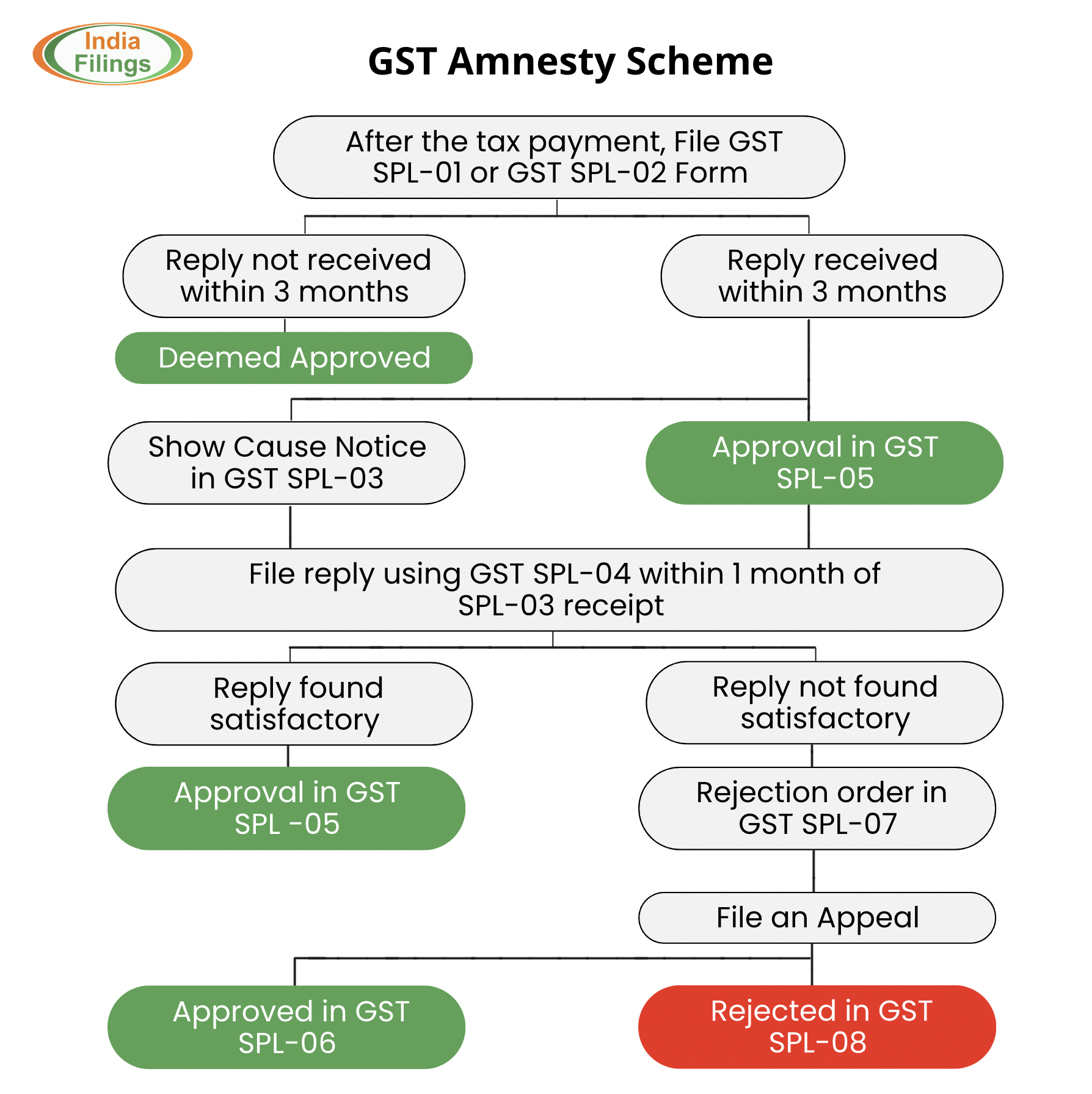

Amnesty Scheme for GST: How to File a GST Amnesty Form

Below is a clear and concise overview of the processing of forms and issuance of orders related to the Section 128A Amnesty scheme for GST, from the initial filing to the final approval.

- Payment of Tax and Initial Filing: After paying the tax, file the appropriate form, GST SPL-01 or GST SPL-02.

- Response Timeline: If no reply is received within 3 months, the application is considered Deemed Approved. If a reply is received within 3 months, further steps are taken.

- Show Cause Notice (if required): If necessary, a Show Cause Notice (GST SPL-03) will be issued to the applicant.

- Submission of Reply: Submit a reply to the notice using GST SPL-04 within 1 month of receiving SPL-03.

- Evaluation of Reply: If the reply is satisfactory, approval will be granted in GST SPL-05. An Order of Rejection (GST SPL-07) will be issued if the reply is unsatisfactory.

- Appeal Process: In case of rejection, the applicant can appeal against the order.

- Final Approval or Rejection: If the appeal is successful, approval will be granted in GST SPL-06. If unsuccessful, the application will be rejected and recorded in GST SPL-08.

Benefits of the GST Amnesty Scheme

The GST Amnesty Scheme offers several advantages for taxpayers:

- Promotes Compliance: Encourages defaulters to follow tax regulations, improving overall compliance and ensuring a stable revenue stream for the government.

- Financial Relief: Provides relief from late fees, allowing taxpayers to reinvest the saved funds into business growth and operations.

- Re-registration Opportunity: Businesses with cancelled GST registrations due to non-filing can re-register, and taxpayers can clear pending returns without incurring high interest charges.

- Penalty Reduction: Substantially reduces penalties for overdue GST returns, helping taxpayers clear backlogs and comply with regulations.

- Simplified Record Updates: Enables updating of tax records without heavy penalties, easing administrative efforts for both taxpayers and tax authorities.

Challenges of the GST Amnesty Scheme

The GST Amnesty Scheme, while beneficial, also comes with certain challenges:

- Limited Timeframe: The scheme is often available for a short period, which may not provide enough time for all eligible taxpayers to benefit. Extending the duration could allow more businesses to take advantage of it.

- Low Awareness: Many taxpayers may be unaware of the scheme and its benefits, leading to lower participation. Effective communication and outreach are essential to improve awareness.

- Input Tax Credit (ITC) Restrictions: Limitations on claiming ITC for past periods can reduce the scheme’s usefulness for businesses with significant pending credits. Greater flexibility in ITC claims could enhance its effectiveness.

- Complexity: Understanding eligibility and the application process can be difficult, especially for small businesses. Simplifying procedures and providing clear guidance can help overcome this challenge.

CBDT Notification - Clarification of Doubts Related to GST Amnesty Scheme

We have attached below the official CBDT Notification clarifies the various doubts on Section 128A of the CGST Act,Appeal Withdrawal Process Under GST Amnesty Scheme

On May 14, 2025, GSTN released a clarification on the appeal withdrawal process in relation to the GST Amnesty Scheme under Section 128a, which requires that no appeal should remain pending before the Appellate Authority against the demand order.

Key Points of the Advisory:

- Automatic Withdrawal Before Final Acknowledgment (APL-02): If a taxpayer files a Withdrawal Application (APL-01W) before the Final Acknowledgment (APL-02) is issued by the Appellate Authority, the system will automatically withdraw the original Appeal Application (APL-01).

- In this case, the status of the appeal will auto-update from “Appeal submitted” to “Appeal withdrawn”.

- Withdrawal After Final Acknowledgment – Approval Required: If the Withdrawal Application is submitted after APL-02 is issued, the appeal will be withdrawn only after approval from the Appellate Authority.

- Once approved, the status of the appeal will also change to “Appeal withdrawn”.

- Requirement Under GST Waiver Scheme (Section 128a): To avail benefits under the amnesty scheme, no pending appeal should exist against the demand order. In both of the above scenarios, once the status becomes “Appeal withdrawn”, the requirement is considered fulfilled.

- Document Requirement While Filing Waiver Application: Taxpayers must upload a screenshot of the appeal case folder clearly showing the status as “Appeal withdrawn”, whether during or after filing the waiver application.

Below, we have attached the official GST advisory regarding this notification.

Conclusion

The GST Amnesty Scheme 2024 under Section 128A provides a valuable opportunity for taxpayers to regularise their GST compliance by waiving penalties and interest on overdue returns. With extended deadlines, simplified procedures, and financial relief measures, the scheme encourages businesses to settle outstanding dues, re-register cancelled GST accounts, and ensure smoother compliance. ThisAmnesty scheme for GST

not only supports taxpayers in addressing backlogs but also enhances the overall efficiency of the tax administration system.IndiaFilings provides professional assistance to help you pay your GST dues smoothly and accurately!!